Clipped from: https://taxguru.in/income-tax/assessment-framed-basis-mechanical-approval-u-s-153d-tenable.html

Saroj Bala Vs ACIT (ITAT Patna)

ITAT Patna held that consolidated approval under section 153D of the Income Tax Act granted in mechanical manner by JCIT without application of mind is invalid and hence assessment framed thereon is liable to be quashed.

Facts- A search & seizure and survey action have been conducted on 06/03/2019 by Investigation Directorate, Patna in the case of Shri Murlidhar Prasad. The search was also conducted on the Smt Saroj Bala and her business entities. Subsequently, notice u/s 153A of the Act was issued on 14/09/2020. The assessee filed return of income on 24/11/2020 u/s 153A of the Act. As per return of income of the assessee, the total income was Rs. 5,23,380/-. Finally, the Assessing Officer framed the assessment order vide order dated 24.08.2021 passed u/s.153A of the Act wherein an addition of Rs.7.00 lakhs was made by treating the same as unexplained money u/s.69A of the Act.

CIT(A) partly allowed the appeal. Being aggrieved, both revenue and assessee has preferred the present appeal.

Conclusion- Hon’ble Allahabad High Court in the case of Sapna Gupta, reported in [2023] 147 taxmann.com 288/[2022] SCC Online All 1294], the Hon’ble High Court has held that approval u/s.153D of the Act is to be granted by the competent authority on the draft assessment order for each year separately.

Hon’ble Orissa High Court in the case of M/s Serajuddin& Co. has held that the approval granted in mechanical manner by the competent authority without application of mind is not a valid approval. Therefore, considering the facts of the present case before us, in the light of the ratio laid down in the above decisions, we are inclined to quash the approval granted u/s 153D of the Act and also the assessment framed by the AO on the ground of being framed on the basis on invalid and mechanical approval granted u/s.153D of the Act.

FULL TEXT OF THE ORDER OF ITAT PATNA

These appeals are filed by three different assessees as well as by the revenue against the separate orders passed by the ld. CIT(A), Patna-3 for the assessment years 2012-2013, 2013-2014, 2014-2015, 20152016, 2016-2017, 2017-2018, 2018-2019 & 2019-2020, respectively. The assessee has also filed Cross Objection arising out of the appeal of the revenue in ITA No.295/PAT/2023 for A.Y.2012-2013.

2. Since the facts and circumstances involved in all the appeals are identical, therefore, for the sake of convenience, all the appeals & cross objection are clubbed together and disposed off by this consolidated order.

3. First we shall decide the appeal of the assessee in ITA No.234/PAT/2024 filed for A.Y.2015-2016 and the outcome of the same shall apply, mutatis mutandis, to the other appeals also.

4. At the time of hearing, ld. counsel pressed the legal issue raised in Ground No.6 in ITA No.234/PAT/2024 for A.Y.2015-2016 which reads as under :-

“That the Ld. CIT(A) has gross erred in law in not considering that the ld. JCIT has granted approval u/s.153D of the Act on assessment order in a mechanical fashion and without proper application of mind.

5. Brief facts of the case are that a search & seizure and survey action have been conducted on 06/03/2019 by Investigation Directorate, Patna in the case of Shri Murlidhar Prasad. The search was also conducted on the Smt Saroj Bala and her business entities. Consequently, a warrant of authorization under section 132(1) of the Act, was issued to assessee and others on 06/03/2019. Smt. Saroj Bala was director in two companies M/s Lovely Rani Constructions Private Limited (LRCPL) and Janardana Pharmacy Private Limited (JPPL). The assessee Smt. Saroj Bala is wife of Shri Murlidhar Prasad. Subsequently, notice u/s 153A of the Act was issued on 14/09/2020. The assessee filed return of income on 24/11/2020 u/s 153A of the Act. As per return of income of the assessee, the total income was Rs. 5,23,380/-. Pertinent to mention that the assessee had filed return of income originally u/s 139(1) of the Act declaring total income Rs.5,23,380/-. Thereafter the Assessing Officer issued notice u/s 142(1) of the Act along with questionnaire to the assessee on 26/11/2020, which was duly served on the assessee calling upon the assessee to furnish various details, information and explanations qua the issues involved qua which the incriminating materials were found and seized during search action. Finally, the Assessing Officer framed the assessment order vide order dated 24.08.2021 passed u/s.153A of the Act wherein an addition of Rs.7.00 lakhs was made by treating the same as unexplained money u/s.69A of the Act.

6. Aggrieved with the assessment order, the assessee filed an appeal before the ld.CIT(A) on legal issues as well as on merit, however, the ld. CIT(A) did not adjudicate the legal issue raised by the assessee challenging the validity of the assessment framed by the Assessing Officer u/s.153A of the Act on the ground of being based upon the invalid and mechanical approval granted by the ld. JCIT, Central Range-1, Patna u/s 153D of the Act.

7. Ld. AR vehemently submitted before us that the assessment framed by the Assessing Officer u/s.153A of the Act dated 24.08.2021 was invalid as the same is based upon the invalid and mechanical approval granted by the JCIT u/s 153D of the Act. The ld.AR submitted that the JCIT is supposed to grant approval after going through the facts of the case as placed before him, however, in the present case, the JCIT has given a mechanical approval without application of mind by giving consolidated approval for all the assessment years i.e. for A.Y.2013-2014 to 2019-2020 u/s.153D of the Act. The ld. Counsel submitted that the machanism of obtaining approval from the senior authority has been provided in the Act to safeguard against any misuse of power by the lower authority /assessing officer. The ld AR submitted that if there is any wrong doing or wrong appreciation of facts or any wrong application of law by the assessing officer, then the approving authority while granting sanction has to check that with due application of mind and take the necessary steps to correct the mistake on the part of the AO. If the approving authority grants approval in mechanical manner without application of mind, the very purpose of the approval mechanism would be defeated. Ld.counsel submitted that the order passed by the Assessing Officer on the basis of the said approval is invalid and assessment order passed consequently would be invalid and nullity. In defence of his arguments relied on serious of decisions, which are as under :-

1. Arch Pharmalabs Ltd. 2021-TIOL-1264-ITAT-Mumbai

2. Shreelekha Damani v/s. DCIT 173 TTJ 332 (Mum) = 2015-TIOL-2170-ITAT-Mum

3. Pr. CIT v/s. Smt. Shreelekha Damani 2018-TIOL-2516-HC-MUM-IT

4. Sanjay Duggal & Others 2021-TIOL-148-ITAT Del

5. Inder International v/s ACIT [ITA 1573/CHANDI/2018]

6. Navin Jain & Others vs. CIT 91 ITR (Tribunal) 682

7. Pr. CIT vs. Shiv Kumar Nayyar in ITA No. 285/2024 and CM Application No. 28994/2024 as reported in Taxsutra 343-HC-2024-Delhi.

