Clipped from: https://economictimes.indiatimes.com/industry/banking/finance/banking/rbi-exploring-need-for-crypto-currency-as-digital-payments-rise/articleshow/80452408.cmsSynopsis

“Private digital currencies (PDCs) / virtual currencies (VCs) / crypto currencies (CCs) have gained popularity in recent years. In India, the regulators and governments have been sceptical about these currencies and are apprehensive about the associated risks. Nevertheless, RBI is exploring the possibility as to whether there is a need for a digital version of fiat currency and in case there is, then how to operationalise it,” the central bank said.

MUMBAI: The Reserve Bank of India (RBI) is exploring whether there is a need for a digital version of fiat or crypto currency and in case there is, then how to operationalise it, the central bank said in a booklet covering the journey of payment and settlement systems in India during t2010 till the end of 2020.

“Private digital currencies (PDCs) / virtual currencies (VCs) / crypto currencies (CCs) have gained popularity in recent years. In India, the regulators and governments have been sceptical about these currencies and are apprehensive about the associated risks. Nevertheless, RBI is exploring the possibility as to whether there is a need for a digital version of fiat currency and in case there is, then how to operationalise it,” the central bank said.

RBI will also publish a digital payments index (DPI) to effectively capture the extent of digitisation of payments in the country and accurately portray the penetration and deepening of various digital payment modes.

“The RBI-DPI has since been constructed with March 2018 as the base period, i.e. DPI score for March 2018 is set at 100. RBI-DPI was published on January 01, 2021 and the DPI score for March 2019 and March 2020 were 153.47 and 207.84, respectively,” RBI said.

Digital payment transactions in India have risen to 3435 crore processing Rs 1623 lakh crore by value in March 2020 from just 96 crore transaction processing Rs 498 crore by value in March 2011 representing a compounded annual growth rate of 12.54% and 43.01% in terms of volume and value, respectively, the RBI said.

Global Data, a data and analytics company, in its 2017 consumer payments insight survey, observed that India is one of the top markets globally in terms of digital cash adoption with 55.4% survey respondents indicating usage of digital cash. India is followed by China and Denmark. “The adoption level in India is much higher compared to many of the developed markets such as the US and the UK, where consumers predominantly use cards,” RBI said.

The central bank plans to engage with the other sectoral regulators – SEBI, IRDA, TRAI, etc., to remove frictions in regulation and ease system operator / customer comfort and has set-up an inter-regulatory committee on digital payments with officials from other financial sector regulators.

“The committee is expected to work towards overcoming frictions in digital payments arising out of connectivity issues, exchange inputs / references between / amongst regulators, enhance awareness about digital payments, facilitate digital financial inclusion, etc,” RBI said.

Read More News on

traiIRDAdigital paymentsRBIcryto currencysebi(Catch all the Business News, Breaking News Events and Latest News Updates on The Economic Times.)

Download The Economic Times News App to get Daily Market Updates & Live Business News.

2 Comments on this Story

| Vignesh Iyer1 hour agoRiches and government fears the crypto because they cannot hold or impose regulations on digital currencies. Predominantly all the transactions performed are transparent over the network though impossible to tamper due to consensus algorithm, thanks to block chain. | |

| ramanath4 hours agoFirst you block and now you approve. What is this nonsense organisation |

Advertorial

Tech Tonic SMBs’ Magic Potion for Growth

Synopsis

For most SMBs, credit score is non-existent. Their public profiles and balance sheets are not something the banks can trust to give loans.

The pandemic has forced everyone to go digital, including both businesses and their customers. Small and medium businesses, which traditionally shied away from tech investments, can look the other way only at their peril

Former IAS officer at ‘anecdote age’: “To start a business in India today, for an average MSME, technically there are 58,172 compliances. The updates, amendments, changes on these compliances are 3,516 per annum.”

Sceptical journo: [Aghast] “How can India possibly solve this issue? It sounds horribly large and unsolvable.”

Former IAS officer at ‘anecdote age’: “We have done it before. In the 1990s, India decided to go digital by dematerialising shares. An American agency wrote a report in 1995, and laughed, and said you guys want to do something that nobody in the world has done. Don’t even try this. So, what did India do? India wrote the Depositories Legislation, one of our finest pieces of legislation, in three nights, by hand. That legislation needed a constitutional amendment and with ratification from states within a month, India created the NSDL, and today millions of shares can be transferred in a second.”

