Clipped from: https://economictimes.indiatimes.com

Will Ayushman Bharat become a model for universal health care?

The scheme, which covers hospitalisation costs for 50 cr beneficiaries, is closely identified with PM Modi.

On May 18, 35-year-old homemaker Puja Thapa, a resident of Meghalaya’s Ri Bhoi district, underwent a minimally invasive surgery to remove kidney stones at Shillong’s Nazareth Hospital. Thapa, as her family found out after the diagnosis, was a beneficiary under the Ayushman Bharat health insurance scheme. This meant the cost of the surgery and treatment at the private hospital, which came to Rs 36,300, was borne by the scheme.

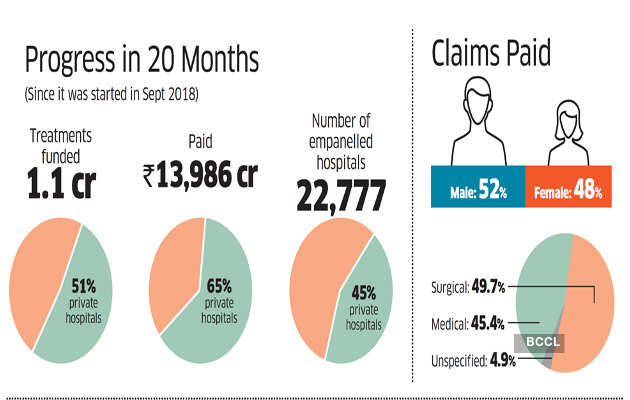

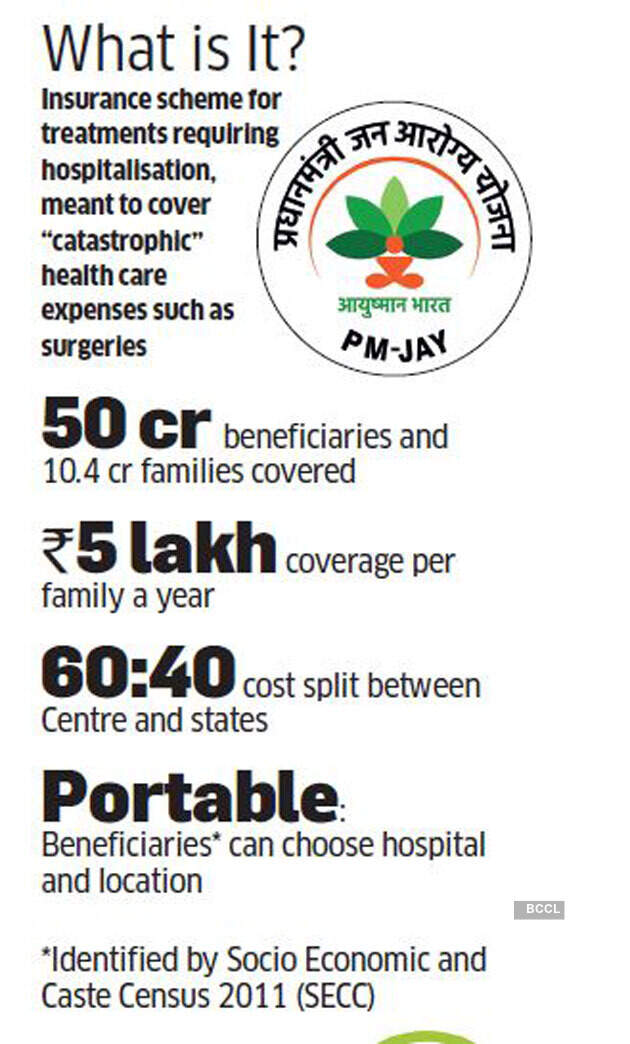

The routine surgery marked a milestone for the ambitious and politically significant Ayushman Bharat — the Pradhan Mantri Jan Arogya Yojana (PMJAY) — it completed the delivery of one crore treatments since its launch in September 2018. The scheme, which covers hospitalisation expenses for 50 crore beneficiaries, or 40% of India’s most vulnerable, is closely identified with PM Narendra Modi, and is a key piece in the arsenal of welfare schemes that is seen to have played a role in his return to power in 2019.

