Read more at: https://taxguru.in/income-tax/pune-itat-section-263-revision-invalid-aos-proper-enquiry.html?utm_source=follow.it

Copyright © Taxguru.in

Digital Risk Mortgage Services LLC Vs ACIT (ITAT Pune)

Pune ITAT Quashes Section 263 Revision – Once AO Has Conducted Enquiries and Taken a Plausible View, PCIT Cannot Order Fresh Investigation

The Pune ITAT quashed the revisionary order under section 263, holding that the Principal CIT cannot invoke section 263 merely because he believes the Assessing Officer should have conducted a more detailed enquiry. The assessee had claimed deductions under sections 10AA and 80JJAA, and the assessment was selected for complete scrutiny. During the assessment proceedings, the Assessing Officer issued specific questionnaires and a detailed show-cause notice, calling for information regarding the eligibility of the deductions. The assessee furnished comprehensive details, including employee-wise data, salary particulars, working days, transfer of employees to the SEZ unit, and other supporting documents, after which the Assessing Officer accepted the claims. The Tribunal found that the PCIT ignored these materials and merely alleged inadequate verification without identifying any defect in the evidence or demonstrating that the statutory conditions were not fulfilled.

Relying on the decisions of the Supreme Court in Malabar Industrial Co. Ltd. and V-Con Integrated Solutions (P.) Ltd., as well as several High Court rulings, the Tribunal reiterated that section 263 cannot be invoked to order a fishing or roving enquiry once the Assessing Officer has made enquiries and adopted a plausible view. It emphasised the distinction between “lack of enquiry” and “inadequate enquiry”, observing that once the Assessing Officer raises queries and considers the assessee’s replies, it is not necessary for the assessment order to discuss every issue in detail. Since the PCIT neither found any fault with the assessee’s submissions nor established that the assessment order was both erroneous and prejudicial to the interests of the Revenue, the revision under section 263 was held to be unsustainable and was quashed. The assessee’s appeal was allowed.

FULL TEXT OF THE ORDER OF ITAT PUNE

This is an appeal filed by the assessee against the order u/s 263 of the Income Tax Act, 1961 for AY 2020-21 passed on 28.03.2025 by Commissioner of Income Tax (IT&TP), Pune emanating from assessment order u/s 143(3) r.w.s. 144C dated 08.04.2022.

2. The Assessee has raised following grounds of appeal :

“1. The notice issued under section 263 of the Act and the order passed under section 263 of the Act are illegal as the same are not in conformity to the basic requirements of section 263.

2. Without prejudice to above, the notice and proceedings under section 263 are invalid as the order passed by AO u/s 143(3) r.w.s 144C was neither erroneous nor prejudicial to the interest of revenue.

3. Without prejudice to the above, the AO having duly verified all the grounds for initiating revisionary proceedings under section 263 of the Act, the order of the AO cannot be held to be erroneous nor prejudicial to the interest of the revenue to be amenable to the provisions of section 263 of the Act and consequently the order passed under section 263 deserves to be quashed as per law and in the interest of justice.

4. The exercise of revisionary powers by the CIT is contrary to the ratio led down by the Honble Supreme Court in Malabar Industrial Co Ltd as the Respondent has failed to apply judicial mind and demonstrate how the AO’s Full scrutiny assessment order is erroneous AND prejudicial to Revenue; The application of CBDT circular 14/2014 in impugned Assessment year is also overtly erroneous and invocation of Revisionary powers on the basis of an allegation of “lack of enquiry” by AO is unfounded as all material facts, evidences were submitted, available in the records of Revenue and already accepted by AO during scrutiny proceedings.

5. On the facts and circumstances of the case and in law, the claim of benefit of exemption and deduction under section 10AA and 80JJAA being legally allowable and which was rightly allowed by the AO after due verification, the same cannot be the basis of invoking the provisions of section 263 of the Act making the order passed under section 263 grossly illegal and which deserves to be quashed as per law and in the interest of justice.

6. The Appellant craves leave to add, amend, alter, vary and/or withdraw any or all the above grounds of Appeal with the kind permission of the Hon’ble Tribunal.”

3. Basic Facts:

The assessee is a company incorporated in United States of America and is non-resident company in India. The assessee company has set up a branch in Pune viz. Digital Risk Mortgage Service LLC, India to render off-shore services to its head office and other group companies. Assessee has a permanent establishment in India. Assessee had filed return of income for AY 2020-21 u/s 139(1) on 12.02.2021 declaring total income of Rs.17,82,17,280/-. Assessee also electronically filed Form 3CEB, Tax audit report and Form 56F. Assessee had claimed deduction u/s 80JJAA and 10AA of the Act. The assessee‟s case was selected for scrutiny accordingly various notices were issued by the Assessing Officer (AO). The AO passed an assessment order deciding total income at Rs.18,89,75,632/-. In the assessment order dated 08.04.2022 for AY 2020-21, AO allowed assessee deduction u/s 10AA and 80JJAA of the Act.