8. Pr. CIT vs. Anuj Bansal [ITA 368/2023]

9. Smt. Sapna Gupta, Kanpur vs DCIT Lucknow ITAT (2021)

10. Hon’ble Allahabad High Court in the case of Pr. CIT vs. Sapna Gupta

11. ACIT vs. Sirajuddin and Co. [2023 SCC Online Ori 992]

12. SLP Dismissed in the case of Serajuddin and Co.

8. Per Contra, ld. CIT-DR vehemently opposed the arguments of the ld. counsel and submitted that there was no question of any invalid or mechanical approval of any kind whatsoever by the JCIT. Ld.CIT-DR submitted that if the assessee is same and common issues are involved then it is quite feasible that it approval could be given by way of consolidated order u/s 153D of the Act. The ld.CIT-DR submitted that the Addl.CIT/JCIT are always involved in search assessment proceedings right from the beginning to the end till the assessment is framed and each and every step/action of the department is proposed and taken under their guidance. In other words, the whole proceedings are monitored by the higher authorities. Therefore, to say that the approval given by the JCIT is mechanical, is bereft of any merit and may be dismissed summarily.

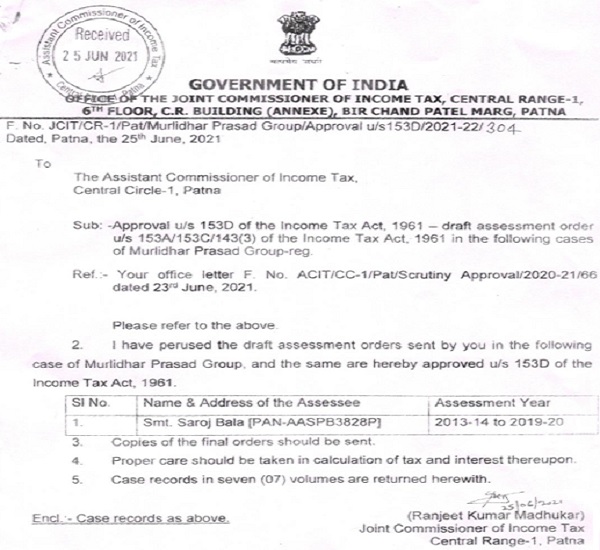

9. After hearing the rival contentions and perusing the material available on record, we find that in this case a search was conducted by the Investigation Wing Patna on the assessee on 6.3.2019 and accordingly assessment was framed u/s.153A of the Act vide order dated 24.08.2021. The legal issue before us raised by the assessee is as to whether the common approval granted by the JCIT, Central Range-1 Patna for all the assessment years involved right from A.Y.2013-2014 to 2019-2020 is invalid, mechanical and given without application of mind. For the sake of ready reference, we extract the copy of approval granted u/s.153D of the Act as under :-

10. A perusal of the above said approval u/s.153D of the Act dated 25.06.2021 reveals that the approval has been given in case of Saroj Bala from A.Y.2013-2014 to A.Y.2019-2020 by a consolidated order. In our opinion, the approval has to be granted by the JCIT after perusing the draft assessment order placed before him by the Assessing Officer for each assessment year separately, however, in the present case a consolidated approval was granted for all the assessment years. In our opinion, the JCIT is supposed to exercise with utmost caution and care while granting approval u/s 153D of the Act as this is a safeguard provided in the Act so that if any wrongs committed by the Assessing Officer, the same would be taken care of while granting the approval and set right accordingly. However, granting approval in a mechanical manner without application of mind would defeat the very purpose of safeguard provided in the Act. In our opinion the mechanical approval granted without application of mind is invalid. In these circumstances, we are not in a position to sustain the order passed by the Assessing Officer which is based on invalid approval granted u/s.153D of the Act. The case of the assessee is squarely covered by the decision of Hon’ble Delhi High Court in the case of Shiv Kumar Nayyar, reported in [2024] 163 taxmann.com 9 (Delhi High Court), wherein the Hon’ble Delhi High Court has held as under:-

1. The solitary question which stands posted before us for adjudication pertains to whether, under the facts of the present case, the specified authority has granted approval in accordance with the mandate of Section 153D of the Income Tax Act, 1961 [“Act”]?

2. The instant appeal, at the instance of the Revenue, impugns the order of the Income Tax Appellate Tribunal [“ITAT”] dated 26.07.2023, whereby, the assessment order has been held to be illegal for lack of appropriate approval under Section 153D of the Act.

3. As per record, the appeal pertains to Assessment Year [“AY”] 2015-16. The dispute essentially emanates from a search and seizure operation which was conducted on 18.11.2016 under Section 132 of the Act by the Investigation Wing in Nayyar Group of cases, including the residential premises of the assessee. The said operation was followed by a survey operation under Section 133A of the Act.

4. Pursuant to the aforenoted search, an order under Section 127 of the Act was passed which led to centralization of the case of the assessee. Consequently, a notice under Section 153A of the Act was issued to the assessee on 22.09.2017. In response to the said notice, the assessee filed its Income Tax Return [“ITR”] on 14.08.2018, declaring an income of ₹18,48,450/- and the same was processed as per the provisions of Section 143(1) of the Act. Subsequently, the case of the assessee was picked up for scrutiny assessment and a notice under Section 143(2) was duly issued.

5. Thereafter, on 30.12.2018, an assessment order was passed by the assessing officer [“AO”] under Section 153A read with Section 143(3) of the Act, whereby, the total taxable income of the assessee was pegged at ₹5,19,85,970/-. Being aggrieved by the additions made by the AO, the assessee preferred an appeal before the Commissioner of Income Tax (Appeals) [“CIT(A)”]. Vide order dated 09.07.2021, the CIT(A), while partly allowing the appeal of the assessee, deleted certain additions made by the AO.

6. However, the Revenue preferred an appeal against the order of the CIT(A) before the ITAT, wherein, the approval under Section 153D of the Act by the competent authority was found to be flawed and mechanical in nature and as a sequitur, the entire search assessment was declared to be illegal.

7. Learned counsel for the Revenue submitted that there is no infirmity in the approval granted by the concerned authority and therefore, the ITAT has erred in declaring the assessment order to be invalid. He contended that merely because the approval was granted on the same day when the draft assessment orders were sent by the AO, the same cannot be a ground to hold that the approval was accorded without any application of mind. According to him, since the authority granting approval has been involved in the assessment proceedings from the initial days, the same cannot be divested of its right to accord approval on the same day. He, therefore, mainly proposed the following substantial question of law for our consideration:-

“Whether the ITAT has erred in law, in considering the Assessment Order under Section 153A of the Act, as invalid and bad in law by stating that the approval granted by the Range head under section 153D of the Act is void as the same was granted in a mechanical manner without application of mind?”

8. Per contra, learned counsel for the assessee vehemently opposed the submissions. He submitted that the competent authority has granted approval in a mechanical manner inasmuch as the draft assessment orders for multiple AYs were accorded approval on the same date on which they were sent, which reflects a complete non- application of mind. It was, therefore, contended that the ITAT has correctly relied upon the decision of this Court in PCIT v. Anuj Bansal [ITA 368/2023] as well as various other High Courts to reach the conclusion that the approval was given in the teeth of the provisions of Section 153D of the Act.