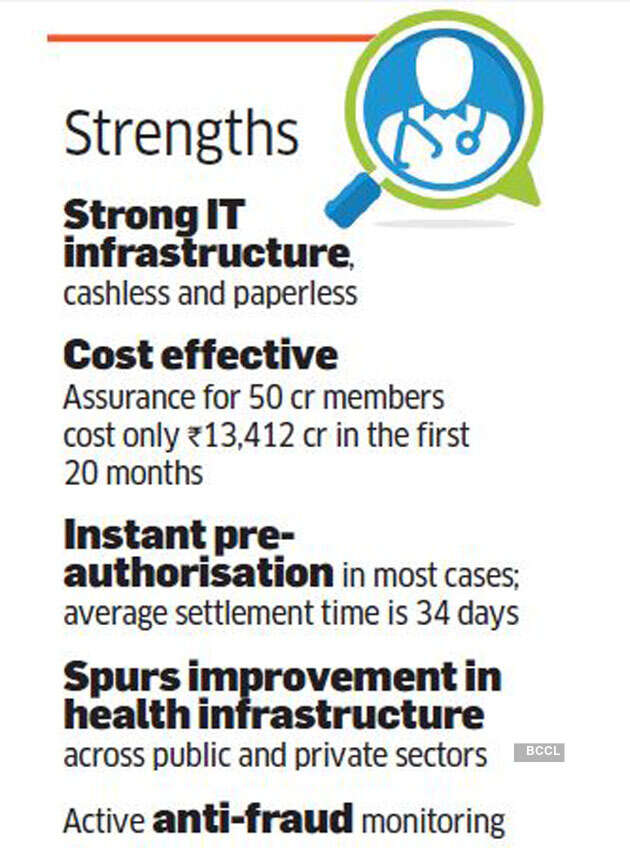

Now billed as the largest publicly funded health care programme in the world, PMJAY has emerged through teething troubles to deliver cashless treatments in 22,700 empanelled hospitals, all connected through an IT backbone designed to eliminate paperwork, enforce standards and prevent abuse.

Conversations with various stakeholders — patients, doctors, public and private hospitals, state governments as well as administrators — reveal a scheme that’s necessary, professionally run and improving, but also one that has yet to adequately contend with weaknesses in design, database, pricing and distortion, among others. The difficult task of achieving equilibrium at the confluence of competing interests, it would appear, is a work in progress.

PMJAY’s progress has a larger import. India is committed to providing universal health care by 2030 as part of the UN sustainable development goals. Before the current government’s term ends, the country would likely have to take a call on the model or group of models that will be deployed to achieve this. PMJAY will doubtless be a contender.

How It Works

PMJAY is essentially a demand-side intervention in public health, a strategy pioneered by Rashtriya Swasthya Bima Yojana (RSBY), a predecessor scheme introduced in 2008 by the first Manmohan Singh government, with a cover of Rs 30,000 per family per year (PMJAY cover is Rs 5 lakh). This marked a departure from what India had done all along — supply-side provisioning in the form of operating public hospitals and health centres. “India always relied on supply-side management, meaning you pump money into government hospitals and rely on that infrastructure to provide care. That was clearly not working. That’s why we thought why not experiment with demand-side management,” says Anil Swarup, the former bureaucrat who designed and ran that scheme before becoming coal secretary.

For the first time, RSBY placed the purchasing power in the hands of the patient, who could now choose to avail treatment at a hospital of their choice — public or private. A major premise of such schemes is also that a cache of purchasing power will spur private investment in health care, especially in rural or underpenetrated areas.

