Clipped from: https://www.business-standard.com

Terms on upgrade of accounts also likely to be tweaked as the central bank’s June 7 circular may get a relook

Well-placed sources said discussions were on between the banking regulator and senior bankers on the thresholds under the circular, which are almost impossible to be adhered to after the outbreak of the Covid-19 pandemic.

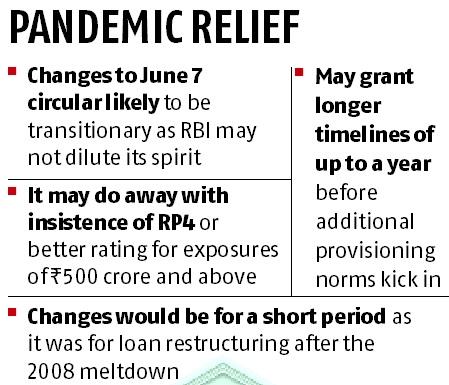

The Reserve Bank of India (RBI) may review its June 7 circular’s key trigger points on additional provisioning and the terms to upgrade accounts.

A view that is gaining traction is the grant of longer timelines of up to a year before additional provisioning norms kick in, and reducing it by, say, 10 per cent — from 20 per cent after 180 days from the end of the review period; and from 15 per cent after a year — or a reduction in the additional provisioning to 15 per cent from 35 per cent.

Well-placed sources said discussions were on between the banking regulator and senior bankers on the thresholds under the circular, which are almost impossible to be adhered to after the outbreak of the Covid-19 pandemic.

The changes, however, would be for a short period. Like the exception for one-time loan restructuring after the Lehman Brothers meltdown in 2008. Multiple sources said the RBI might not dilute the spirit of its June 7 guidelines. On June 7, 2019, the RBI had issued revised guidelines for resolution of stressed assets, under which lenders had to mandatorily enter into an inter-creditor agreement (ICA) during the review of the borrower account within 30 days of the first default to any lender.

“It (circular) has suitably empowered us, but some of what is in it may have to be rethought now,” said a banker. The circular needs to be revisited as many resolution plans could not be implemented, and banks are in capital conservation mode.

ALSO READ: Banks sanction Rs 75,000-cr loans to MSMEs under credit guarantee scheme

A case is also being made for relaxing the terms for the upgrade of accounts. As on date, standard accounts classified as non-performing assets and those in the same category on restructuring may be upgraded only when all outstanding loans demonstrate ‘satisfactory performance’ from the date of implementation of the resolution plan up to the date by which at least 10 per cent of outstanding principal debt is repaid. The account also cannot be upgraded before one year from the commencement of the first payment of interest or principal (whichever is later).

A related point of contention is that independent credit evaluation of the residual debt by credit rating agencies for exposures of Rs 500 crore and above should have a credit opinion of RP4 or better – the RBI has defined debt with RP4 as having a moderate degree of safety.

“In the post-Covid world, it is tough to wait for a year to get upgraded as additional funding may be needed in most cases or get such an RP4 opinion,” said a banker. Another banker said: “Anyway, all resolution plans may have to be reworked even as stress has only increased in these accounts.”

The June 7 circular is now being revisited due to the references to the extraordinary circumstances in earlier RBI communiques.

While the RBI’s June 7 circular does not contain the word “pandemic”, its master circular of July 1, 2015, mentions it — “There can be situations where a bank is put unexpectedly to loss due to events such as civil unrest or collapse of currency in a country. Natural calamities and pandemics may also be included in the general category. All these factors, which are beyond the control of the promoters, may lead to delay in project implementation and involve restructuring and reschedulement of loans by banks.”

During the discussions it has been pointed out that “the Covid-19 pandemic should be seen as a force majeure and a natural calamity in the health space”. But if the RBI were to treat Covid-19 as a force majeure, all contracts could be opened up. A top lawyer said: “A few contracts have adverse material changes incorporated in them, but these have not really been tested.”

One-time restructuring of loans due to Covid-19 is also on the cards. The RBI’s June 7 circular states the under “exceptions” restructuring in respect of projects involving deferment of date of commencement shall continue to be covered under the guidelines contained in the master circular of July 1, 2015.