SynopsisWhile Covid brought unprecedented challenges, it helped the insurance sector to learn new things. Technology has made the distribution of the product faster and cheaper, which is critical to increase the bottom line of a company. The industry is likely to grow faster now as the economy is recovering from the pandemic impact.

The chances of benefiting from equity investment grow if you invest in a business you are familiar with or understand. Many of us would have at some point of time come across insurance in several forms, be it a term plan, an endowment plan, ULIP, health insurance, motor insurance and so on. Insurance is also one of the major pillars of financial services as it has become an inseparable part of personal finance. So, is the insurance business worthy of long-term equity investment? If yes, which companies are best suited for your investment?.

According to the Swiss Re Institute, the Indian life insurance industry will show resilience and grow at an exceptional rate of 6.6% (in real terms) in 2022 and 7.1% in 2023. Considering the projected growth rate, the life insurance premiums in India are set to cross $100 billion for the first time in 2022. The growth of global life insurance premiums will be almost flat this year and grow by 1.9% in real terms in 2023. According to the report, India’s insurance premiums are expected to keep growing at an average of 14% in the next 10 years. That will make India the sixth-largest insurance market in the world over the next decade. Let us understand the factors that are likely to drive this growth.

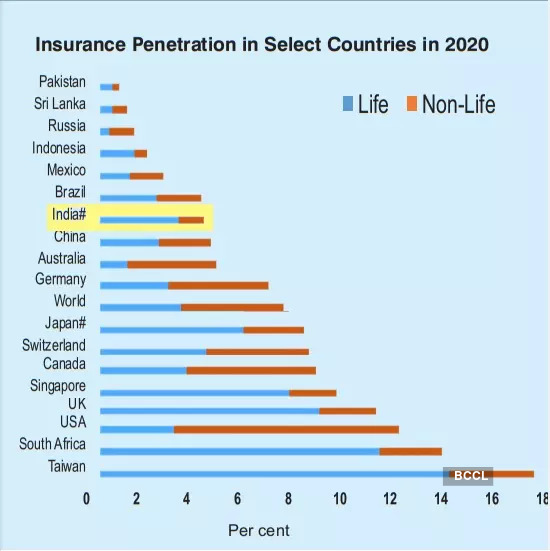

Underpenetrated sector

While India’s GDP may have done well to reach the fifth spot globally, when it comes to insurance penetration, the country has a long way to go. “India’s insurance sector has been steadily expanding in the past decade but its share in the global insurance market remains abysmally low. According to the Economic Survey of 2020-21, insurance penetration in India stood at 4.2 per cent as of 2020. This offers a huge growth opportunity for insurance companies,” says Arpit Jain, Joint MD at

.

Source: IRDA Annual Report 2020-21

Insurance to grow faster than the economy

Insurers have their task cut out. They might have to push the envelope to increase insurance penetration (percentage of insurance premiums to GDP) and insurance density (per capita premium). “Insurance companies are investing a large portion of their profits in marketing and to raise awareness about their products,” says Vivek Bajaj, Cofounder StockEdge & Elearnmarkets.com. “They see the low penetration of life insurance policies as a potential opportunity. As these companies sell simple insurance policies to more people in India, market leaders have a good chance of increasing their profits and market share.”

Apart from the growth potential, industry stakeholders see another reason to be optimistic. The industry is likely to grow faster now as the economy is recovering from the pandemic impact, supported by a conducive environment and the regulators, says Sandeep Bhardwaj, CEO-Retail,

. Even a “regular” growth in GDP will augur well for the insurance sector. Besides this, Bhardwaj says, the youth of the country have started believing that insurance is an important risk management tool.

As the average income of people rises, their awareness and inclination to buy insurance products would also rise. “Long-term growth drivers for the sector include a large protection gap and rising per capita income,” says Bajaj. “Strong players with the right mix of products, services and distribution will benefit disproportionately well from the opportunity.”