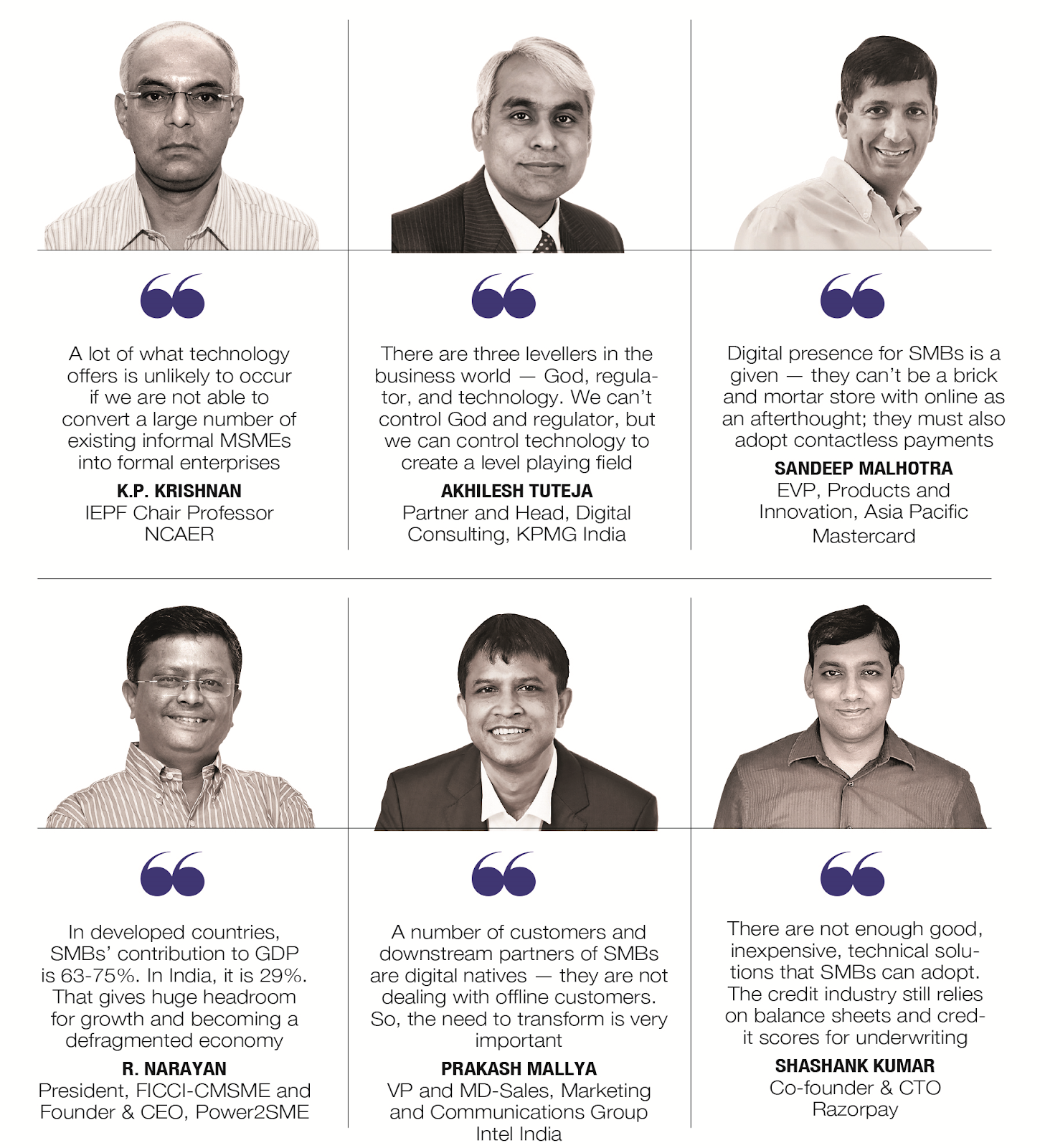

The larger point being made by K.P. Krishnan, currently IEPF Chair Professor at NCAER, and former secretary in the ministry of skill development and entrepreneurship, was that “tech comes in majorly by government creating platforms for these [58,172] compliances, because a lot of these are information that you need to file, which can be easily handled by technology”. Krishnan, incidentally, heads a task force to clean up these compliances, and is working with some state governments to implement the recommendations.

Krishnan was participating in a brainstorming session organised by The Economic Times and Mastercard, on the subject “Technology in Small Business – The Path to Sustained Growth”, along with some other stalwarts. The discussion was moderated by Alokesh Bhattacharyya, Senior Editor and Suchetana Ray, Senior Assistant Editor of The Economic Times.

The fundamental problem, as Intel’s Prakash Mallya pointed out, is that “there is a fear of technology adoption, which we need to circumvent. The second is [their perception] of no justification or RoI for tech adoption”. Ironically, the pandemic has practically forced everyone to adopt digital solutions. “In the past 10 months, people who serve you at your homestay have all adopted whatever digital tools they need to survive,” pointed out R. Narayan of FICCI & Power2SME.

Sandeep Malhotra of Mastercard highlighted three big, lasting trends that are moving SMBs towards technology: (1) People are staying home and ordering online (2) India is going cashless; ATM withdrawals are at all-time low (3) Contactless, tap and go, payments are rising. “Last year, 30 per cent of all transactions worldwide were tap and go; it has become 41 per cent in 10 months,” said Malhotra. “India used to be 3 per cent tap and go; it’s now mid-teens.”

Certain things need change. Razorpay’s Shashank Kumar pointed out that the credit industry still relies on balance sheets and credit scores for underwriting SMB loans: “For most SMBs, credit score is non-existent. Their public profiles and balance sheets are not something the banks can trust to give loans.” Instead, companies like Razorpay and Mastercard have found ways to use data to determine credit-worthiness of small entities, and then provide them collateral-free loans.

All panellists agreed on the acceleration of tech adoption during the pandemic, but then the question is: what’s the right way for a small, low-on-capital entity to adopt technology? First, as Mallya pointed out, technology is not expensive any more, and “all technologies are operating on pay per use model”. Kumar said SMBs must first digitalise the front-end of their business, through simple tools such as a website, Google Maps, WhatsApp, Khatabook or OkCredit. Then, make it convenient for customers to pay digitally.

At the back end, SMBs should first look at where their time is most spent — payroll or compliances or taxation — and use digital tools to cut down on the time, and also bring efficiency and cost optimisation. Malhotra of Mastercard added that once the front and back-ends are digitalised, SMBs should move to richer things like employee collaboration, electronic education, financial literacy, digital identity, etc.

Government policy also plays a part. “Germany’s MSMEs have a significant contribution to the national GDP,” said KPMG’s Akhilesh Tuteja. “Such markets provide impetus for easy access to technology. And if you use technology, availability of capital and credit happens at a much lower cost.” Greater digitalisation of the lending ecosystem would surely lower cost of capital and ease access to credit. “We need to think about SMBs who are under the GST barrier,” said Narayan. “Progressive SMBs can dig out what is good for them.”

The rest, we must address.