Clipped from: https://economictimes.indiatimes.com

Covid impact: Job losses, pay cuts leading to surge in home loan defaults

IMGC guarantees 20% of the loan amount which covers EMIs for nearly two years. Once an account becomes a non-performing asset, the guarantee company pays the EMIs to the lender on the borrower’s behalf. IMGC has 15 lender clients, including ICICI Bank, Axis Bank, LIC Housing Finance, HDFC and SBI.

Mumbai: Mortgage, considered the safest segment of lending in India, is showing signs of cracks as the delinquencies at India Mortgage Guarantee Corporation (IMGC) nearly doubled from the year-ago levels, reflecting the stress of job losses and salary cuts.

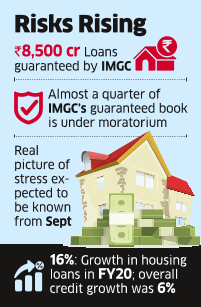

IMGC, which has guaranteed loans worth ₹8,500 crore, has seen the affordable home segment contributing the highest to defaults. With almost a quarter of its guaranteed book under moratorium, the real picture of the stress is expected to be known from September onwards.

“If we have to look at our delinquencies at the start of this financial year, they are nearly double of what they were last year. From August 2019 our delinquency numbers have started inching up gradually,” IMGC chief executive Mahesh Misra said. “As of now we have not been able to ascertain the Covid impact and will wait for the moratorium to be lifted to have a better sense of repayment behaviour.”

Misra said he could not reveal the delinquency figure as it was sensitive information due to a concentration of a few client banks on the firm’s books.

IMGC guarantees 20% of the loan amount which covers EMIs for nearly two years. Once an account becomes a non-performing asset, the guarantee company pays the EMIs to the lender on the borrower’s behalf. IMGC has 15 lender clients, including ICICI Bank, Axis Bank, LIC Housing Finance, HDFC and SBI. With mortgage stress rising, it expects to sign on five more lender partners in the coming weeks.

According to IMGC, a quick study of its portfolio showed that customers that were traditionally perceived as high-risk had demonstrated elevated levels of asset quality pressure. Moratorium percentages are higher among people who had poor credit scores when they took the loan. Also, borrowers with over 80% loan-to-value ratio have elevated moratorium levels.

With retail stress on the rise, experts believe lenders would tighten their credit policies to manage risk, in turn, leading to lower loan growth in this segment. “With 26% to 40% of the loan book under moratorium for private banks, we expect them to be extremely cautious in the retail loan segment given the challenges around pay cuts and job losses, leading to a loan growth pressure on this segment,” Macquarie Capital associate director Suresh Ganapathy said.

Housing loans have been the mainstay of growth among retail loans, which grew over 16% in the fiscal year ended March 2020. This when overall credit growth slowed to a six-decade low of 6%. While the overall bad loan ratio is upwards of 9%, it is less than 2% in the retail category. But job losses and salary cuts due to the outbreak of Covid-19 could spoil the party.

“We expect that demand for secured lending products like auto loans and home loans will likely remain weak for some time,” said Abhay Kelkar, vice president of research and consulting at TransUnion CIBIL.