3.1 The Ld. Commissioner of Income Tax (IT&TP), Pune [herein called as “CIT(IT&TP”)] invoked jurisdiction u/s 263 of the Act. The CIT(IT&TP) passed order u/s 263 of the Act for AY 2020-21 on 28.03.2025, after considering submissions of the assessee. The relevant paragraphs of the order u/s 263 are produced here under :

“2.5 A careful examination of the assessment records reveals that the Assessing Officer (AO) did not conduct a comprehensive and meaningful inquiry into the eligibility of the assessee’s claim for deduction under Section 10AA. Although a notice seeking justification for the 10AA claim was issued, and certain details were submitted in response, the critical details necessary for verifying compliance with statutory conditions were neither called for nor examined adequately.

Specifically, essential information such as:

-

- The number of technical manpower transferred from the old unit to the SEZ unit,

- The total number of technical manpower employed at the end of the year in the SEZ unit, and

- The percentage of redeployed manpower vis-à-vis newly hired manpower,

were not obtained or examined by the AO. These details, supported by adequate documentary evidence (appointment letters, PF slips etc.) are crucial for determining whether the assessee meets the conditions prescribed under Section 10AA, particularly in light of CBDT Circular No. 14/2014, which lays down clear guidelines on the redeployment of technical manpower for IT/ITES SEZ units.

The absence of these fundamental inquiries suggests that the AO did not apply his mind to a key eligibility criterion for the 10AA deduction. Without verifying whether the manpower redeployment threshold was adhered to, the AO could not have arrived at an informed and legally sustainable conclusion regarding the assessee’s eligibility for deduction. Mere receipt of submissions from the assessee mentioning that the eligibility conditions are fulfilled, without proper scrutiny and cross-verification, does not constitute a valid examination of the issue.

In light of these omissions, it is evident that the assessment order was passed without making the necessary inquiries or verification that should have been made. Consequently, in terms of Explanation 2(a) and (b) to Section 263, introduced by the Finance Act 2015, the order is deemed to be both erroneous and prejudicial to the interests of the revenue.

3.6 As mentioned, although AO during the assessment proceedings did issue a general notice asking assessee to substantiate its claim, a perusal of the notices and submissions in this respect reveals that the AO did not conduct specific verification of the assessee’s claim. While the assessee claimed the benefit under this section, no meaningful inquiry was carried out to ensure compliance with the statutory conditions prescribed therein. Specifically, the AO failed to call for or examine crucial details such as:

-

- The list of employees for whom the deduction was claimed, along with proof of their actual period of employment to verify whether they were employed for more than 240 days in the relevant previous year.

- The Provident Fund (PF) registration and contribution records to ensure that the employees were duly enrolled in a recognized provident fund, as mandated under the Act.

- Salary registers and payroll records to verify that the monthly emoluments of each eligible employee did not exceed 25,000.

3.7 Without a thorough examination of these critical aspects, the AO could not have ascertained whether the assessee fulfilled the eligibility conditions for claiming deduction under Section 80JJAA. Mere acceptance of the claim without independent verification does not amount to a proper application of mind. Given these omissions, it is evident that the assessment order was passed without making inquiries or verification that were imperative for determining the validity of the claim. In light of Explanation 2(a) and (b) to Section 263, as introduced by the Finance Act, 2015, the order is deemed to be erroneous and prejudicial to the interests of the revenue. Therefore, the AO’s failure to conduct a proper inquiry into the eligibility of the assessee’s claim under Section 80JJAA warrants revision under Section 263 of the Act.”

3.2 Aggrieved by the order u/s 263 of the Act, the assessee has filed appeal before this Tribunal.

4. Submission of Ld. AR:

The Ld. AR filed a factual paper book containing 875 pages and case laws paper book along with written submissions. The Ld. AR invited our attention to various notices issued u/s 142(1) of the Act and show cause notice dated 28.01.2022 which are in the paper book to argue that AO had carried out proper inquiry regarding assessee’s claim for deduction u/s 10AA and 80JJAA of the Act. Ld. AR invited our attention to page Nos. 157, 193, 367, 379 and 467 of the paper book and submitted that all the details were filed by the assessee during the assessment proceedings. Ld. AR further submitted the AO after considering the elaborate reply of the assessee allowed assessee deduction u/s 10AA and 80JJAA of the Act. Ld. AR specifically invited our attention to page No. 379 of the paper book and submitted that the details of employees along with their salary were filed during assessment proceedings. Ld. AR therefore submitted that the PCIT’s allegation that AO had not verified details of employees is factually incorrect. The relevant paragraphs of the submissions of the Ld. AR are reproduced here as under :

