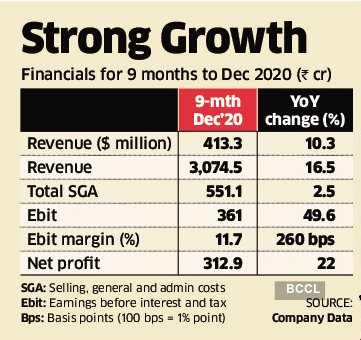

Synopsis–In line with bigger peers, Persistent showed a strong topline growth and margin improvement in the third quarter. Revenue grew by 7.4% sequentially to $146.2 million.

The stock of Persistent Systems has gained nearly 53% over the past three months. Of this, over 18% was clocked in the seven trading sessions since its third quarter result on January 28. The mid-tier software exporter reported improved order booking and better operating margin despite salary increases during the quarter. The momentum is expected to continue given the traction in its digital offerings.

In line with bigger peers, Persistent showed a strong topline growth and margin improvement in the third quarter. Revenue grew by 7.4% sequentially to $146.2 million. In the rupee terms, it rose by 6.7% to Rs 1,075.4 crore while net profit shot up by 18.6% to Rs 120.9 crore helped by lower operating cost and lesser foreign exchange loss compared with the previous quarter.

The company reported order bookings of $302 million during the quarter, one of the highest in recent quarters as clients continued to adopt new technologies. “We are witnessing traction in digital and product engineering segments. Cloud adoption among clients has increased as they want to protect market share by going digital,” said Sunil Sapre, executive director and chief financial officer.

Despite increase in salaries, the operating margin (EBIT margin) improved by 60 basis points to 12.7% helped by cost optimisation and improving revenue per client due to increasing size of the new deals. Sapre said that while the COVID driven cost savings in the form of lower travel expenses would be around for a few more quarters, the company is gearing up to accommodate cost increase once the situation returns to normal.

The provision for doubtful client accounts reduced during the quarter due to rising collection efficiency. As a result, the number of days sales were outstanding (DSO) improved to 57 from 63 in the previous quarter.

The company has actively reduced dependence on the US H1 Visa over the years by hiring more local talent. At present, among its US employees, 65% are hired locally which indicates visa dependency of 35%.

The higher growth visibility and earnings upgrade by brokerages are expected to support the stock’s trajectory in the coming months. “We upgrade our EPS estimates over FY21–23E by 6–8% as we gain further confidence on growth and margin momentum,” said Motilal Oswal Financial Services in a report. The brokerage has reiterated Persistent as the top buyacross its small-cap IT coverage.

( Originally published on Feb 08, 2021 )