PMJAY retains the fundamentals of RSBY, while expanding the scope and size of coverage, adding more sophisticated IT infrastructure and more and sharply defined medical packages. Ayushman Bharat actually has two components : the PMJAY insurance scheme run by the National Health Authority, and a scheme to upgrade 1,50,000 primary health subcentres into health and wellness centres (HWC), run by the ministry of health. While PMJAY is a high-profile scheme, with data dashboards, outreach teams and the PM’s at tention, you hear relatively little about the progress on HWCs, much to the annoyance of public health specialists and those who work closely with communities.

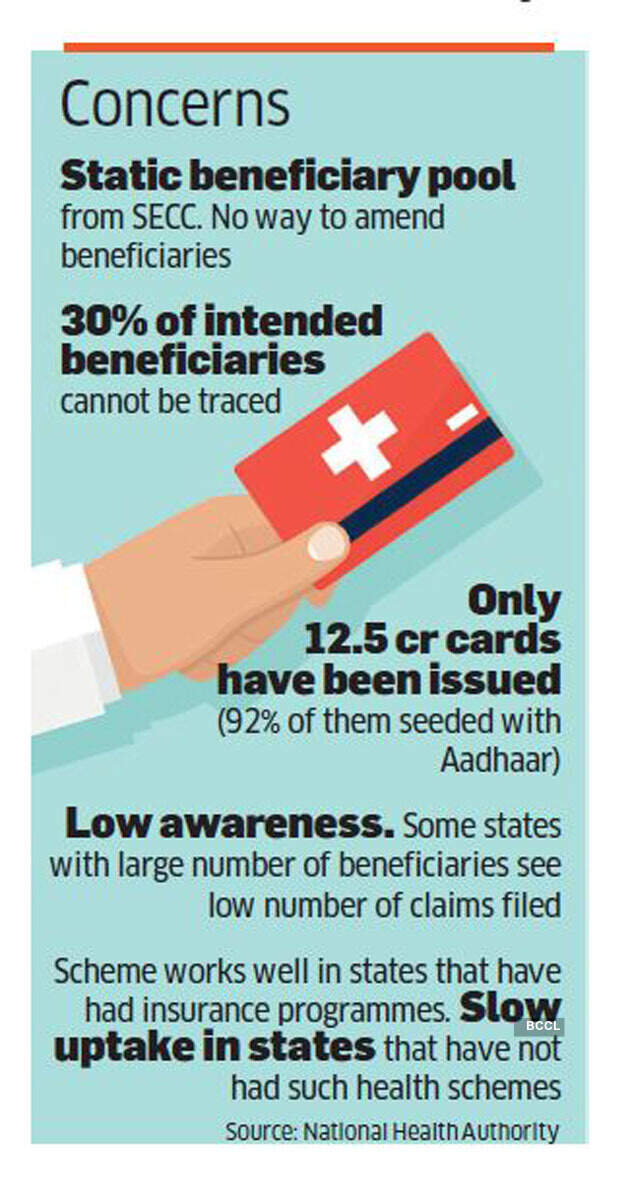

The database of PMJAY beneficiaries has been derived from the Socio Economic and Caste Census (SECC) of 2011. But some 30% of them have never been tracked. And the database is locked, which means as of now amendments are not possible. In an interview with ET Magazine, PMJAY CEO Indu Bhushan said they were working on different models to refine the database but a policy decision had to be taken to actually amend it. Nobody knows how many beneficiaries are aware of the scheme. About 12 crore beneficiary cards have been issued, including to 5 crore members inherited from RSBY. They are certainly aware.