“A. The order passed by the CIT u/s 263 of the Act is without Jurisdiction

9. Section 263 of the Act confers the power upon the CIT to call for and examine the records of proceeding under the Act and revise any order only if he (the CIT) considers the same to be erroneous and prejudicial to the interests of the revenue and this power to revise is subject to various checks and balances.

10. As settled by the Hon’ble Supreme Court in Malabar Industrial Co. Ltd. vs. CIT [243 ITR 83], an order can be revised only if both conditions are satisfied:

(i) Order is erroneous; and

(ii) It is prejudicial to the interest of revenue.

11. Further, to understand the meaning of “erroneous in so far as it is prejudicial to the interests of the revenue”, the Appellant would like to place reliance on Explanation 2 of section 263(1) of the Act, which states in which manner an order passed can be treated as erroneous or prejudicial to the interest of revenue, which is as under:

(a) the order is passed without making inquiries or verification which should have been made;

(b) the order is passed allowing any relief without inquiring into the claim;

(c) the order has not been made in accordance with any order, direction or instruction issued by the Board under section 119; or

(d) the order has not been passed in accordance with any decision which is prejudicial to the assessee, rendered by the jurisdictional High Court or Supreme Court in the case of the assessee or any other person.

12. Clause (c) and clause (d) of the aforesaid explanation are not applicable to the case at hand. The clauses relevant to the present case are clauses (a) and (b).

13. The conjoint reading of aforesaid clauses (a) and (b) clarifies the fact that the revision u/s 263 of the Act can be only adopted if the order is passed or relief is granted without making proper verification and enquiry.

14. The above-mentioned criteria must be satisfied mandatorily to exercise a valid revisionary power u/s 263 of the Act.

15. The facts relevant to establish that proper verification and enquiry was conducted by the Ld. AO are as follows:

(i) For the impugned year, the case of the Appellant was selected for complete scrutiny under CASS and notice u/s 143(2) of the Act dated 29th June 2021 was issued wherein the issues as specified requiring further clarification was mentioned as “Deduction claimed for industrial undertaking u/s 801A/801AB/801AC/IB/IC/IBA/80ID/80IE/10A/10AA.” A copy of the said notice is enclosed in Annexure -1.

(ii) During the assessment proceedings, the AO raised various queries throughout the assessment proceedings which includes queries in relation to the claims made u/s10AA of the Act and 80JJAA of the Act. Against the said queries, the Appellant made detailed submissions from time to time.