9. We have heard the learned counsels appearing on behalf of the parties and perused the record.

10. Before embarking upon the analysis of the factual scenario of the instant appeal, we deem it apposite to examine the underlying intent of the relevant provision of the Act i.e., Section 153D, which is culled out as under:-

“153-D. Prior approval necessary for assessment in cases or requisition.–No order of assessment or reassessment shall be passed by an Assessing Officer below the rank of Joint Commissioner in respect of each assessment year referred to in clause (b) of [sub-section (1) of Section 153-A] or the assessment year referred to in clause (b) of sub-section (1) of Section 153-B, except with the prior approval of the Joint Commissioner :

Provided that nothing contained in this section shall apply where the assessment or reassessment order, as the case may be, is required to be passed by the Assessing Officer with the prior approval of the [Principal Commissioner or Commissioner] under sub-section (12) of Section 144-BA.“

11. A plain reading of the aforesaid provision evinces an uncontrived position of law that the approval under Section 153D of the Act has to be granted for “each assessment year” referred to in clause (b) of sub-section (1) of Section 153A of the Act. It is beneficial to refer to the decision of the High Court of Judicature at Allahabad in the case of PCIT v. Sapna Gupta [2022 SCC Online All 1294] which captures with precision the scope of the concerned provision and more significantly, the import of the phrase- “each assessment year” used in the language of Section 153D of the Act. The relevant paragraphs of the said decision are reproduced as under:-

“13. It was held therein that if an approval has been granted by the Approving Authority in a mechanical manner without application of mind then the very purpose of obtaining approval under Section 153D of the Act and mandate of the enactment by the legislature will be defeated. For granting approval under Section 153D of the Act, the Approving Authority shall have to apply independent mind to the material on record for “each assessment year” in respect of “each assessee” separately. The words ‘each assessment year’ used in Section 153D and 153A have been considered to hold that effective and proper meaning has to be given so that underlying legislative intent as per scheme of assessment of Section 153A to 153D is fulfilled. It was held that the “approval” as contemplated under 153D of the Act, requires the approving authority, i.e. Joint Commissioner to verify the issues raised by the Assessing Officer in the draft assessment order and apply his mind to ascertain as to whether the required procedure has been followed by the Assessing Officer or not in framing the assessment. The approval, thus, cannot be a mere formality and, in any case, cannot be a mechanical exercise of power.

***

19. The careful and conjoint reading of Section 153A(1) and Section 153D leave no room for doubt that approval with respect to “each assessment year” is to be obtained by the Assessing Officer on the draft assessment order before passing the assessment order under Section 153A.“

[Emphasis supplied]

12. It is observed that the Court in the case of Sapna Gupta (supra) refused to interdict the order of the ITAT, which had held that the approval under Section 153D of the Act therein was granted without any independent application of mind. The Court took a view that the approving authority had wielded the power to accord approval mechanically, inasmuch as, it was humanly impossible for the said authority to have perused and appraised the records of 85 cases in a single day. It was explicitly held that the authority granting approval has to apply its mind for “each assessment year” for “each assessee” separately.

13. Reliance can also be placed upon the decision of the Orissa High Court in the case of Asst. CIT v. Serajuddin and Co. [2023 SCC Online Ori 992] to understand the exposition of law on the issue at hand. Paragraph no.22 of the said decision reads as under:-

“22. As rightly pointed out by learned counsel for the assessee there is not even a token mention of the draft orders having been perused by the Additional Commissioner of Income-tax. The letter simply grants an approval. In other words, even the bare minimum requirement of the approving authority having to indicate what the thought process involved was is missing in the aforementioned approval order. While elaborate reasons This is a digitally signed order.

The authenticity of the order can be re-verified from Delhi High Court Order Portal by scanning the QR code shown above. The Order is downloaded from the DHC Server on 20/05/2024 at 21:34:51 need not be given, there has to be some indication that the approving authority has examined the draft orders and finds that it meets the requirement of the law. As explained in the above cases, the mere repeating of the words of the statute, or mere “rubber stamping” of the letter seeking sanction by using similar words like “seen” or “approved” will not satisfy the requirement of the law. This is where the Technical Manual of Office Procedure becomes important. Although, it was in the context of section 158BG of the Act, it would equally apply to section 153D of the Act. There are three or four requirements that are mandated therein,

(i) the Assessing Officer should submit the draft assessment order “well in time”. Here it was submitted just two days prior to the deadline thereby putting the approving authority under great pressure and not giving him sufficient time to apply his mind ; (ii) the final approval must be in writing ; (iii) the fact that approval has been obtained, should be mentioned in the body of the assessment order.”

[Emphasis supplied]

14. During the course of arguments, learned counsel for the assessee apprised this Court that the Special Leave Petition preferred by the Revenue against the decision in the case of Serajuddin (supra), came to be dismissed by the Supreme Court vide order dated 28.11.2023 in SLP (C) Diary no. 44989/2023.

15. A similar view was taken by this Court in the case of Anuj Bansal (supra), whereby, it was reiterated that the exercise of powers under Section 153D cannot be done mechanically. Thus, the salient aspect which emerges from the abovementioned decisions is that grant of approval under Section 153D of the Act cannot be merely a ritualistic formality or rubber stamping by the authority, rather it must reflect an appropriate application of mind.

16. In the present case, the ITAT, while specifically noting that the approval was granted on the same day when the draft assessment orders were sent, has observed as under:-

“10. We have gone through the approval granted by the ld. Addl. CIT on 30.12.2018 u/s 153D of the Act which is enclosed at page 36 of the paper book of the assessee. The said letter clearly states that a letter dated 30.12.2018 was filed by the ld. AO before the ld. Addl. CIT seeking approval of draft assessment order u/s 153D of the Act. The ld. Addl. CIT has accorded approval for the said draft assessment orders on the very same day i.e., on 30.12.2018 for seven assessment years in the case of the assessee and for seven assessment years in the case of Smt. Neetu Nayyar. It is also pertinent in this regard to refer to pages 68 and 69 of the paper book which contains information obtained by Smt. Neetu Nayyar from Central Public Information Officer who is none other than the ld. Addl. Commissioner of Income-tax, Central Range-S, New Delhi, under Right to Information Act, wherein, it reveals that the ld. Addl. CIT had granted approval for 43 cases on 30.12.2018 itself. This fact is not in dispute before us. Of these 43 cases, as evident from page 36 of the paper book which contains the approval u/s 153D, 14 cases pertained to the assessee herein and Smt. Neetu Nayyar. The remaining cases may belong to some other assessees, which information is not available before us. In any event, whether it is humanly possible for an approving authority like ld. Addl. CIT to grant judicious approval u/s 153D of the Act for 43 cases on a single day is the subject matter of dispute before us. Further, section 153D provides that approval has to be granted for each of the assessment year whereas, in the instant case, the ld. Addl. CIT has granted a single approval for all assessment years put together.”

