SynopsisThe Reserve Bank of India on Friday promised abundant liquidity to calm market nerves, after yields surged past 6% amid apprehension of extra supply of government papers.

Mumbai: The central bank’s decision to normalise the cash reserve ratio would reduce liquidity, but by doing it in a staggered manner and providing leeway to banks on marking to market their bond portfolio, it has ensured that there will be no cash crunch when the government is planning large borrowings.

The Reserve Bank of India on Friday promised abundant liquidity to calm market nerves, after yields surged past 6% amid apprehension of extra supply of government papers. But if its bond purchases of this fiscal is repeated at Rs 4 lakh crore and with another Rs 4 lakh crore of headroom for banks to buy bonds, these could negate any adverse impact of increased state borrowings.

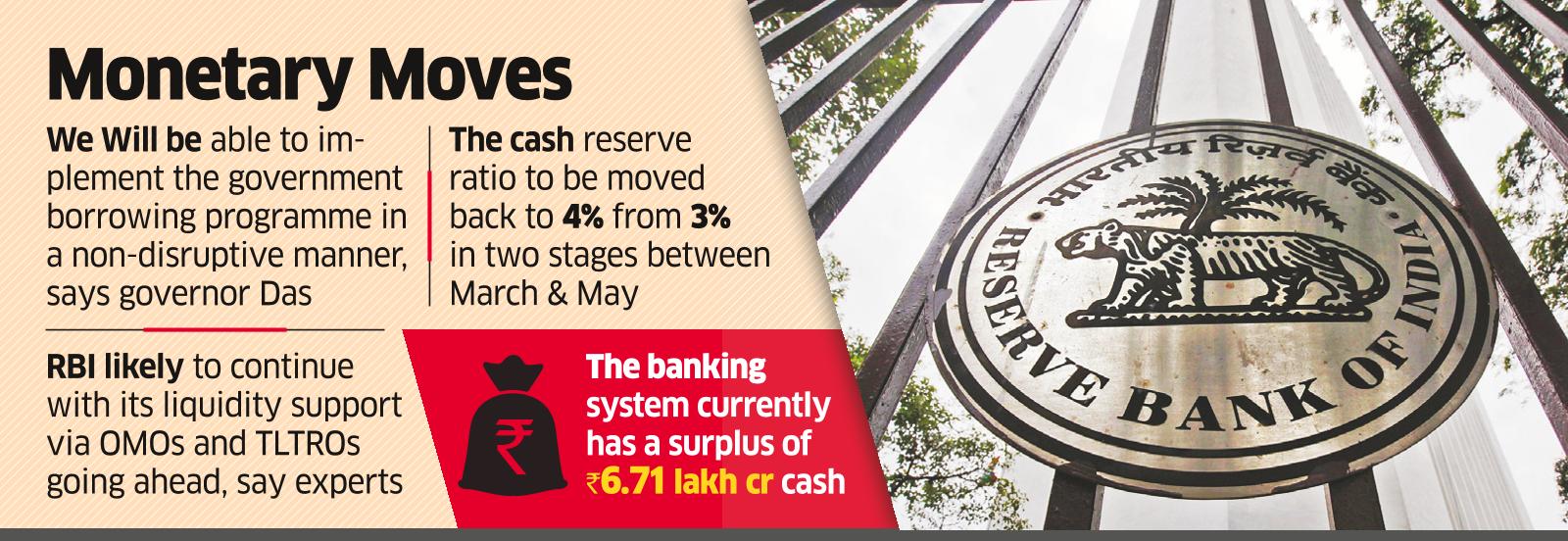

“Our liquidity stance continues to be accommodative and in consonance with the overall monetary policy stance,” said RBI governor Shaktikanta Das. “In 2021-22 we will be able to implement the government borrowing programme in a non-disruptive manner,” he said.

In September, the central bank had increased the limits under held to maturity (HTM) category to 22% from 19.5% of total deposits in respect of statutory liquidity ratio, or the portion of deposits banks are mandated to invest in sovereign bonds. Banks buying sovereign bonds can put the securities in this category where they don’t have to mark the value of the holding as per market fluctuations and make provisions.

Securities that qualify for the plan were to be acquired between September 1, 2020 and March 31, 2021. As per the original order, the 22% limit was to be in place till March 31, 2022.

The RBI has now extended the scope of the plan until the end of FY2023, while the papers can be acquired till March 31, 2022.

The RBI’s market operations have dispelled illiquidity fears and bolstered financial market sentiment, the governor said.

Convinced by the RBI’s communication and actions, market participants also responded synchronously and cooperatively.

In the G-sec market in which risk-free benchmarks evolve, a record low weighted average cost of 5.78% and an elongated weighted average maturity of 14.9 years testify the credibility of the monetary and liquidity management operations of the RBI.

The HTM limits would be restored to 19.5% in a phased manner starting from the quarter ending June 30, 2023. It is expected that banks will be able to plan their investments in SLR securities in an optimal manner with a clear glide path for restoration of HTM limits.

The cash reserve ratio, meanwhile, will be moved back to 4% from 3% in two stages between March and May.

“The announcements supporting liquidity in today’s policy is a positive for the bond markets,” said Madan Sabnavis, chief economist at CARE Ratings. The RBI is likely to continue with its liquidity support via OMOs and TLTROs going ahead.”

“Bond markets still seem to be cautious given the rise in yields post announcement of policy,” he said.

The banking system has a surplus of Rs 6.71 lakh crore cash.