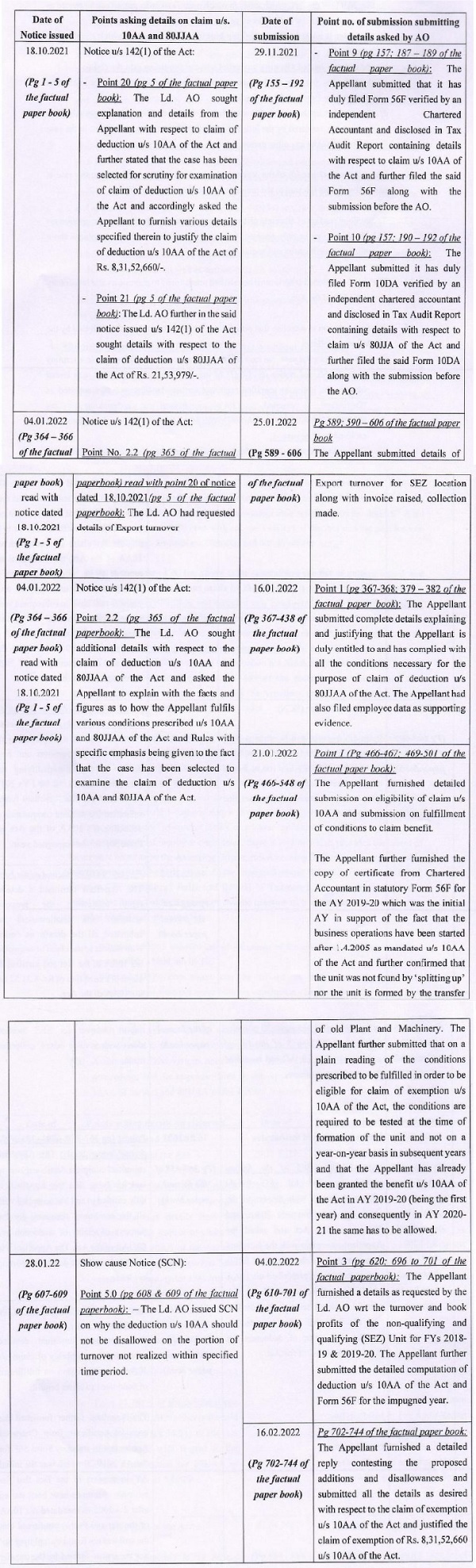

(iii) A summary of the various notices issued by the Ld. AO during the assessment proceedings and the responses filed by the Appellant on allowability of claim u/s 10AA of the Act and 80JJAA of the Act are as under:

(iv) The AO then proceeded to issue draft order u/s 144C of the Act dated 28th February 2022 proposing disallowance u/s 40(a)(ia) and 40(a)(i) of the Act and AO then finally proceeded to complete the assessment vide assessment order dated 8th April 2022 passed u/s 143(3) read with section 144C(3) of the Act making additions on account of disallowance u/s 40(a)(ia) and 40(a)(i) of the Act.

16. From the Annexures- 1 & the above table (containing the list of notices issued and the corresponding submissions made by the Appellant) annexed herewith above, it is clear that proper verification and enquiry was conducted by the Ld. AO as during the original assessment proceedings, with respect to claims made u/s 10AA and 80JJAA of the Act, relevant questionnaires were issued by Ld. AO on the Appellant against which the Appellant had duly filed detailed submission. Also, the Ld. AO had issued final Show Cause Notice (SCN) on claim of deduction u/s 10AA of the Act dated 28th January 2022 (copy enclosed in Page Nos. 607-609 of the factual paper book) and after considering the detailed submission filed by the Appellant, the Ld. AO had not made any adverse adjustment in the final assessment order.

19. The CIT in the case at hand has conducted the revisionary proceedings u/s 263 of the Act on account of change in opinion, which is not permissible in law.

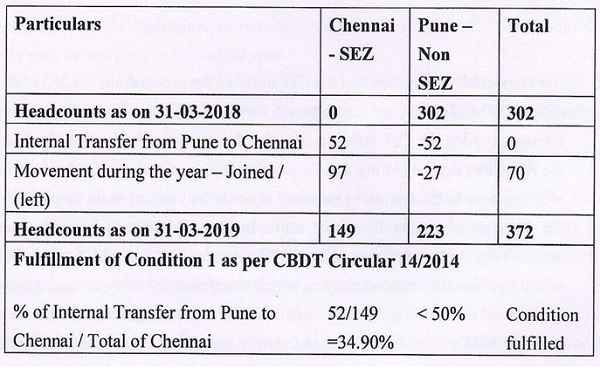

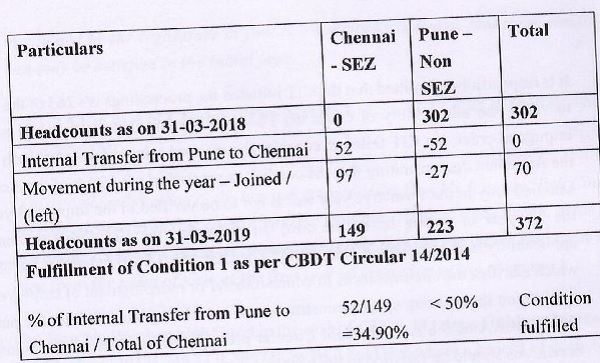

33. In this regard, during the proceedings u/s 263 of the Act, the Appellant had specifically brought to the attention of the CIT that it operates two units, namely (i) an SEZ unit at Chennai and (ii) a Non-SEZ unit at Pune. The Chennai SEZ unit commenced operations on 30 April 2018, i.e. during FY 2018-19. Accordingly, the conditions for claiming deduction u/s 10AA of the Act were required to be examined in FY 2018-19 relevant to AY 2019-20. The Appellant had furnished the employee movement details, summarized as under:

34. Based on the above, the percentage of employees transferred from the Pune unit to the Chennai SEZ unit works out to 52/149 = 34.90%, which is well below the threshold of 50% prescribed under CBDT Circular No. 14/2014. Accordingly, the unit-level condition stands fulfilled. Thus, it is evident that in the year of formation, less than 50% of the employees of the SEZ unit comprised transferred personnel from the existing unit, and therefore, the setting up of the SEZ unit cannot be construed as resulting from splitting up or reconstruction of an existing business. Consequently, the conditions stipulated u/s 10AA(4)(ii) read with CBDT Circular No. 14/2014 stood duly satisfied.