17. Notably, the order of approval dated 30.12.2020 which was produced before us by the learned counsel for the assessee clearly signifies that a single approval has been granted for AYs 2011-12 to 2017-18 in the case of the assessee. The said order also fails to make any mention of the fact that the draft assessment orders were perused at all, much less perusal of the same with an independent application of mind. Also, we cannot lose sight of the fact that in the instant case, the concerned authority has granted approval for 43 cases in a single day which is evident from the findings of the ITAT, succinctly encapsulated in the order extracted above.

18. Therefore, under the facts of the present case, considering the foregoing discussion and the enunciation of law settled through judicial pronouncements discussed hereinabove, we are unable to find any substantial question of law which would merit our consideration.

19. Consequently, the appeal stands dismissed. Pending application(s), if any, are also disposed of.

11. Similarly the Hon’ble Allahabad High Court in the case of Sapna Gupta, reported in [2023] 147 taxmann.com 288/[2022] SCC Online All 1294], the Hon’ble High Court has held that approval u/s.153D of the Act is to be granted by the competent authority on the draft assessment order for each year separately. The operative part of the said judgment is extracted below :-

Considering the submissions of the learned counsel for the parties and having perused the order of the Tribunal, in view of the undisputed facts before us about the manner in which the approval to the draft assessment order was granted under Section 153D for the assessment proceedings, by a letter dated 30.12.2017 in 85 cases placed before the approving authority in a single day, we are required to examine as to whether a substantial question of law arises for consideration before us so as to admit the present appeal.

To answer the same, we are required to go through the relevant provisions of the Income Tax Act. Section 132 provides the procedure for search and seizure operations in consequence of the information in possession of the Income Tax Authorities. Section 153A prescribes assessment in case of search or requisition. Section 153A provides that in the case of a person where a search is initiated under Section 132, the Assessing Officer shall issue notice to such person requiring him to furnish within such period, as may be specified in the notice, the return of income in respect of each assessment year falling within six assessment years (and for the relevant assessment year or years) referred to in clause (b), in the prescribed form and verified in the prescribed manner and setting forth such other particulars as may be prescribed and the provisions of this Act shall, so far as may apply accordingly as if such return were a return required to be furnished under Section 139.

Section 153D of the Act relevant for our purposes is to be noted hereinunder:

“Prior approval necessary for assessment in cases of search or requisition.

153D. No order of assessment or reassessment shall be passed by an Assessing Officer below the rank of Joint Commissioner in respect of each assessment year referred to in clause (b) of [subsection (1) of] section 153A or the assessment year referred to in clause (b) of sub-section (1) of section 153B, except with the prior approval of the Joint Commissioner.”

Provided that nothing contained in this section shall apply where the assessment or reassessment order, as the case may be, is required to be passed by the Assessing Officer with the prior approval of the [Principal Commissioner or] Commissioner under sub-section (12) of section 144BA.

The Tribunal while quashing the assessment order had relied upon its earlier decision in Navin Jain and Others (Supra) wherein a detailed discussion has been made with regard to the requirement of prior approval of superior authority on the draft assessment order under Section 153D, before passing the assessment order by the Assessing Officer. It was noted that the word ‘approval’ though has not been defined in the Income Tax Act but the general meaning of the word ‘approval’ in Black’s Law Dictionary, 6th Edition was to be seen. The decision of the Apex Court in Vijayadevi Naval Kishore Bharatia vs. Land Acquisition Officer (2003) 5 SCC 83 wherein the distinction between Approving Authority and Appellate Authority was drawn, had been noted. The decision of the High Court of Gauhati in Dharampal Satyapal Ltd. vs. Union of India (2019) 366 ELT 253 (Gau.) has been noted to record that grant of approval means due application of mind on the subject matter approved which satisfies all the legal and procedural requirements. There is an exhaustive discussion on the requirement of prior approval under Section 153D of the Act and it was noted that the requirement of approval cannot be treated as mere formality and the mandate of the Act that the Approving Authority has to act in a judicious manner by due application of mind in a manner of a quasi judicial authority, has been considered.

It was held therein that if an approval has been granted by the Approving Authority in a mechanical manner without application of mind then the very purpose of obtaining approval under Section 153D of the Act and mandate of the enactment by the legislature will be defeated. For granting approval under Section 153D of the Act, the Approving Authority shall have to apply independent mind to the material on record for “each assessment year” in respect of “each assessee” separately. The words ‘each assessment year’ used in Section 153D and 153A have been considered to hold that effective and proper meaning has to be given so that underlying legislative intent as per scheme of assessment of Section 153A to 153D is fulfilled. It was held that the “approval” as contemplated under 153D of the Act, requires the approving authority, i.e. Joint Commissioner to verify the issues raised by the Assessing Officer in the draft assessment order and apply his mind to ascertain as to whether the required procedure has been followed by the Assessing Officer or not in framing the assessment. The approval, thus, cannot be a mere formality and, in any case, cannot be a mechanical exercise of power.

It was noted that the obligations of the approval of the Approving Authority serves two purposes:

i. On the one hand, he has to apply his mind to ensure the interest of the revenue against any omission or negligence by the Assessing Officer in taxing right income in the hands of right person and in right assessment year.

ii. On the other hand, superior authority is also responsible and duty-bound to do justice with the tax-payer by granting protection against arbitrary or creating baseless tax liability on the assessee.

The Tribunal has further noted that the provisions contained in Sections 153A to Section 153D provide for separate notice to be given to assessee for assessment for each year as specified in Section 153A of the Act; the assessee has to file separate ITR for each year as specified in Section 153A of the Act; separate assessment orders are to be passed for each year as specified in Section 153A of the Act.

It was observed that this is an important concept mentioned in Section 153A of the Act, which is peculiar to the scheme of the said Section. Keeping in view of this basic fundamental features of Section 153A, if Section 153D is scrutinized, then, it would become manifest that an important phrase is employed in the text of Section 153D, which is “each assessment year”. The reading of the provisions in Section 153A and 153D conjointly makes it clear that separate approval of draft assessment order for each year is to be obtained under Section 153D of the Income Tax Act. In its erudite judgement with the discussion on the legislative intent of Section 153A to 153D and the meaning of the “approval” as defined in Black’s Law Dictionary as also the decisions of the Apex Court in the case of Sahara India vs. CIT and Others (2008) 300 JTR 403 (SC) where the discussion on the requirement of prior approval of Chief Commissioner or Commissioner in terms of provision of Section 142(2A) of the Act had been made, it was noted that the Apex Court has held therein that the requirement of previous approval of the Chief Commissioner or Commissioner in terms of the said provision being an in-built protection against arbitrary or unjust exercise of power by the Assessing Officer casts a very heavy duty on the said high ranking authority to see that the approval envisaged in the section is not turned into an empty ritual. The Apex Court has held therein that the approval must be granted only on the basis of material available on record and the approval must reflect the application of mind to the facts of the case.

