It’s too early to say if the central bank’s recent measures will offer relief any time soon

Photo: iStock.

The Financial Stability Report (FSR, June 2022), released last month, had observed: “Across emerging and developing economies, debt distress is rising as external funding conditions turn austere, compounded by currency depreciation and drainage of reserves as investors shun them as an asset class and fly to the safe haven of the relentlessly strengthening the dollar”.

This sentence in the Reserve Bank of India’s (RBI’s) bi-annual publication hasn’t got the attention it deserved. And the surprise over the decisions on the forex front on July 6-7 is proof enough.

But will these measures deliver the desired results? (The rupee closed at 79.88 to the dollar on Friday.)

“The rupee may not have depreciated to the extent a few other currencies have against the dollar, but all we know is that the RBI sold tens of billions of dollars to stem the rupee’s slide,” says Madan Sabnavis, chief economist at Bank of Baroda. “We will never know how many dollars other central banks sold to defend their currencies, or if at all they did.”

It has also triggered discussions (in private quarters) around the dollar’s appreciation despite the surge in US inflation. But the straightforward point here, a senior banker says, “is that the hike in interest rates and the fact that the dollar is a reserve currency has made the greenback all the more attractive!”

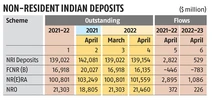

It follows that non-resident deposits may not inch up merely because the RBI has allowed banks to offer higher interest rates, because banks themselves may not be keen to raise them. Reason: Unlike in the past, the RBI has not opened a swap-window for banks, and the hedging costs involved don’t actually make this an attractive option for banks either.

The same logic applies to the move to ease the sourcing of cross-border loans, which is linked to India Inc’s capacity expansion plans and the ability of firms to service them out of their earnings — firms without a natural dollar hedge may not be keen to take on currency risks at this point.

Incidentally, an RBI working paper (India’s External Commercial Borrowings: Determinants and Optimal Hedge Ratio) in January estimated the optimal hedge ratio for such borrowings at 63 per cent for periods of volatility in the forex market.

The nitty-gritty

Take the move on the settlement of trades in rupees. C S Setty, managing director (international banking) at the State Bank of India, reckons the arrangement will “ease the settlement of trade transactions with countries where bilateral trade flows (exports and imports) are substantial.”

He says “the bank is in the process of framing standard operating procedures before making customers aware of the facility for opening of special vostro accounts.” (A vostro account is an essential aspect of correspondent banking in which a bank holding the funds acts as custodian for or manages the account of a foreign counterpart.)

Taken together, external commercial borrowings (ECBs) and deposits of non-resident Indians constituted nearly 60 per cent of India’s external debt, followed by short-term trade credit (18 per cent). Net ECBs amounted to $12.8 billion during FY22. Nearly 80 per cent of ECBs are denominated in dollars and five per cent each in euro and yen. A predominant component (56 per cent) of these loans are hedged. And private-sector borrowers have a larger share of hedged loans.

Again, it’s not the settlement of trades in rupees that is necessarily to be read as a step towards “internationalisation” of the domestic currency, even though the idea had been referred to by the former RBI governor, Raghuram Rajan, in September 2013: “This might be a strange time to talk about rupee internationalisation, but we have to think beyond the next few months. As our trade expands, we will push for more settlement in rupees…”

Points out Ananth Narayan, senior India analyst at the Observatory Group: “It allows for a more generalised internationalisation of the rupee, but realistically, the immediate takers right now are likely countries that wish to move out of dollar-G7 currency settlements for fear of sanctions.” He says the RBI circular’s language also seems to envisage and allow for alternative financial messaging to SWIFT, if needed.

He notes that the trade balance — in Russia’s favour — will stay, as rupee balances of Russian banks with India’s banking system are to be invested in Indian assets (including government securities).

But will this last aspect really come through? At a time when foreign portfolio investors have sold heavily their investments in debt, to think Russian entities will invest their surplus held under the just announced trade settlement framework in Indian government securities is to take an immense leap of faith.

Missed trick

The RBI could have also taken the demand for dollars by oil firms off market by doing bilateral deals with them, thereby easing the pressure on the spot-rupee. But in hindsight, the move not to float dollar-bonds over a ten-year period as mooted in the 2019 budget appears to have been a misstep, as the government opted to allow foreign investors to buy local debt (at higher rates) — and there have been no takers.

Explains S C Garg, former finance secretary, Government of India: “The idea was to borrow $10 billion every year for ten years. Or, in all, $100 billion. Thereafter, annual borrowing would have gone towards refinancing retiring debt.” He thinks it was not activated because “there was an uproar, largely on the misconceived ground that this could lead to profligacy, as the government would not be able to control its urge to borrow.” But this was unfounded, he says.

He believes borrowing abroad would have been better fiscally, and in exchange rate management — it would have been cheap and there would have been no pressure on the rupee, as foreigners would buy and sell the bonds among themselves instead of repatriating proceeds from India.

“There’s also another aspect. To the extent that foreigners sell rupee-denominated debt, it puts pressure on the yields, which, in turn, affects domestic government debt issuance as well,” he notes.

The country may not be in for a roller-coaster ride, but it will be a ride nevertheless.