35. However, the Ld. CIT, without considering or dealing with the above submissions and factual details, proceeded to set aside the assessment order for fresh verification by Ld. AO. Such an approach clearly reflects non-application of mind and renders the assumption of jurisdiction u/s 263 of the Act unsustainable in law.

38. During the year, the Appellant made claim u/s 80JJAA of the Act as detailed hereinunder:

| Fresh claim (rs.) | Continuous Claim (Rs.) | Total (Rs.) |

| 2,065,716 | 88,263 | 2,153,979 |

40. With respect to the details of the eligible employees for claiming deduction u/s 80JJAA of the Act, the same had been provided to the Ld. AO during the Assessment proceedings vide submissions dated 16th January 2022 (copy enclosed in Page No. 379 of the factual paper book). In this regard, to examine the aforesaid details, the Hon’ble Bench had sought for a clearer copy of the same (having the details of the employees) and the same is enclosed herewith as Annexure 3 to this written submissions. As submitted before the AO, on a consistent basis, the average annual salary of such employees remains below the threshold of Rs.25,000 per month, and accordingly, they continue to satisfy the eligibility conditions prescribed u/s 80JJAA of the Act. It may be noted that in the list of eligible employees enclosed, in certain rare cases the monthly salary figures include non-recurring or variable components such as overtime payments, performance incentives, bonuses, or similar payments, and does not reflect any change in the regular or fixed remuneration structure of the employees.”

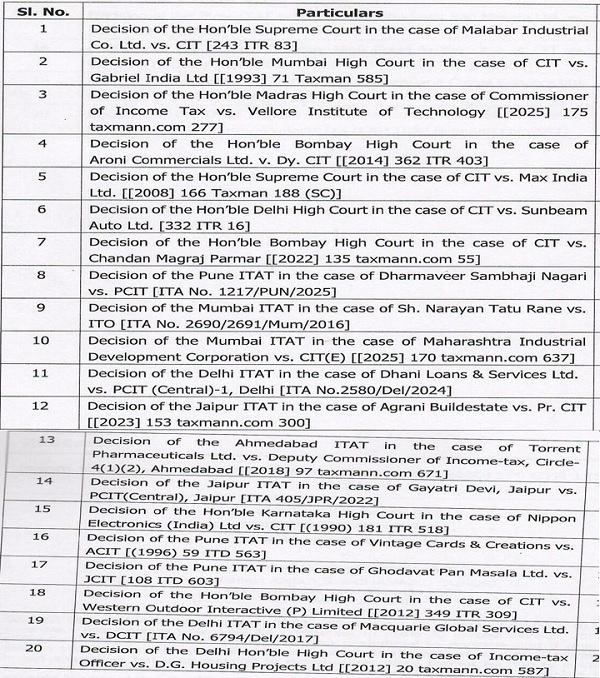

4.1 The Ld. AR further submitted that the CBDT Circular No. 14/2014 relied by Ld. CIT is applicable for the first year. Assessee was allowed deduction u/s 10AA of the Act for AY 2019-20 by the AO which was the first year. The Ld. AR further submitted once assessee was allowed deduction u/s 10AA of the Act for the first year without disturbing first year, assessee’s claim cannot be disallowed. Ld. AR invited our attention to Hon’ble Jurisdictional High Court decision in the case of CIT Vs. Western Outdoor Interactive (P.) Ltd., 349 ITR 309 (Bom.).

4.2 Ld. AR submitted that the order u/s 263 of the Act is not maintainable as assessment order neither erroneous nor prejudicial to the interest of Revenue. The Ld. AR relied on following decisions:

5. Submission of Ld. DR:

The Ld. DR relied on the order of the Ld. CIT(IT&TP). The Ld. DR submitted that as per explanation to Section 263 of the Act, it is the relative opinion of the Ld. CIT(IT&TP) which decides whether order is erroneous or not. Ld. DR read Explanation-2 to Section 263 of the Act. Ld. DR submitted that AO should have called for details regarding Provident Fund deduction to understand eligibility of the assessee for deduction u/s 80JJAA and 10AA of the Act.

6. Findings and analysis:

We have heard both the parties and perused the records. In this case, the assessee had filed return of income for AY 2020-21 u/s 139(1) of the Act claiming deduction u/s 80JJAA and 10AA of the Act. Assessee‟s case was selected for complete scrutiny.