The above discussion made in the judgement of Tribunal dated 3.08.2021 in the case of Navin Jain Vs. Dy. C.I.T. (Supra) has been relied by the Tribunal, in the instant case, to arrive at the conclusion that the mechanical approval under Section 153D of the Act would vitiate the entire proceedings in the instant case.

For the reasoning given in the case of Navin Jain (Supra), as extracted in the impugned order passed by the Tribunal, as noted above, there cannot be any two opinion to the requirement of prior approval of the Joint Commissioner to the draft assessment order prepared by the Assessing Officer, as per the mandate of Section 153D of the Income Tax Act.

The approval of draft assessment order being an in-built protection against any arbitrary or unjust exercise of power by the Assessing Officer, cannot be said to be a mechanical exercise, without application of independent mind by the Approving Authority on the material placed before it and the reasoning given in the assessment order. It is admitted by Sri Gaurav Mahajan, learned counsel for the appellant-revenue that the approval order is an administrative exercise of power on the part of the Approving Authority but it is sought to be submitted that mere fact that the approval was in existence on the date of the passing of the assessment order, it could not have been vitiated. This submission is found to be a fallacy, in as much as, the prior approval of superior authority means that it should appraise the material before it so as to appreciate on factual and legal aspects to ascertain that the entire material has been examined by the Assessing Authority before preparing the draft assessment order. It is trite in law that the approval must be granted only on the basis of material available on record and the approval must reflect the application of mind to the facts of the case. The requirement of approval under Section 153D is pre-requisite to pass an order of assessment or reassessment.

Section 153D requires that the Assessing Officer shall obtain prior approval of the Joint Commissioner in respect of “each assessment year” referred to in Clause (b) of sub-section (1) of Section 153A which provides for assessment in case of search under Section 132. Section 153A(1)(a) requires that the assessee on a notice issued to him by the Assessing Officer would be required to furnish the return of income in respect of “each assessment year” falling within six assessment years (and for the relevant assessment year or years), referred to in Clause (b) of subsection (1) of Section 153A. The proviso to Section 153A further provides for assessment of the total income in respect of each assessment year falling within such six assessment years (and for the relevant assessment year or years).

The careful and conjoint reading of Section 153A(1) and Section 153D leave no room for doubt that approval with respect to “each assessment year” is to be obtained by the Assessing Officer on the draft assessment order before passing the assessment order under Section 153A.

In the instant case, the draft assessment order in 85 cases, i.e. for 85 assessment years placed before the Approving Authority on 30.12.2017 was approved on same day i.e. 30.12.2017, which not only included the cases of respondent-assessee but the cases of other groups as well. It is humanly impossible to go through the records of 85 cases in one day to apply independent mind to appraise the material before the Approving Authority. The conclusion drawn by the Tribunal that it was a mechanical exercise of power, therefore, cannot be said to be perverse or contrary to the material on record.

As the facts are admitted before us, the questions of law framed on the factual issues related to the findings recorded by the Assessing Officer are not open to agitate within the scope of the present appeal being in the nature of second appeal. No substantial question of law arises for consideration before us.

The Appeal is dismissed being devoid of merit.

12. Similar position has been laid down in various decisions passed by various Hon’ble High Courts and coordinate benches of the Tribunal. Similarly Hon’ble Orissa High Court in the case of M/s Serajuddin& Co., reported in 454 ITR 312 (Orissa-HC), has held as under :-

21. It is seen that in the present case, the AO wrote the following letter seeking approval of the Additional CIT:

GOVERNMENT OF INDIA

OFFICE OF THE ASST. COMMISSIONER OF INCOME TAX,

CIRCLE-1(2), BHUBANESWAR

No. ACIT/C-1(2)//Approval/2010-11/5293 Dated, Bhubaneswar, the 27/29th December, 2010

To

The Addl. Commissioner of Income-tax,

Range-1, Bhubaneswar.

Sub: Approval of draft orders u/s 153D of the I.T. Act 1961 in the case of M/s. Serajuddin & Co. 19A, British India Street, Kolkata (in Serajuddin Group of Cases)- matter regarding.

Sir, Enclosed herewith kindly find the draft orders u/s 153A of the I.T.Act, 1961 along with assessment records in the case of M/s Serajuddin & Co., 19A, British India Street, Kolkata for kind perusal and necessary approval u/s.153D.

No. Name of the assessee Section under which order passed Asst. Year

1. M/s Serajudding & Co, 19A, u/s.153A/143(3)/144/145(3) 2003-04 British India Street, Kolkata

2. -do- -do- 2004-05

3. -do- -do- 2005-06

4. -DO- -do- 2006-07

5. -DO- -DO- 2007-08

6. -DO- -DO- 2008-09

3. -DO- U/s.143(3)/144/153B(B)/145(3) 2009-10 3) The above cases will be barred by limitation on 31.12.2010.

Encl: As above

Yours faithfully,

Sd/-

Asst. Commissioner of Income-tax,

Circle-1(2), Bhubaneswar

OFFICE OF THE ADDL. COMMISSIONER OF INCOME TAX, 3

Floor, Range-1, Bhubaneswar

No. Addl. CIT/R-1/BBSR/SD/2010-11/5350 Dated, Bhubaneswar, the 30th December, 2010 ITA Nos.284-290/CTK/2025

To

The Assistant Commissioner of Income Tax,

Circle-1(2), Bhubaneswar.

Sub: Approval u/s 153D-in the case of M/s Serajuddin & Co., 19A, British India Street, Kolkata-Matter regarding.

Ref: Draft Orders u/s 153A/143(3)/144 for the A.Y. 2003- 04 to 2008-09 u/s.143(3)/153B (b)/144 of the A.Y.2009-10 in the case of above mentioned assessee.

Please refer to the above The draft orders u/s 153A/143(3)/144 for the A.Y. 2003-04 to 2008-09 and u/s. 143(3)/153B(b)/144 for the A.Y. 2009-10 submitted by you in the above case for the following assessment years are hereby approved:

| Assessment Year(Rs.) | Income Determined |

| 2003-04 | 11,66,22,771 |

| 2004-05 | 36,46,80,016 |

| 2005-06 | 65,70,12,805 |

| 2006-07 | 60,02,65,791 |

| 2007-08 | 130,03,13,307 |

| 2008-09 | 274,68.87,069 |

| 2009-10 | 301,17,05,952 |

You are requested to serve these orders expeditiously on the assessee, submit a copy of final order to this office for record.