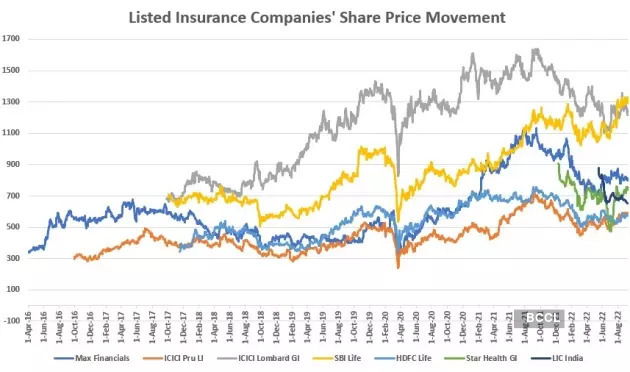

Source: BSE, Till August 9, 2022

Not only life, general insurers can create wealth for investors

Besides life insurance, the demand for general insurance policies is also expected to grow. Bhardwaj says general insurance companies will be key beneficiaries as the economy opens up, especially due to improved trade activity and increasing demand for motor and health insurance. “A strong growth in the automotive industry over the next decade is expected to give a boost to the motor insurance market,” says the CEO of IIFL Securities.

In the general insurance segment, health has shown higher growth potential. “The pandemic emphasised the importance of healthcare in the economy, and health insurance would play a critical role in the effort to strengthen the healthcare ecosystem,” says Bhardwaj.

7 driving forces that will fuel growth in insurance

- A rising middle class will buy more insurance: The rise in GDP is likely to propel many new Indians into the middle class. Bhardwaj says an additional 140 million middle-income and 21 million high-income households will drive the economy. “This is favourable demographics, as 55% of the Indian population is in the working-age bracket and expected to get covered (by insurance) under a lot of corporate, social or individual capacities.”

- Increased digitisation: The rising digitisation in India is giving new growth avenues to the insurance sector. “After the launch of Jio, there is widespread digitalisation. The pandemic helped to enhance the acceptance of digital payments, giving a boost to the growth of digi-insurance,” says Bhardwaj. While Covid brought unprecedented challenges, it helped the sector to learn new things. Technology has made the distribution of the product faster and cheaper, which is critical to increase the bottom line of a company. “Digital issuance and online channels are expected to witness continued growth. The share of web aggregators within digital insurance has been constantly increasing,” he says.

- Increased price power and improved profitability factors: The pricing power of the sector is getting stronger. Arpit Jain, Joint MD atArihant CapitalMarkets, says: “The industry hiked premiums after Covid and this trend would aid long-term profitability. Claim settlement ratio is going to improve in the favour of insurance companies as the impact of Covid is reducing. Overall, life expectancy has improved, and this should augur well for insurance companies.”

- Push to simplify the processes: Many operational hurdles in digital buying and claim process were removed by the Insurance Regulatory and Development Authority (IRDAI). “The regulator has undertaken various initiatives to boost insurance penetration, such as permitting insurers to conduct video-based KYC, launching standardised insurance products, and allowing insurers to offer rewards for low-risk behaviour,” says Bhardwaj. The regulator has been continuously cracking down on misselling and also trying to enhance the quality of the grievance redressal method.

- Greater flexibility to bring innovation: IRDA has also shown greater flexibility in allowing companies to innovate. “Recently, IRDAI streamlined the process to launch products by implementing revisions in the ‘file & use’ policy. This will encourage insurers to launch products that are more aligned with clients’ needs,” says Bhardwaj.

- Technology to enhance the volume of simpler products:Introducing products that are easy to understand will make insurance more attractive to prospective customers. “The focus of the insurance sector is steadily shifting towards increasing access to low-cost and simple products. This, coupled with the use of digital technologies like IoT and blockchain, will propel the insurance industry,” says Jain.

- Great appeal as long-term wealth creators: Given the growth potential, insurance is worth consideration for your long-term equity investment. The low penetration levels give these companies a long growth trajectory, says Tanushree Banerjee, Co-Head of Research at Equitymaster. “Investors must consider investing in insurance companies for the long term based on the distinct moats of product profile and distribution strength,” she adds.