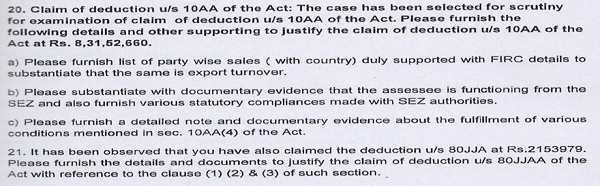

6.1 During the assessment proceedings, the AO asked specific questions vide notice u/s 142(1) of the Act dated 18.10.2021. The relevant questions asked by the AO are reproduced here as under :

6.2 Assessee filed reply on 16.01.2022 which is at page Nos. 367 to 382 of the paper book.

6.3 Then AO issued show cause notice dated 28.01.2022 which is at page Nos. 607 to 609 of the paper book. Assessee filed reply to the show cause notice which is at page Nos. 610 to 620 of the paper book. Assessee had filed details of employees during assessment proceedings which is at page No. 379 of the paper book. Ld. DR has not doubted the submission of the Assessee.

6.4 The Ld. AO considered all these replies filed by the assessee and then allowed assessee deduction u/s 10AA and 80JJAA of the Act.

6.5 In the order u/s 263 of the Act, the Ld. CIT(IT&TP) has alleged that AO failed to obtain number of technical man power transferred from old unit to SEZ unit, total number of technical man power employed in the SEZ unit, percentage of employed man power as per CBDT Circular No. 14/2014. Ld. CIT(IT&TP) had also alleged that AO had not examined crucial details such as list of employees, along with proof of their actual period of employment, PF Registration details and salary details. Mainly for these reasons, the Ld. CIT(IT&TP) held that the Assessment Order was erroneous and prejudicial to the interest of the revenue, accordingly passed an order u/s 263 of the Act.

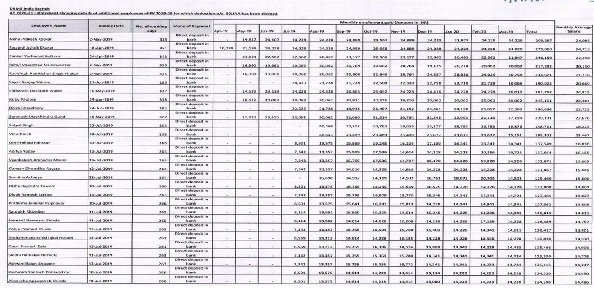

6.6 We have observed that assessee had filed list of employees along with number of working days during assessment proceedings. The part of the said list is scanned and reproduced here as under :

6.7 Similarly, the assessee had filed details of number of employees transferred to SEZ unit, the same is reproduced here as under :

6.8 The details of transferred employees were filed before Ld. CIT(IT&TP), however, Ld. CIT(IT&TP) had not commented on the submissions of the assessee regarding number of employees transferred and its claim that it fulfills conditions for deduction u/s 10AA of the Act.

6.9 Thus, on perusal of the submissions of the assessee, it is observed that assessee had filed all the details before Ld. AO and then before Ld. CIT(IT&TP). Ld. AO after considering the details allowed assessee deduction u/s 10AA and 80JJAA of the Act. Ld. CIT(IT&TP) alleged that the AO had not verified details of employees qua section 10AA and 80JJAA of the Act. Assessee had also filed those details before the Ld. CIT(IT&TP). We have reproduced the relevant details in our earlier paragraphs. Ld. CIT(IT&TP) has not found any fault with the details filed by the assessee. Rather, Ld. CIT(IT&TP) has not made any comment on the details filed by the assessee. Ld. CIT(IT&TP) merely set aside the assessment order to the AO for de-novo adjudication on the ground that AO failed to obtain number of technical employees, emoluments, monthly salary which are necessary for claiming u/s 10AA and 80JJAA of the Act. We have already observed in the earlier paragraphs and reproduced the relevant details that assessee had filed necessary details regarding the employees. In these facts, the Ld.CIT(IT&TP) should have commented on the details filed, should have verified the details filed by the Assessee qua eligibility for deduction claimed by assessee. There are no adverse inference or findings by the Ld.CIT(IT&TP) with reference to the elaborate submission of the Assessee. In these facts and circumstances of the case, we are of the considered opinion that Ld. CIT(IT&TP) had failed to prove that assessment order was erroneous and prejudicial to the interest of the Revenue. It has been observed by the Hon’ble Supreme Court in the case of Malabar Industrial Co. Ltd. Vs. CIT, 243 ITR 83 (SC) that provisions of section 263 cannot be invoked to correct each and every type of mistake committed by the Assessing Officer.

