The government has ruled out tweaking the inflation target under the monetary agreement framework between it and the RBI

C Ranganathan, former governor, Reserve Bank of India & Pronab Sen, former chief statistician, & country director, India Programme, International Growth Centre

C Ranganathan, former governor, Reserve Bank of India & Pronab Sen, former chief statistician, & country director, India Programme, International Growth Centre

The issue of whether the fiscal expansionary Budget for 2021-22 is inflationary has engaged experts and economists. While the government says it is not, experts are divided on this.

Former RBI governor C Rangarajan said the move would be inflationary to the extent that the central bank, indirectly or indirectly, would have to support government papers since the Centre would go for huge borrowing — Rs 12 trillion — in the next fiscal year over and above the Rs 12.80 trillion estimated for the current one.

Although the huge borrowing is also owing to the government cleaning up the books of Food Corporation of India (FCI) in the current fiscal year and the next one and the fiscal deficit would depend on revenue growth, it is the RBI that will have to support government bonds, said Rangarajan. To that extent, the programme would be inflationary, he said.

To a question whether the government and RBI should increase the inflation target from the current 4 per cent with a tolerance band of 2-6 percentage points when it comes up for review by March 31, Rangarajan said the target should be kept intact but flexibility should be provided in the case of fiscal deficit targets. The government has ruled out tweaking the inflation target under the monetary agreement framework between it and the RBI.

“Not necessarily,” said former chief statistician Pronab Sen when asked if the expansionary Budget will lead to price rise. Much of the widening of the fiscal deficit is happening due to past bills, said Sen, who is country director for the India Programme of the International Growth Centre.

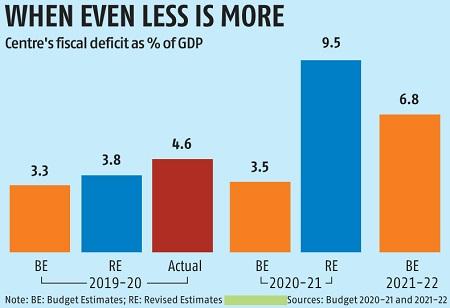

The government has brought in further transparency in the fiscal deficit by doing away with loans from the National Small Savings Fund (NSSF) to FCI from next fiscal year. The government will provide Rs 2.54 trillion to FCI next fiscal year, wiping out its arrears. So far, the government used to give loans from the NSSF to FCI, and they did not account for government expenditure. For instance, it has estimated this loan to FCI at over Rs 84,000 crore this fiscal year. In fact, it was over Rs 60,000 crore lower than the Budget Estimates. This, coupled with a food support scheme for the vulnerable sections during the Covid-induced lockdowns, led to a widening of the food subsidy by around Rs 3.1 trillion to Rs 4.2 trillion in the Revised Estimates of the current fiscal year against Rs 1.1 in the Budget Estimates.

This, coupled with a capital outlay, led to a projected widening of the deficit at a record 9.5 per cent of GDP in the current financial year compared to 3.5 per cent pegged under the Budget Estimates.

The government provided an NSSF loan in the range of Rs 70,000 crore-1.1 trillion to FCI in the previous four years. The food subsidy has been pegged at Rs 2.4 trillion next financial year. Besides the NSSF loan, extra-budgetary resources are being used for the Pradhan Mantri Awas Yojana-Rural to the tune of Rs 20,000 crore and the rural electrification programme Ujjwala (Rs 5,000 crore).

This might have also played its part in widening the fiscal deficit to 6.8 per cent of gross domestic product (GDP) next year.

Sen said clearing past dues of FCI and others would not lead to additional demand to a great extent. “Goods and services have been delivered. They are clearing the bills now,” he said. He said huge borrowing would have repercussions for interest rates, which have a relation with inflation only in the long run. If the benchmark rate on government papers goes up, inflation should rather come down, he said.

It should also be seen where increased expenditure is being incurred. If it goes mainly to capital expenditure in a situation where there is a lot of idle capacity in the economy, it may not lead to inflation.

ICRA Principal Economist Aditi Nayar said, “Given the output gap, we do not expect the budgetary allocations to be inflationary.”

Earlier Expenditure Secretary T V Somanathan had said: “The question is the level of idle capacity in the economy. So there’s a lot of unemployment. And there’s a lot of idle capacity in services and goods. In that situation, the macroeconomic fundamentals will indicate it is unlikely to be inflationary.”

India Ratings Chief Economist Devendra Pant pointed out while capital expenditure was projected to increase by 25 per cent to Rs 5.5 trillion next year from the revised estimate of Rs 4.4 trillion in 2020-21, revenue expenditure is projected to fall by 2.6 per cent from Rs 30.1 trillion to Rs 29.3 trillion during this period.

However, a better way could be to look at the ratio of revenue expenditure to GDP. The ratio remained in the range of 10.6 per cent to 12.2 per cent during 2013-14 to 2019-20. However, it is pegged at 15.5 per cent for the current financial year and 13.1 per cent for the next financial year, Pant said.

Nayar expected the retail price inflation rate to exceed the mid-point of 4 per cent, as mandated by the RBI’s monetary policy committee (MPC). The rate remained above 6 per cent for the most part of 2020, but fell to 4.59 per cent in December from 6.93 per cent in the previous month. The MPC expected it to be 5.2 per cent in the ongoing quarter, 5.2-5.0 per cent in the first half of the coming FY22, and 4.3 per cent in the third quarter (of FY22), with risks broadly balanced.