The journey of a pre-pack starts with an informal understanding, engages stakeholders, and ends with a judicial blessing of the outcome

The pre-packaged scheme, touted as the next stage in the evolution of the Insolvency and Bankruptcy Code (IBC), 2016, will attempt a balancing act, as lawmakers put together an informal arrangement with a debtor-in-possession and creditor-in-control model, as suggested in the draft proposal of the sub-committee of Insolvency Law Committee.

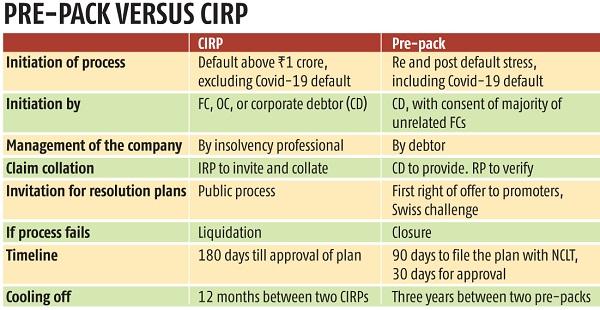

The scheme involves a step before the insolvency resolution, where creditors and the promoter agree on a plan to resolve the stressed company before admission of insolvency application. This plan can come from the promoter, if eligible under section 29A of IBC, or from a third party.

While this will be the base plan, creditors would be able to invite resolution plans to challenge it and select the best offer between promoter or investors and the one by the Swiss challenger. Each would then get a chance to better the other’s offer, depending on calculations suggested in the framework. Having studied the pre-packaged framework of different countries, India has opted for a hybrid of both informal out-of-court and formal judicial insolvency proceedings.

The journey of a pre-pack starts with an informal understanding, engages stakeholders, and ends with a judicial blessing of the outcome. “The proposed pre-packed insolvency will bring in a hybrid approach, where a debtor-in-possession would be allowed during the pre-pack insolvency, while the creditors would have enough power to maintain checks and balances to prevent any kind of abuse,” said Dinkar Venkatasubramanian, partner and national leader – restructuring and turnaround services, EY.

The purpose of this scheme is not just to have a timely and faster resolution mechanism, but also to give legal sanction to a plan agreed between banks, promoters, and the buyer. It is also expected to be lighter on courts. At a time when the suspension of corporate insolvency resolution process is about to expire and Covid-related debt needs to be resolved, the prepackaged scheme could hold many answers.

Laying the framework

The sub-committee has recommended that the corporate debtor may initiate the pre-pack, since it could prove difficult to implement if creditors were allowed to do so without the willingness of the promoter.

While some experts feel relaxation of certain eligibility criteria under section 29A for promoters may be beneficial to ensure their participation, others disagree. “Section 29A is needed in the Indian context given political sensitivity around write-offs on banks’ books,” said Rajiv Chandak, partner, Deloitte India.

Unlike the corporate insolvency resolution process (CIRP), where the resolution professional takes charge of the company, the sub-committee has proposed a debtor-in-possession model for pre-packs. The resolution professional has to be appointed with the consent of a majority of unrelated financial creditors.

Experts feel this would avoid the inevitable shock to operations associated with CIRP, where the corporate debtor shifts from the current management to the interim resolution professional, then to the resolution professional, and, finally, to the successful resolution applicant. “There are chances that corporates will refer the case to pre-pack to avoid CIRP. However, pre-pack provisions have provided for enough options to creditors to take it to CIRP with 66 per cent consent.”

The corporate debtor would require the consent of a simple majority of unrelated financial creditors for initiation of pre-pack. The committee of creditors (CoC), just like in CIRP, has the power to approve or reject a resolution plan. The CoC can also order liquidation with 75 per cent voting power, higher than the threshold of 66 per cent under CIRP. “The sub-committee recommends 90 days for market participants to submit the resolution plan to the adjudicating authority (AA), and 30 days thereafter for the AA to approve or reject it,” the sub-committee says.

The pre-pack can be initiated if there is a default in the payment of debt, especially in the context of Covid-related default, which is to get priority in the proposed framework. “If pre-pack is not available in respect of Covid-19 defaults, such defaults would never be resolved under the Code,” according to the framework.

A moratorium that gives a calm period just like in CIRP is also recommended for pre-packs, but with no option of extension.

Treading carefully

The IBC may make a skeletal provision enabling pre-packs, and prescribing the contours of subordinate legislation that will allow the government to introduce “many sophisticated variants of pre-pack”.

The future phases would cover a default above Rs 1 crore, followed by Rs 1 to Rs 1 lakh and then the pre-default stress that would require consent of 75 per cent of creditors to avoid misuse, the sub-committee has said. As far as claims go, the corporate debtor has to make available all information regarding outstanding, contingent, and future claims for verification by the resolution professional.

The framework says, “If the corporate debtor willfully provides any wrong information or omits to provide material information with respect to any claim, the same shall attract criminal liability”.

A pre-pack cannot be initiated within three years of closure of another pre-pack. This is like a CIRP, which cannot be initiated within 12 months of closure of another CIRP, and the two processes cannot run in parallel.