The best bets in insurance

Out of the prominent life insurance companies,

has demonstrated the most remarkable performance. It has captured the highest market share among private life insurers in new business premium, which is second to LIC on an overall basis.

“Our top pick,

Life, seems to be best placed from a growth-recovery and valuation-headroom perspective,” says Bhardwaj. “SBI Life (SBILI) reported 1QFY23 results with 79% YoY growth in APE, while renewal premium grew at a healthy 14% YoY, on a steady base. SBILI witnessed healthy traction in its non-par (including annuities), retail protection, and group savings segments (+372%/54%/ 122% YoY), while ULIPs saw 33% YoY growth. Group protection APE remained healthy, growing 33% YoY,” says Bhardwaj.

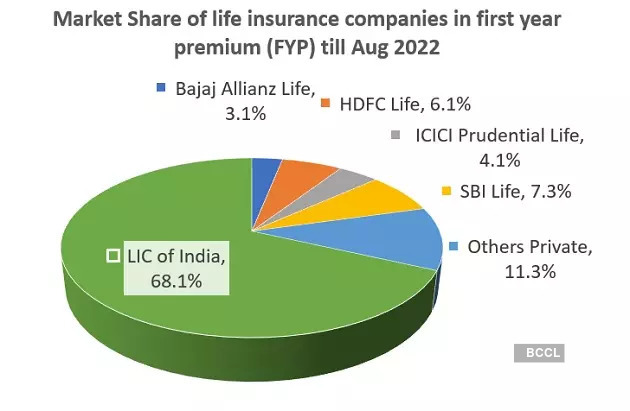

Source: IRDA

SBI has been working well on several profitability matrices. “VNB (value of new business) margin saw a 630-basis point expansion YoY to 30.4% (on effective tax rate basis), on improved business mix towards non-par and protection. Management hopes to deliver 25%+ premium growth in the rest of the year on the back of strong demand for its recently launched guaranteed product and retail protection,” says Bhardwaj.

Source: IRDA

has also maintained its high growth momentum and has all the factors that make it an attractive buy for retail investors. Bajaj, the cofounder StockEdge, says: “With a healthy capitalisation and a favourable business mix, HDFC Life is better positioned in the current environment because of its high proportion of protection, savings-related products and strong business franchise. Being the largest player, it is likely to benefit from favourable tailwinds. The company’s sustained persistency ratio reflects client service and product quality, both of which are critical for long-term sustainability.”

For Max Life, the journey has been a slow-and-steady rise — favoured by many investors. Emkay Research has maintained a buy call on this company. In its August report, Share Khan Research gave a buy call on Max Life at Rs 848 and a target price of Rs 1,020. Motilal Oswal has also given a buy call with a target price of Rs 950. “Among the listed insurance companies, HDFC Life, SBI Life and Max Life are good to invest in at current levels,” says Jain.

Life witnessed a higher volatility in its premium growth in recent past, but it seems to have gotten its act together of late. Emkay Research has maintained a buy call on this company with a target price of Rs 670. Share Khan gave a buy call with a target price of Rs 650 in its July report.

Among the general insurance players Star Health Insurance and

GI, the former seems to have an edge in the current situation. “ICICI Lombard is doing well but the overhang of an FPO would limit its upside in the near term,” says Jain. Motilal Oswal Research says it expects the health insurance segment to continue to outpace the growth of the general insurance segment. Star, “with a 16%/33% market share in the health/retail health industry” is well-positioned to benefit from this growth story. Given the strong earnings growth prospects and healthy RoE profile (15-17%), the brokerage house has maintained its buy rating with a target price of Rs 800.

Should you buy LIC now?

While the insurance behemoth, LIC, was listed with much fanfare, it proved to be a disappointment later for many retail investors. However, a sharp correction has made this stock attractive to some. But not all are very confident about investing in LIC at the current level.

