Listen to this article in summarized format

Geopolitical conflicts are usually analysed through the lens of diplomacy, security or energy markets. Yet, their ripple effects sometimes reach the everyday lives of ordinary individuals in unexpected ways. The ongoing tension involving the United States, Israel and Iran have periodically disrupted aviation routes across parts of West Asia. Major transit hubs such as Dubai and Abu Dhabi have experienced sudden airspace restrictions and flight cancellations, leaving many travellers stranded.

Income Tax Guide

Income Tax Union Budget FY 2026-27 LiveIncome Tax Slabs FY 2025-26Income Tax Calculator 2025

For Indians in the United Arab Emirates, including expatriates, professionals, and senior citizens from India visiting their children, such disruptions may initially seem little more than a travel inconvenience. However, in the realm of taxation, even a brief involuntary extension of stay can trigger consequences far beyond delayed flights. A deviation of just two or three days may alter a person’s tax residency status, reshape compliance obligations, and potentially expose foreign income to taxation.

The explanation lies in the way our nation’s tax system determines residential status.

The arithmetic

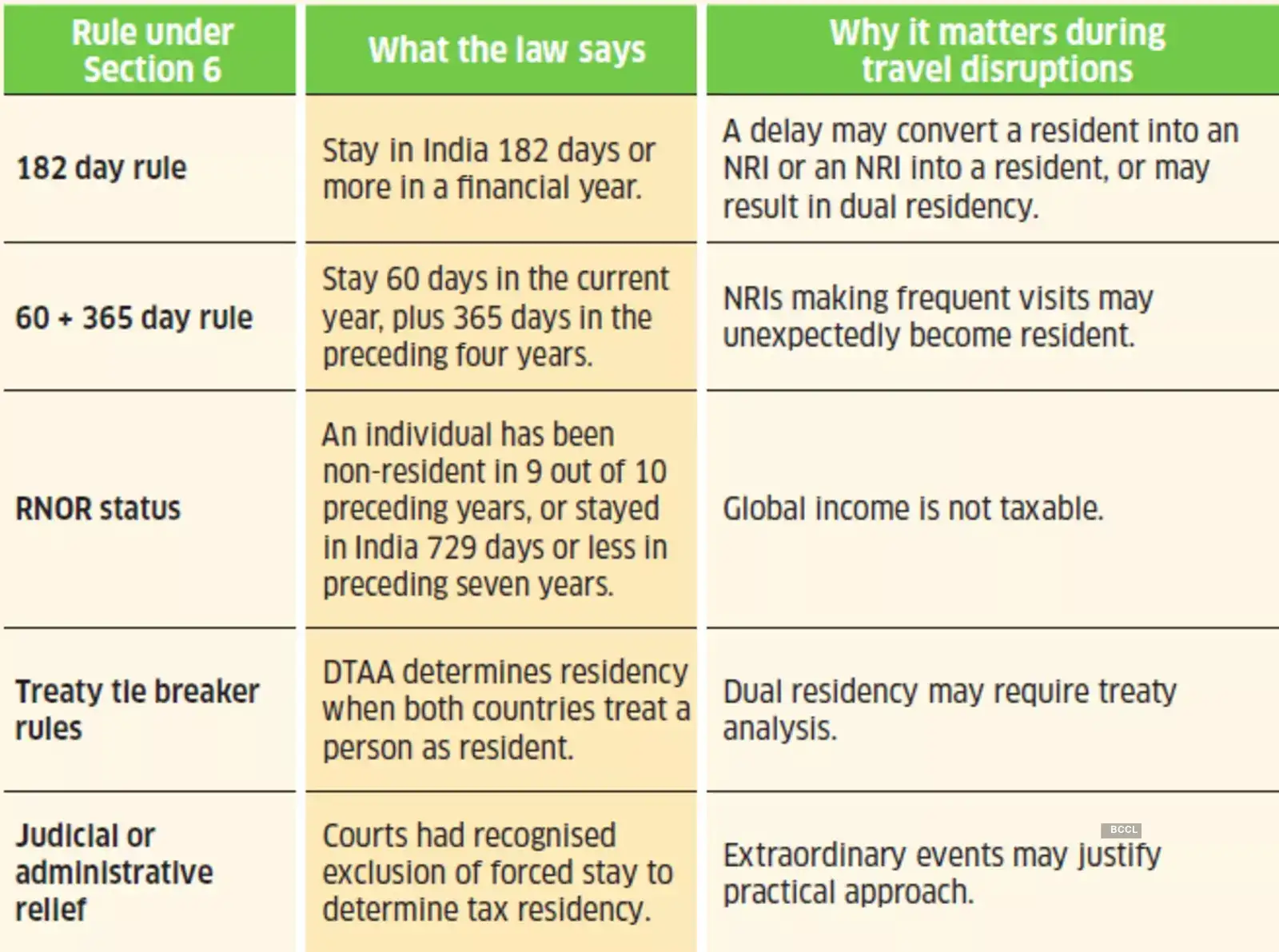

Under Section 6 of the Income Tax Act, residential status is determined primarily by the number of days spent in India during a financial year. The law lays down clear thresholds. An individual becomes a resident if they stay in India for 182 days or more during the year. Alternatively, residency may also arise if the individual stays in India for 60 days in that year and for 365 days or more during the four preceding financial years. These rules appear objective and straightforward. Under ordinary circumstances, they function smoothly. Yet, they are also rigid because the law counts days without examining the reasons behind them. This rigidity becomes evident when real-life travel disruptions collide with statutory thresholds.

Forced overstay & dual residency

Take Mr. A, a senior citizen who has lived in India for decades. He travels to Dubai on 2 September 2025 to visit his daughter and plans to return on 1 March 2026. As per the itinerary, his stay in Dubai would have lasted 181 days. However, the region’s airspace suddenly closes due to military escalation. Flights remain suspended and Mr. A manages to return only on 4 March, extending his stay in Dubai to 184 days.

This small shift in the calendar can lead to an unexpected outcome. Under the domestic tax framework of the UAE, physical presence exceeding 182 days may qualify an individual to obtain a tax residency certificate. Mr. A may, therefore, be treated as resident in the UAE. At the same time, he continues to qualify as a resident in India under Section 6 because his stay India during the year exceeds 60 days and his presence in India during the preceding four years exceeds 365 days. A three-day delay has suddenly created a situation of dual residency.

![]() |

|![]()

Upgrade to ETPrime for expert insights & exclusive stories

Special Offer ends in 00 : 03 : 29

![]() 1M+ Subscribers Trust ETPrime • 60k Joined Today

1M+ Subscribers Trust ETPrime • 60k Joined Today

Residency thumb rules for travellers

Treaty rules become relevant