Sd/-

Addl. Commissioner of Income

Tax, Range-1, Bhubaneswar

22. As rightly pointed out by learned counsel for the Assessee there is not even a token mention of the draft orders having been perused by the Additional CIT. The letter simply grants an approval. In other words, even the bare minimum requirement of the approving authority having to indicate what the thought process involved was is missing in the aforementioned approval order. While elaborate reasons need not be given, there has to be some indication that the approving authority has examined the draft orders and finds that it meets the requirement of the law. As explained in the above cases, the mere repeating of the words of the statute, or mere “rubber stamping” of the letter seeking sanction by using similar words like ‘see’ or ‘approved’ will not satisfy the requirement of the law. This is where the Technical Manual of Office Procedure becomes important. Although, it was in the context of Section 158BG of the Act, it would equally apply to Section 153D of the Act. There are three or four requirements that are mandated therein, (i) the AO should submit the draft assessment order “well in time”. Here it was submitted just two days prior to the deadline thereby putting the approving authority under great pressure and not giving him sufficient time to apply his ITA Nos.284-290/CTK/2025 mind; (ii) the final approval must be in writing; (iii) The fact that approval has been obtained, should be mentioned in the body of the assessment order.

23. In the present case, it is an admitted position that the assessment orders are totally silent about the AO having written to the Additional CIT seeking his approval or of the Additional CIT having granted such approval. Interestingly, the assessment orders were passed on 30th December 2010 without mentioning the above fact. These two orders were therefore not in compliance with the requirement spelt out in para 9 of the Manual of Official Procedure.

24. The above manual is meant as a guideline to the AOs. Since it was issued by the CBDT, the powers for issuing such guidelines can be traced to Section 119 of the Act. It has been held in a series of judgments that the instructions under Section 119 of the Act are certainly binding on the Department. In Commissioner of Customs v. Indian Oil Corporation Ltd. 2004 (165) E.L.T. 257 (S.C.) the Supreme Court observed as under:

“Despite the categorical language of the clarification by the Constitution Bench, the issue was again sought to be raised before a Bench of three Judges in Central Board of Central Excise, Vadodara v. Dhiren Chemicals Industries: 2002 (143) ELT 19 where the view of the Constitution Bench regarding the binding nature of circulars issued under Section 37B of the Central Excise Act, 1944 was reiterated after it was drawn to the attention of the Court by the Revenue that there were in fact circulars issued by the Central Board of Excise and Customs which gave a different interpretation to the phrase as interpreted by the Constitution Bench. The same view has also been taken in Simplex Castings Ltd. v. Commissioner of Customs, Vishakhapatnam 2003 (5) SCC 528. The principles laid down by all these decisions are: (1) Although a circular is not binding on a Court or an assessee, it is not open to the Revenue to raise the contention that is contrary to a binding circular by the Board. When a circular remains in operation, the Revenue is bound by it and cannot be allowed to plead that it is not valid nor that it is contrary to the terms of the statute.

2. Despite the decision of this Court, the Department cannot be permitted to take a stand contrary to the instructions issued by the Board.

3. A show cause notice and demand contrary to existing circulars of the Board are ab initio bad (4) It is not open to the Revenue to advance an argument or file an appeal contrary to the circulars.”

25. For all of the aforementioned reasons, the Court finds that the ITAT has correctly set out the legal position while holding that the requirement of prior approval of the superior officer before an order ITA Nos.284-290/CTK/2025 of assessment or reassessment is passed pursuant to a search operation is a mandatory requirement of Section 153D of the Act and that such approval is not meant to be given mechanically. The Court also concurs with the finding of the ITAT that in the present cases such approval was granted mechanically without application of mind by the Additional CIT resulting in vitiating the assessment orders themselves.

26. The question of law framed is therefore answered in the affirmative i.e., in favour of the Assessee and against the Department.

13. We note that in the said decision the Hon’ble Orissa High Court hasheld that the approval granted in mechanical manner by the competent authority without application of mind is not a valid approval. The said decision of the Hon’ble Orissa High Court has been affirmed by the Hon’ble Supreme Court on the SLP filed by the revenue, reported in 163 com 118 (SC). In view of the above, we do not find any merit in the contention of the ld. CIT-DR that the competent authority i.e. Addl./JCIT are usually involved in the assessment proceedings right from stage 1 till the end and, thus, they are aware of all the facts and proceedings. Therefore, the argument of the ld. CIT-DR that granting of approval by way of consolidated order was valid, is devoid of any merit as in all the aforesaid decisions, it has categorically been held by various Courts/judicial forums that the approval shall be granted separately for each year. Therefore, considering the facts of the present case before us, in the light of the ratio laid down in the above decisions, we are inclined to quash the approval granted u/s 153D of the Act and also the assessment framed by the AO on the ground of being framed on the basis on invalid and mechanical approval granted u/s.153D of the Act.

14. Thus, appeals of the assessee in ITA Nos. 233, 234 & 235/PAT/2024 for the assessment years 2014-2015, 2015-2016 & 20132014 in the case of Saroj Bala, are allowed.

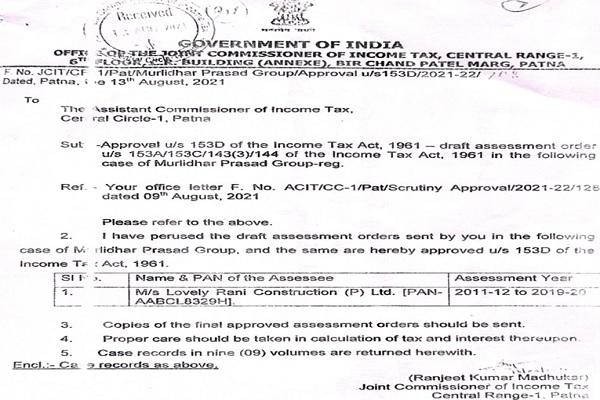

15. Now, we shall decide ITA Nos.279, 282 & 283/PAT/2023 filed by the assessee-Lovely Rani Constructions Pvt. Ltd. for the assessment years 2013-2014, 2016-2017 & 2018-2019.

16. The facts qua the above appeals are same as extracted above and decided by us in the case of Saroj Bala. The assessee has challenged the assessments framed by the AO on the ground of being passed consequent to invalid approval granted u/s.153D of the Act by the JCIT without application of mind as the same is granted for all the assessment years together by way of a consolidated order. For the sake of ready reference the order passed u/s.153D of the Act same is extracted hereinbelow:-

17. As we have already adjudicated the issue in ITA No.234/PAT/2024 for A.Y.2014-2015 in favour of the assessee by holding that the consolidated approval granted by the JCIT u/s 153D of the Act as well as consequential order is not sustainable in the eyes of law. Therefore, the findings recorded by us in the said appeal shall apply mutatis mutandis to these appeals as well. Thus, ITA Nos.279, 282 & 283/PAT/2023 filed by the assessee-Lovely Rani Constructions Pvt. Ltd. for the assessment years 2013-2014, 2016-2017 & 2018-2019 are allowed.