“The LIC stock has corrected over 32% from its IPO price in less than four months,” says Jain. “The company’s premium growth has been strong, and it seems to check all the right boxes to maintain its industry-leading position with a market share of over 60%, and ramp up growth in the highly profitable product segments. The stock price looks attractive at current levels and investors can consider adding LIC in their portfolio with a long-term investment horizon.”

It is an insurance giant in India and there is hardly any comparable benchmark to get its valuation right. So, it is likely to create its own value proposition with time, which investors can relate to and compare. “LIC is India’s largest insurance company, with ~37%/74% market share in FY22 in retail APE (annual premium equivalent)/group NBP (new business premium), respectively,” says Bhardwaj. “It boasts of being one of the strongest brands in the country and having an unparalleled agency network that ensures it still owns ~46% of the total APE market even after 20 years of privatisation of the sector. LIC’s current portfolio, while significantly large, offers multiple pockets of opportunities for faster growth.”

There has been improvement in transparency and a push towards rewarding equity investors. “Before the IPO, the majority of LIC’s operations were centred on participating policies that ensured consistent cash flows. Before the listing, amendments to the LIC Act resulted in the separation of participating and non-participating funds as well as a revised surplus distribution policy in favour of the shareholder (95:5 to 90:10 by FY25). LIC is also working to diversify its product mix to the margin-enhancing non-par segment,” says Bajaj.

While no one can rule out a further downside from this level, the chances of a very significant correction are less. “With the price correction in LIC, the PE multiple for the stock has come down to 102X of FY22 earnings, though it is still higher than its peers, which trade in the range of 80-90x of FY22 earnings. However, if we look at LIC’s price to sales ratio and the price to embedded value, the former has come down to 0.58X of FY22 revenue, while the latter is at 0.76X, both of which are significantly lower than those of the private players. As the stock is currently trading near lows, one can start investing in it in a staggered manner. A stock SIP would be better suited,” says Bhardwaj.

While Emkay Research has given a hold call on LIC, Motilal Oswal Research has given a buy call at Rs 682 and a target price of Rs 830.

Limited investment options in insurance?

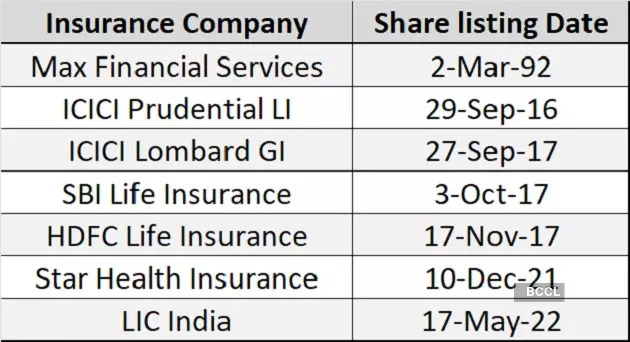

There are several insurance companies in India but only seven are listed. So that narrows the equity investment avenues. Only one insurance company was listed on Indian exchanges until 2016 but the scenario changed after that. “India has 57 insurance companies — 24 life insurance companies and 34 general insurance companies. But only seven are listed. The sector opened up for individual investors after

ICICI Prudential Life Insurance Company

made a successful debut on the bourses in 2016,” says Jain of Arihant Capital Markets.

Source: BSE

Should you wait for more listings or invest now?

With only seven listed players in the insurance industry, many investors say they would like to wait for more players to get listed before jumping in. This is because many prominent companies Bajaj Allianz, Aditya Birla Sun Life, Tata AIG and Kotak, among others are still unlisted. So, should you wait for these companies to list or invest now?

Bhardwaj says most big players have been listed and there is no definite timeline for others to be listed. “Consider investing in existing players so as not to miss the opportunity now.”

The industry is growing and there are enough opportunities to invest in the listed insurance space, says Jain of Arihant Capital. “I believe it is imperative for investors to be part of the Indian insurance industry as they have the potential to become consistent wealth creators,” says Jain. (Originally published on Sep 13, 2022, 09:58 AM IST)

Share the joy of reading! Gift this story to your friends & peers with a personalized message. Gift Now