Whenever a person is regarded as resident in two countries simultaneously, the Double Taxation Avoidance Agreement (DTAA) between the nations concerned helps resolve the issue. The India-UAE tax treaty contains tiebreaker provisions under Article 4 that determine the final residence for treaty purposes.

These provisions examine several connecting factors, including where a person’s permanent home is, where his personal and economic relations are strongest, where he habitually resides, and ultimately his nationality. If the issue still remains unresolved, the competent authorities of the two countries may need to settle the matter through a mutual agreement procedure. Thus, a situation that began with a simple family visit may suddenly involve treaty interpretation, documentation, and interaction with tax authorities in two jurisdictions, merely due to a brief and involuntary overstay abroad caused by airspace closures.

NRIs facing the reverse problem

The situation may be reversed for non-resident Indians (NRIs). Consider Mr. B, an NRI working in Abu Dhabi since 2021. He visits India on 3 January 2026 and plans to return on 1 March. His intended stay in India is 58 days, comfortably below the 60-day threshold under the alternative tax residency condition.

However, due to the same airspace disruptions, his departure is delayed till 4 March. His stay in India increases to 61 days, thereby crossing the statutory threshold. Mr. B frequently visits India to manage his personal investments; therefore, his cumulative stay in India over the preceding four financial years already exceeds 365 days. Consequently, once his stay in the relevant financial year crosses 60 days, the second limb of the residency test under the Income Tax Act becomes applicable. As a result, he becomes a resident in India for that financial year.

If he does not qualify as a ‘Resident but Not Ordinarily Resident’ (RNOR), his global income, including overseas salary, may become taxable in India. What was meant to be a short visit home may turn into a major tax event.

Courts and policy responses

Indian courts have recognised that such situations cannot always be evaluated just through mechanical arithmetic. In the case ‘CIT vs. Suresh Nanda’, the Delhi High Court ruled that presence in India caused by circumstances beyond an individual’s control should be excluded for determining residential status.

During the Covid-19 pandemic, similar concerns arose when overseas travel curbs left many stranded. The Central Board of Direct Taxes issued Circular No. 11 of 2020, allowing the exclusion of certain days of forced stay in India while computing residential status. Although limited in scope, it took into account the hassle caused by extraordinary events.

Learning curve

Residential status determines whether a taxpayer is liable only for Indian income or for global income, yet the current-day count rules can produce unintended results when travel disruptions occur. In extraordinary cases, tax residency should ideally reflect genuine economic connections rather than accidental travel delays. Until the law evolves, travellers would be well advised not to plan their visits on wafer-thin margins, like 181 or 58 days, because even a delay of two or three days can unexpectedly change the tax residency status.

The Author is Founder, Taxaaram India And Partner, SM Mohanka & Associate