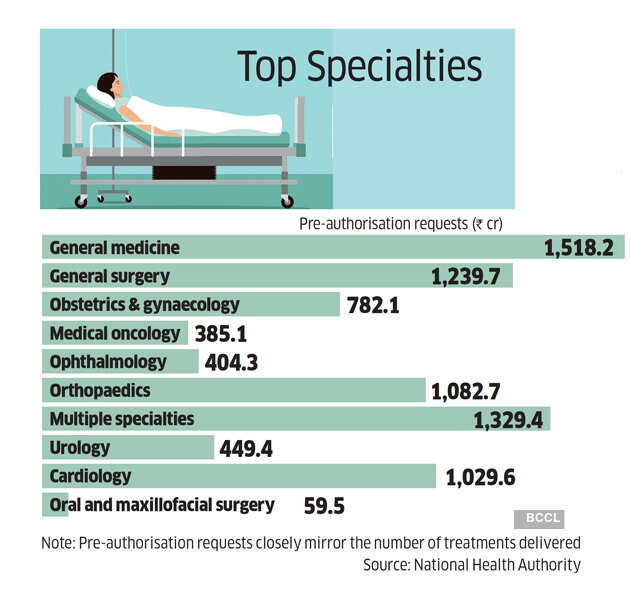

The ideal way the scheme is envisaged to work is as follows. A patient visits a hospital and is diagnosed with a condition requiring hospitalisation. A facilitation guide or Ayushman Mitra — typically an employee of the state health department — will help the patient through enrolment (if she doesn’t already have a card) and the hospital staff will seek pre-authorisation for an appropriate package or procedure (there are 872 packages and 1,573 procedures to choose from), seeking pre-authorisation through the portal. Once pre-authorisation is approved, the hospital can commence treatment. It is supposed to cover the cost of all medicines and consumables during the treatment and the patient is not required to pay anything.

The Centre foots 60% of the cost of the policy premium and the state picks up the rest. But in practice, it doesn’t always work like that.

Collective Bargaining

A big advantage of schemes such as PMJAY is that it can drive down prices with the leverage of volumes — in effect, it bargains on behalf of the collective of its beneficiaries. In many cases, this leads to prices that are too low to be viable for hospitals. But the volumes the scheme offers are too tempting to pass up, especially in states where utilisation is high. If your catchment area has a significant number of PMJAY beneficiaries, then not empanelling is a bit of a Hobson’s choice — you might be driven out of business otherwise.

What doctors and hospitals then end up doing in many cases is to tell the patient, whose awareness of the scheme and its cashless guarantee is limited, to co-pay. In some cases the hospital will say certain consumables or expensive items such as implants are not covered under the scheme and will be out-of-pocket expenses for the patient. Asymmetrical information, a scourge of healthcare in general, becomes acute in subsidised health insurance. The PMJAY does its best to counsel patients to not pay anything from their pockets but in practice, stakeholders say, it doesn’t always work. The danger of unattractive pricing of certain packages is also that hospitals might under-diagnose, in borderline cases, if they detect unwillingness to co-pay. But if the pricing is attractive, the system starts seeing a huge rise in the utilisation of that price or package.

The price has to be just right. But this is not a PMJAYspecific problem. It’s a bug of all subsidised health insurance schemes. “Such schemes cause distortion. If the national average of caesarian sections is 13% of all deliveries, in some districts it’s 70%. That’s because such schemes are available and hospitals like to do it,” says Keshav Desiraju, a former Union health secretary. PMJAY’s fix for is to require detailed documentation and proofs in the form of diagnostic scans, which are uploaded to the portal. But this creates its own problems.

“We understand the system is trying to fight abuse, but an Xray after a procedure to remove renal stones is unnecessary. CT scans and MRIs are required after many procedures, which adds to the cost and exposes the patient to radiation unnecessarily. ICU admissions need arterial blood gas reading, which is not available in all ICUs. This requirement reduces the availability of ICU beds. Hernia cases used to require ultrasound. But it can be medically diagnosed easily. Now they have removed that requirement,” says Dr Sushil Patil, a programme coordinator with Jan Swasthya Sahyog, a community healthcare programme in Chhattisgarh that operates a multi-specialty hospital and works with PMJAY.

The bigger issue doctors encounter most frequently, Patil says, is the unavailability of an appropriate package. In tuberculosis, for instance, packages are only available for pericardial or pleural tuberculosis. But patients come with conditions such as pulmonary, extrapulmonary, skeletal or other kinds of TB. Then doctors face difficulty in getting clearance. “We can talk to them. Sometimes the justifications get accepted, and sometimes they don’t,” Patil said.

