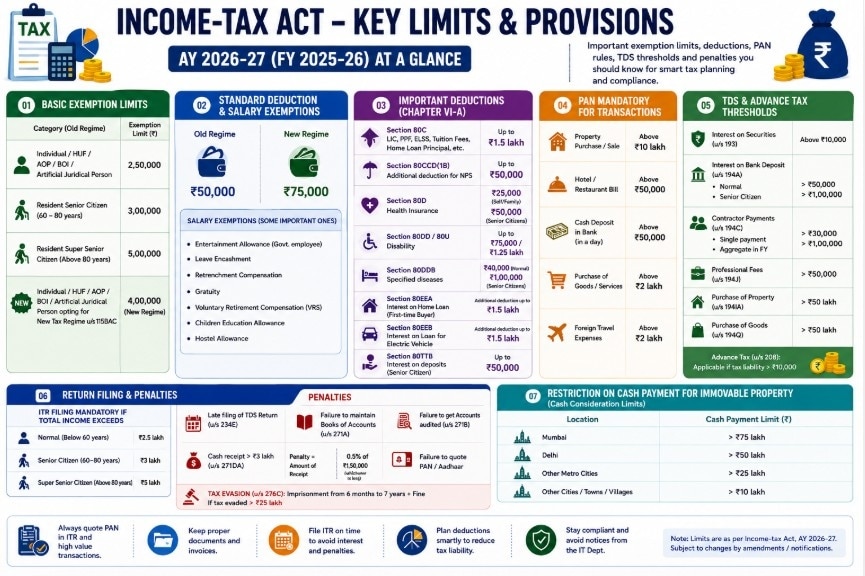

The Income-Tax framework for AY 2026-27 includes important rules on PAN-linked transactions, tax deductions, TDS thresholds and penalties that taxpayers should track carefully. From standard deduction changes to high-value transaction reporting, the updated limits could directly impact salaried individuals, senior citizens, businesses and investors.

Tax experts say taxpayers should carefully track these limits to avoid penalties, unnecessary notices and compliance issues while filing returns for AY 2026-27.

Tax experts say taxpayers should carefully track these limits to avoid penalties, unnecessary notices and compliance issues while filing returns for AY 2026-27.

The Income-Tax framework for Assessment Year (AY) 2026-27 includes several important rules covering exemption limits, PAN-linked transactions, tax deductions, TDS thresholds and penalties. For salaried individuals, business owners, senior citizens and investors, understanding these limits has become increasingly important as tax compliance norms tighten.Here’s a simple explainer on the key provisions taxpayers should know.

Advertisement

Basic tax exemption limits

The basic exemption limit refers to the level of income below which no income tax is payable.

Under the old tax regime:

- Individuals, HUFs, AOPs and BOIs get exemption up to ₹2.5 lakh

- Resident senior citizens aged 60–80 years get an exemption up to ₹3 lakh

- Super senior citizens above 80 years get an exemption of up to ₹5 lakh

- Under the new tax regime under Section 115BAC, the exemption limit is ₹4 lakh.

What is the Standard Deduction available?

The standard deduction continues to be available for salaried taxpayers and pensioners.

Old tax regime: ₹50,000

New tax regime: ₹75,000

The higher deduction under the new regime is aimed at making it more attractive for salaried taxpayers.

Advertisement

Which popular tax deductions continue?

Several deductions under Chapter VI-A remain available for eligible taxpayers.

Some key deductions include:

Section 80C

- Deduction up to ₹1.5 lakh for:

- PPF

- ELSS mutual funds

- LIC premiums

- Tuition fees

- Home loan principal repayment

- Section 80CCD(1B)

- Additional ₹50,000 deduction for National Pension System (NPS) investments.

- Section 80D

Health insurance deductions:

₹25,000 for self/family

₹50,000 for senior citizens

Section 80TTB

Senior citizens can claim deduction up to ₹50,000 on interest income from deposits.

The framework also includes deductions for disability support, specified diseases, affordable housing loans and electric vehicle loans.

When Is PAN Mandatory?

Advertisement

PAN quoting rules have become stricter for high-value transactions.

PAN is mandatory for:

Property purchase or sale above ₹10 lakh

Hotel or restaurant bills above ₹50,000

Cash deposits above ₹50,000 per day

Purchase of goods/services above ₹2 lakh

Foreign travel spending above ₹2 lakh

The government has expanded PAN-linked reporting to improve financial transparency and reduce unaccounted transactions.

What are the important TDS thresholds?

The chart also specifies important Tax Deducted at Source (TDS) limits.

Key examples:

- Bank interest for senior citizens above ₹50,000

- Professional fees above ₹50,000

- Contractor payments above ₹30,000 per transaction

- Property purchases above ₹50 lakh

Advance tax becomes applicable if the total tax liability exceeds ₹10,000 in a financial year.

Penalties explained

The Income-Tax framework also outlines penalties for delays and reporting failures.

Important penalties include:

- ₹200 per day for delayed TDS return filing

- ₹25,000 for failure to maintain books of accounts

- ₹10,000 penalty for failure to quote PAN or Aadhaar

- In serious cases involving tax evasion above ₹25 lakh, imprisonment ranging from six months to seven years may apply along with fines.

Restrictions on cash property transactions

The rules also impose limits on cash consideration in property transactions.

Thresholds include:

- ₹75 lakh in Mumbai

- ₹50 lakh in Delhi

- ₹25 lakh in other metro cities

- ₹10 lakh in smaller towns and villages

- Tax experts say taxpayers should carefully track these limits to avoid penalties, unnecessary notices and compliance issues while filing returns for AY 2026-27.