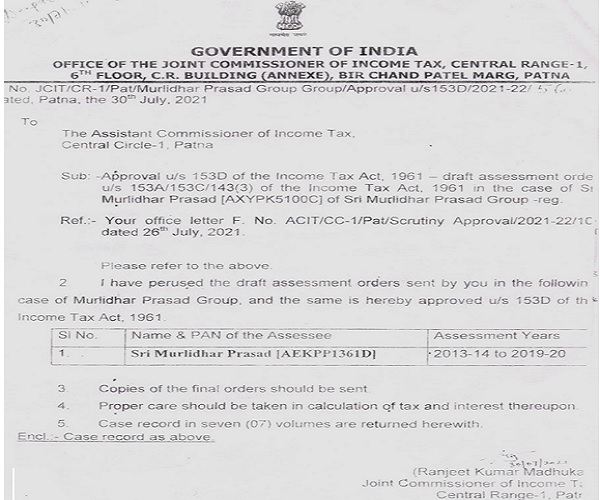

18. Now, we shall decide ITA Nos.272-276&278/PAT/2023 filed by the assessee-Murlidhar Prasad for the assessment years 2014-2015, 20152016, 2016-2017, 2017-2018, 2019-2020 & 2018-2019 and ITA Nos.291&293/PAT/2023 filed by the revenue for A.Y.2019-2020 & 20182019.

19. The facts qua the assessee are same as extracted above and decided by us in the case of Saroj Bala in ITA No.234/PAT/2024 for A.Y.2014-2015. In the present cases, the assessee has challenged the assessment framed by the AO on the ground of being passed consequent to the invalid approval granted u/s.153A of the Act by the JCIT without application of mind and the same is granted for all the years together by way of a consolidated order. For the sake of ready reference the order u/s.153D of the Act is extracted hereinbelow:-

20. As we have already adjudicated the issue in ITA No.234/PAT/2024 for A.Y.2014-2015 in favour of the assessee by holding that the consolidated approval granted by the JCIT as well as consequential assessment order is not sustainable in the eyes of law. Therefore, the findings recorded by us in the said appeal shall apply mutatis mutandis to these appeals as well.

21. With regard to appeals of the revenue in ITA Nos.291&293/PAT/2023 for A.Y.2019-2020 & 2018-2019, as we have already quashed the assessment for the assessment years under consideration holding that the consolidated approval granted by the JCIT is invalid, the appeals of the revenue for above assessment years under consideration have no legs to stand and accordingly we dismiss the same.

22. Thus, ITA Nos.272-276 & 278/PAT/2023 filed by the assessee-Murlidhar Prasad for the assessment years 2014-2015, 2015-2016, 20162017, 2017-2018, 2019-2020 & 2018-2019 are allowed and appeals of the revenue in ITA Nos.291&293/PAT/2023 for A.Ys.2019-20 & 2018-19 are dismissed.

23. Now, we shall decide ITA No.277/PAT/2023 filed by the assessee- Saroj Bala for the assessment year 2013-2014.

24. The only issue raised by the assessee is against confirmation of addition of Rs.7,15,600/- as made by the AO treating the agricultural income as unexplained income u/s.69A of the Act and bringing to tax @60% u/s.115BBE of the Act.

25. Facts in the present case have already been discussed hereinabove which are common. The assessee filed a voluntary return of income on 29.08.2019 declaring total income at Rs.2,96,330/-. Besides the assessee has declared the agricultural income also of Rs.7,15,600/-. The AO treated the said agricultural income to be not acceptable and treated the same as unexplained u/s.69A of the Act by invoking the provisions of Section 115BBE of the Act.

26. In the appellate proceedings the ld. CIT(A) also dismissed the appeal of the assessee by ignoring the submissions of the assessee that the assessee owned agricultural land of 14.32 acres at Kishanganj near Bihar and Bengal border for which the assessee submitted necessary documents of ownership of land during the assessment proceedings. It was also observed by the ld. CIT(A) that before the AO the assessee has submitted that the assessee was not doing the agricultural activities by herself. Therefore, she could not submit the necessary documents as required by the AO during the assessment proceedings. The ld. CIT(A) noted that the agricultural operations were being carried out by the agriculturists who were managing all the affairs like growing or selling the agricultural produce. However, the bills regarding diesel, water charges, pesticides etc. were produced before the ld. CIT(A) for which ld. CIT(A) observed that the agricultural activities were being carried out on the aforesaid land.

27. It was submitted by the ld. AR that the assessee was consistently showing the agricultural income from the assessment year 2011-2012 onwards in the return of income. It was submitted that AY 2012-13 was reopened u/s 147 of the Act on the grounds that the appellant was showing the agricultural income. It was submitted that the agricultural income shown by the appellant was duly accepted by the AO in the assessment framed u/s 147r.w.s. 143(3) of the Act . It was submitted that the AO made addition on account of agricultural income as unexplained income u/s.69A of the Act in the assessment years 2013-2014 & 20182019 and in the appellate proceedings, the ld. CIT(A) deleted the addition by accepting the submissions of the assessee except the instant assessment year under consideration.

28. After hearing the rival contentions and perusing the material available on record, we find that the assessee has been the owner of agricultural land of 14.32 acres in Kishanganj Bihar-Bengal Border and had been disclosing the agricultural income right from assessment year 2011-2012 onwards. The case of the assessee for A.Y.2012-2013 was reopened u/s.147 of the Act and in the assessment framed u/s.147 r.w.s.143(3) of the Act the agricultural income was accepted. However, the AO during the search assessment years 2013-2014 to 2018-2019 made the additions of agricultural income treating the same as unexplained income, which were deleted by the ld. CIT(A) for all the assessment years except A.Y.2019-2020. The relevant findings of the ld. CIT(A) for A.Y.2018-2019 are extracted hereinbelow :-

I have considered the assessment order and the submission of the appellant. The entries regarding transactions with Naved Alam were found written on the page no. 03 of the seized document MDP-06. Further, the appellant was given sufficient opportunities during the assessment proceedings to submit whether these entries have been recorded in the books of accounts maintained by him. However, it is found that the appellant has failed to avail of the opportunities provided to him. The appellant has submitted that he had nowhere admitted that the transactions in Naved’s account pertain to him. However, on perusal of the Q.27 of the statement which has been referred by the AO, the appellant has admitted that the account of Naved Alarm is maintained at Dena Bank and State bank and he used to receive the amount in the bank account of Md. Naved Alam. The undisputed facts on the issue are that deposit of commission on behalf of the appellant had been admitted by the appellant himself. Even signed blank cheques issued on the bank account held in the name of Md. Naved Alam was found and seized from the residential premises of the appellant. It confirmed the view that although the bank accounts existed in the name of Md. Naved Alam, however they were under control of the appellant Shri Murlidhar Prasad in which he has admitted to have received the commission amount from the contractors. The Ld. AR has disputed the addition, however, has failed to bring on record any documentary evidence to prove that said amount of Rs. 10,62,000/-genuinely represented the receipts of Md. Naved Alam. In view of the aforesaid discussion, I do not find any reason to disturb the addition. Accordingly, the ground is dismissed. Therefore, the addition of Rs. 10,62,000/- is hereby confirmed and the ground is dismissed.