States also do their part in monitoring and correcting distortions. In Chhattisgarh, procedures that were being carried out in large numbers, such as hernioplasty, caesarean section and hydrocelectomy, are now permitted only in government hospitals. PMJAY incorporates feedback and periodically fine-tunes the medical benefit packages. In January this year, it published the first revised package, leaving the date of implementation to states.

But fundamental to all these issues is chronic underfunding, says the head of a private healthcare operator who asked to remain anonymous as his company works closely with PMJAY. “The per capita medical expenditure in India is about $60. Let’s say half of that goes in primary care. So take $30 and multiply it with 4.2, which is the average size of a family in India. So the policy premium for a beneficiary family should be about $120.” The average scheme-wide premium paid by PMJAY is about one-ninth of that.

“This is the root of all problems. Even with the low rates for packages, this cannot be viable for insurance companies. They are bidding these unrealistically low rates because they are counting on uptake remaining low. So the moment someone starts billing at scale, they clamp down, raise objections and start saying people are committing fraud,” he says. Public health experts concur on the point about the scheme being underfunded. “The scheme is highly underfunded. The mathematics didn’t quite match the hype even when it was announced,” says Rama Baru, professor at the Centre for Social Medicine and Community Health at the Jawaharlal Nehru University, Delhi.

Access and Awareness

It’s hard to overstate the necessity of a scheme like PMJAY in India where unexpected healthcare expenditure can spell disaster for families. The Public Health Foundation of India estimated in a 2018 study that 5.5 crore Indians are pushed below the poverty line every year due to health care expenditure. Access to treatment cannot just spell the difference between a stable life and penury but indeed between life and death.

On the morning of January 28, Rahul Gaud, a resident of Bahraich district in UP, left his home for his BEd classes on his motorcycle. As he negotiated a turn, a nilgai pounced upon his vehicle. He fell with the left side of his face hitting the road hard.

His left jaw sustained three fractures. He first sought treatment at Bahraich district hospital and then was referred to Lucknow Medical College for surgery. He says his PMJAY card took care of the expenses. “We got support from the doctors, it was a stress-free process,” he says. The experience of Awadesh Maurya, 48, a resident of Majhawa in Mirzapur, UP, was starkly different. When his wife Sheela was diagnosed with cervical cancer in June 2019, he says hospitals would not accept the PMJAY card.

“We first went to BHU (SSH Hospital), where they said the relevant treatments were not available. Then we took her to Mumbai. First to a hospital in Malad, where they charged me Rs 40,000 for three days without even telling me what was happening. I said this was looting and we took her to Cama Hospital. There they said we only accept Rajiv Gandhi (RG Jeevandayee Arogya Yojana was the name of a state health scheme in Maharashtra). Then we took her to Tata Memorial. They sent me from one building to another and I couldn’t understand anything. So I paid the money and told them to start the treatment. When we went for radiation, they said, ‘you are eligible for Ayushman Bharat but now that you have started the treatment nothing can be done’.”

Maurya says social workers at the Tata Memorial Hospital helped raise part of the money for the treatment. Sheela recovered and the family stayed on in Mumbai for a few months for follow-up checks. While she recovered fully from cancer, she contracted dengue in October and rapidly deteriorated. She passed away on October 29. Maurya does not try to hide how distraught he is by the death of his wife. He is reluctant to say how much he had to spend for her treatment. Upon pressing, he says the family spent more than `8 lakh. He works in a garment unit that makes Banarasi saris. “What could I do? These hospitals are so big. Nobody was willing to help. You can get lost in some buildings. And my wife was very sick. I just wanted her treatment to begin,” he says.

Sheela was precisely the kind of person PMJAY was intended to benefit. But the lack of awareness among patients (Maurya didn’t know he could call a helpline or seek out an Ayushman Mitra at a hospital) and the failure of hospitals to properly guide a poor patient meant that the family could not access the benefit meant for them.