7. The Hon’ble Supreme Court of India in the case of Principal Commissioner of Income-tax-1 v. V-Con Integrated Solutions (P.) Ltd [2025] 476 ITR 526 (SC)[04-04-2025] held as under :

Quote, “3. The assessee does not have control over the pen of the Assessing Officer. Once the Assessing Officer carries out the investigation but does not make any addition, it can be taken that he accepts the plea and stand of the assessee.

4. In such cases, it would be wrong to say that the Revenue is remediless. The power under Section 263 of the Income Tax Act, 1961, can be exercised by the Commissioner of Income Tax, but by going into the merits and making an addition, and not by way of a remand, recording that there was failure to investigate. There is a distinction between the failure or absence of investigation and a wrong decision/conclusion. A wrong decision/ conclusion can be corrected by the Commissioner of Income Tax with a decision on merits and by making an addition or disallowance.

5. There may be cases where the Assessing Officer undertakes a superficial and random investigation that may justify a remit, albeit the Commissioner of Income Tax must record the abject failure and lapse on the part of the Assessing Officer to establish both the error and the prejudice caused to the Revenue.”

8. The Hon’ble High Court of Madras in the case of Commissioner of Income-tax v. Vellore Institute of Technology [2025] 305 Taxman 450 (Madras)[03-06-2025] has held as under :

Quote, “10. It is true that the assessment order dated 14.12.2011 does not discuss the queries raised or the answers given thereto. But the fact is, the Assessing Officer had issued a questionnaire dated 26.07.2011 under Section 142 (1) of the Act raising 34 questions on various issues and assessee had given an explanation and also submitted materials. In our view, once a notice is issued and assessee is called upon to show cause or give explanation or submit documents and assessee has complied, not giving a finding or discussing the same would mean that the Assessing Officer was satisfied with the explanation given by the assessee.

11. In Aroni Commercials Limited v. Dy. CIT [2014] 44 taxmann.com304 / 224 Taxman 13 (Mag.)/ 362 ITR 403 (Bom.),a Division Bench of the Bombay High Court, while dealing with the provisions of Section 148 of the Act, held that once a query is raised during the assessment proceedings and assessee has replied to it, it follows that the query was subject matter of consideration of the Assessing Officer while completing the assessment and the same is deemed to have been accepted. The Court also held that it is not necessary that an assessment order should contain reference and/or discussion to disclose its satisfaction in respect of each and every query raised. Therefore, as there is no discussion or finding on the 34 questions raised under Section 142(1) of the Act, vide the communication dated 26.07.2011, the Assessing Officer should be taken as having accepted assessee’s explanation. Paragraph 14 of Aroni Commercials Limited (supra) reads as under:

” 14) We find that during the assessment proceedings the petitioner had by a letter dated 9 July 2010 pointed out that they were engaged in the business of financing trading and investment in shares and securities. Further, by a letter dated 8 September 2010 during the course of assessment proceedings on a specific query made by the Assessing Officer, the petitioner has disclosed in detail as to why its profit on sale of investments should not be taxed as business profits but charged to tax under the head capital gain. In support of its contention the petitioner had also relied upon CBDT Circular No.4/2007 dated 15 June 2007. (The reasons for reopening furnished by the Assessing Officer also places reliance upon CBDT Circular dated 15 June 2007). It would therefore, be noticed that the very ground on which the notice dated 28 March 2013 seeks to reopen the assessment for assessment year 2008-09 was considered by the Assessing Officer while originally passing assessment order dated 12 October 2010. This by itself demonstrates the fact that notice dated 28 March 2013 under Section 148 of the Act seeking to reopen assessment for A.Y. 2008-09 is based on mere change of opinion. However, according to Mr. Chhotaray, learned Counsel for the revenue the aforesaid issue now raised has not been considered earlier as the same is not referred to in the assessment order dated 12 October 2010 passed for A.Y. 200809. We are of the view that once a query is raised during the assessment proceedings and the assessee has replied to it, it follows that the query raised was a subject of consideration of the Assessing Officer while completing the assessment. It is not necessary that an assessment order should contain reference and/or discussion to disclose its satisfaction in respect o f the query raised. If an Assessing Officer has to record the consideration bestowed by him on all issues raised by him during the assessment proceeding even where he is satisfied then it would be impossible for the Assessing Officer to complete all the assessments which are required to be scrutinized by him under Section 143(3) o f the Act. Moreover, one must not forget that the manner in which an assessment order is to be drafted is the sole domain of the Assessing Officer and it is not open to an assessee to insist that the assessment order must record all the questions raised and the satisfaction in respect thereof of the Assessing Officer. The only requirement is that the Assessing Officer ought to have considered the objection now raised in the grounds for issuing notice under Section 148 of the Act, during the original assessment proceedings. There can be no doubt in the present facts as evidenced by a letter dated 8 September 2012 the very issue of taxability of sale of shares under the head capital gain or the head profits and gains from business was a subject matter of consideration by the Assessing Officer during the original assessment proceedings leading to an order dated 12 October 2010. It would therefore, follow that the reopening of the assessment by impugned notice dated 28 March 2013 is merely on the basis of change of opinion of the Assessing Officer from that held earlier during the course of assessment proceeding leading to the order dated 12 October 2010. This change of opinion does not constitute justification and/or reasons to believe that income chargeable to tax has escaped assessment.