29. Therefore, we do not find any find any merit in the order of the ld. CIT(A) as the same is in contradiction to the view taken in the earlier assessment years. Moreover, the addition was confirmed by the ld. CIT(A) without there being any substantial change of facts and circumstances and it would also be against the rule of consistency. In our view if there being no change of facts and circumstances of the case, the view taken by the department in the earlier assessment years has to be followed in the subsequent years as well. The case of the assessee finds supports from the decision of the Hon’ble Supreme Court in the case of Radhasoami Satsang, reported in [1992] 193 ITR 321 (SC) and the decision of the Hon’ble Supreme Court in the case of Excel Industries Ltd., reported in [2013] 358 ITR 298 (SC). Accordingly, we set aside the order of the ld.CIT(A) and direct the AO to delete the addition.

30. Thus, ITA No.277/PAT/2023for A.Y.2013-2014 is allowed.

31. Now, we shall decide the appeals filed by the assessee in ITA No.267/PAT/2024 and cross appeals filed by the revenue in ITA No.295/PAT/2023 along with cross objection of the assessee in CO NO.02/PAT/2023 in the case of Lovely Rani Construction Pvt. Ltd. for the assessment year 2012-2013.

32. First we shall decide appeal of the assessee in ITA No.267/PAT/2024 wherein the only issue raised by the assessee is against the confirmation of addition of Rs.39,10,270/- by the ld. CIT(A) by partly allowing the appeal of the assessee as against the addition of Rs.1,24,50,000/- made by the AO.

33. Facts in brief are that during the course of assessment proceedings the assessee was asked by the AO to explain the receipt of Rs.1,24,50,000/- received from Smt. Anusuya Singh and cash expenses of Rs.85,39,730/- as per the seized document being MDP07 during search. The assessee submitted before the AO that since he had not seen the seized documents he was not in a position to explain the same. The said documents were never confronted to the Assessee, however, the assessee on the other hand submitted that all the receipts from Smt. Anusuya Singh had been recorded in the books of accounts in A.Y.2012-2013 & 2013-2014. The assessee also submitted that there was no evidence other than the sale deed which showed that the assessee had received any money over and above the sale consideration. It was only while making the addition, the AO referred to the documents seized by the Investigation wing without confronting the same to the assessee. However, the contention of the assessee did not find favour with the AO and he made addition to the income of the assessee of Rs.1,24,50,000/-.

34. Ld. CIT(A) partly allowed the appeal after taking into consideration the reply and arguments presented by the assessee as under :-

I have considered the findings of the AO recorded in the assessment order and the submission of the appellant. From the perusal of the assessment order, it transpires that the AO granted sufficient opportunities to the appellant to furnish evidence that the cash receipt of Rs. 1,24,50,000/- received from Smt. Anusuya Singh were duly recorded in the books of account of M/s Lovely Rani Construction Pvt Ltd. The AO has mentioned that the appellant could not produce necessary evidence to prove that the above amount was duly received in its books of account. Accordingly, the AO was constrained to treat the cash receipt of Rs. 1,24,50,000/- as the unrecorded receipt of income on revenue account in hands of the appellant company. Even during the course of appellate proceedings, the Ld. AR though has made written submission, however, has miserably failed to produce documentary evidence to prove that the impugned amount of Rs. 1,24,50,000/-was duly recorded in the books of account of the appellant M/s Lovely Rani Construction Pvt. Ltd. Hence, this amount is considered to be undisclosed business income of the appellant. As per Impounded material MDP-07, the appellant has Incurred expenses of Rs. 85,39,730/- which has also been mentioned by the AO in the assessment order. Most of these expenses relate to construction activities carried out by the appellant and have been found to have been Incurred after the cash received from SmtAnusuya Singh. Hence, benefit of telescoping is given to the appellant. Accordingly, the addition of Rs. 1,24,50,000/- is restricted to Rs. 39.10.270/- and the ground is partly allowed.0

35. After hearing the rival contentions of the parties and perusing the material available on record , we find that in the instant case the assessee had sold flat to Smt. Anusuya Singh for which the sale deed was executed and the payments received from Smt. Anusuya Singh were duly shown and recorded in the books of accounts maintained for A.Y.2012-2013 & 2013-2014 and offered the same to tax accordingly. The AO referred to the seized document being MDP-07 which was not found and discovered from the possession of the assessee but from Shri Murlidhar Prasad, and, therefore, it was never confronted to the assessee during the assessment proceedings. We note that the AO has only asked the assessee to explain the cash, however, the assessee denied that no such cash was ever received and admittedly proof of receipt of cash was not impounded from the assessee but from Shri Murlidhar Prasad. We have examined the seized documents MDP -07, which were seized from Shri Murlidhar Prasad and found that there is no mention of Smt. Anusuya Singh in the said documents. The copy of the said document is available in the paper book from page no. 1 to 22. We find that there are number of transactions mentioned in the said documents ranging from 2000 to 50,000, however, it is not clear as to what entries represented the said receipt of Rs.1,24,50,000/-, which were stated to be received from Smt. Anusuya Singh, in respect of sale of Flat. Therefore, we find merit in the argument of the ld. Counsel of the assessee that addition made on the said document cannot be sustained. The said documents only contained some description of transactions without any signatures and narrations as to whom, these transactions pertained to. Therefore, the ld. CIT(A) has erred in considering Rs.1,24,50,000/- as receipt from Anusuya Singh nonetheless the ld CIT(A) allowed expenses to the tune of Rs.85,39,730/-on the basis of MDP-07. In our opinion, the said document was never confronted to assessee and any addition made on the basis of such document cannot be sustained. At the most, the said document is a dump document and cannot attach any importance/significance/reliance for making addition. We have examined the seized documents MDP-07 seized from Shri Muralidhar Prasad and found that there is no mention of Smt. Anusuya Singh from whom Rs.1.24 crores was stated to be received. We find merit in the argument of the ld. counsel that in the said documents no mention of receipts of Rs.1.24 crores which according to the AO is the amount received from Anusuya Singh. The case of the assessee find support from the decision of Sunil Kumar Sharma Vs. DCIT (2023) 146 taxmann.com 553 (Karnataka) and SK Gupta Vs. DCIT 63 TTJ 532 (Delhi). Consequently, we reverse the order of the ld. CIT(A) on this issue and direct the AO to delete the addition.

36. Since, we have already directed the AO to delete the addition by allowing the appeal of the assessee in ITA No.267/PAT/2024, therefore, appeal of the revenue in ITA No.295/PAT/2023 against the confirmation of part addition by the ld. CIT(A) is dismissed. The cross objection of the assessee is also dismissed.

37. Thus, ITA No.267/PAT/2024 is allowed and ITA No.295/PAT/2023 & CO NO.02/PAT/2023 are dismissed.

38. In the result, ITA Nos.233-235/PAT/2024, ITA Nos.279, 282, 283, 272-276, 278, 277/PAT/2023& 267/PAT/2024 are allowed. Revenue’s appeal in ITA No.291, 293 & 295/PAT/2023 along with Cross Objection of the assessee in CO No.02/Pat/2023 are dismissed.

Order pronounced in the open court on 14/10/2025.