The scheme’s utilisation and quality of functioning varies widely between states. In states where existing schemes got merged with Ayushman Bharat, the utilisation rates are good. In states where Ayushman Bharat is the first such scheme in a while (some states discontinued RSBY after the UPA went out of power in 2014), the utilisation and awareness are low. In UP, where there are 3.2 crore beneficiary families (and about 13 crore beneficiaries if you apply the average family size multiple of 4.2), only 3.8 lakh pre-authorisation requests have been made.

PMJAY CEO Bhushan says ensuring more homogenisation across states is a top priority.

Public Benefit

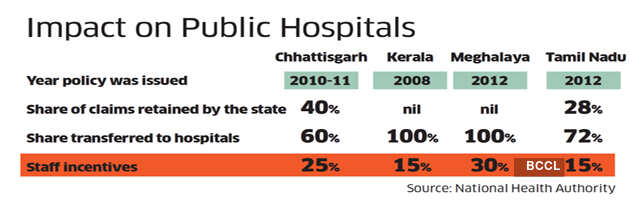

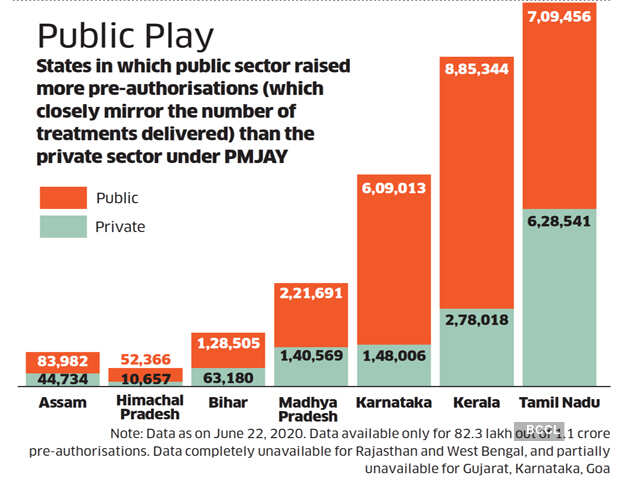

For government hospitals around the country, PMJAY could become a game changer. In 2008, when RSBY was introduced, Dinesh Arora IAS, who was then heading the National Rural Health Mission in Kerala, decided that government hospitals that participated in the RSBY programme could keep the money from the insurance scheme, and use it to improve its infrastructure to better compete with private hospitals, and also pay cash incentives to staff. “Within three years of implementation, 75% of RSBY money was going to public hospitals and 25% to private hospitals,” says Arora, who is now secretary of power in Kerala government.

This advantage continues to this day. Now only 23.8% of pre-authorisation requests from Kerala come from the private sector. The rest are from government hospitals, which means they are doing a superior job in attracting patients. Nationally, 60% of PMJAY money goes to the private sector but in states where such schemes have for a while allowed government hospitals to keep the money from insurance schemes to improve, the balance is tilted in favour of state-run hospitals (See “Power Play”). While this can be seen as PMJAY’s impact in improving private hospitals, the private healthcare provider who spoke on the condition of anonymity says that’s a wrong way to look at it. “If you have to calculate the cost of delivery of that treatment, you have to take into account the capital expenditure and also the operating expenditure of a hospital. The government hospital is already funded. So this gives them a huge margin and they are very happy because there are cash incentives. The private operator is expected to compete while also paying for capex and op-ex. How is this fair?” he asks.

Could PMJAY spur private investment in healthcare in tier-2 and -3 towns? “Private hospitals have not exactly rushed into tier-2 and -3 towns because of these schemes,” says Sujatha Rao, former Union health secretary.

The private health operator says it is not just a matter of demand. “It takes more than 35 licences to open and run a hospital. The compliance requirements are onerous. You need a clearance from the Atomic Energy Regulatory Board to operate an X-ray machine, for example. Also, unless the system guarantees settlements within 30 days or penal interest on outstanding, it’s too risky. Operating expenses are very high and margins are thin in health care. Banks run away from funding projects the moment we say the client is the government.”

Before PMJAY is expanded and potentially scaled to become the model for India’s universal health care ambitions, there’s work to be done.