(emphasis supplied)

12. Therefore, we agree with the Tribunal that the Commissioner has exercised his power under Section 263 of the Act in an arbitrary manner and hence, the impugned order requires to be quashed. The substantial questions of law framed are answered accordingly. The Tax Case Appeal is dismissed. There shall be no order as to costs. ” Unquote.

9. The Hon‟ble High Court of Bombay in the case of Commissioner of Income-tax, Mumbai v. Chandan Magraj Parmar [2022] 445 ITR 674 (Bombay)[16-11-2021] has held as under :

Quote, “7. When it is not disputed that the land concerned would not fall under the definition of capital asset, the question of any capital gains arising also will not arise. Moreover, we also find that the ITAT has come to a factual finding that the AO has raised queries with regard to the claim of capital gain on transfer of land, Respondent vide its reply dated 31-1-2014 furnished the details in respect of distance of agricultural land from municipal limits, record of population as per last census and the AO after considering the reply of Respondent, accepted the claim of Respondent. The ITAT has given a finding that the claim of capital gain was accepted by AO after necessary inquiry and the order under section 143(3) of the Act was passed. It is true that the AO has not passed any written detailed order while accepting the explanation of capital gains of Respondent but the fact is AO had raised queries and Respondent has given detailed reply means the AO has passed this order after making necessary inquiries. We agree with the view of the ITAT that the order of the AO cannot be branded as erroneous merely because the order does not contain the details which Principal Commissioner feels should have been included. The Principal Commissioner cannot decide how elaborate an order of the AO should be. Where the AO, during the scrutiny assessment proceedings, has raised a query which was answered by the Assessee to the satisfaction of the AO but the same was not reflected in the AO by him, the Commissioner cannot conclude that no proper inquiry with respect to the issue was made by the AO and enable him to assume jurisdiction under section 263 of the Act.” Unquote.

10. The ITAT Mumbai Bench ‘B’ in the case of Narayan Tatu Rane v. Income-tax Officer, Ward 27(1)(1), Mumbai [2016] 70 taxmann.com 227 (Mumbai – Trib.) has held as under :

Quote, “19. The law interpreted by the High Courts makes it clear that the Ld Pr. CIT, before holding an order to be erroneous, should have conducted necessary enquiries or verification in order to show that the finding given by the assessing officer is erroneous, the Ld Pr. CIT should have shown that the view taken by the AO is unsustainable in law. In the instant case, the Ld Pr. CIT has failed to do so and has simply expressed the view that the assessing officer should have conducted enquiry in a particular manner as desired by him. Such a course of action of the Ld Pr. CIT is not in accordance with the mandate of the provisions of sec. 263 of the Act. The Ld Pr. CIT has taken support of the newly inserted Explanation 2(a) to sec. 263 of the Act. Even though there is a doubt as to whether the said explanation, which was inserted by Finance Act 2015 w.e.f.1.4.2015, would be applicable to the year under consideration, yet we are of the view that the said Explanation cannot be said to have over ridden the law interpreted by Hon’ble Delhi High Court, referred above. If that be the case, then the Ld Pr. CIT can find fault with each and every assessment order, without conducting any enquiry or verification in order to establish that the assessment order is not sustainable in law and order for revision. He can also force the AO to conduct the enquiries in the manner preferred by Ld Pr. CIT, thus prejudicing the independent application of mind of the AO. Definitely, that could not be the intention of the legislature in inserting Explanation 2 to sec. 263 of the Act, since it would lead to unending litigations and there would not be any point of finality in the legal proceedings. The Hon’ble Supreme Court has held in the case of Parashuram Pottery Works Co. Ltd. v. ITO [1977] 106 ITR 1that there must be a point of finality in all legal proceedings and the stale issues should not be reactivated beyond a particular stage and the lapse of time must induce repose in and set at rest judicial and quasi-judicial controversies as it must in other spheres of human activity.

20. Further clause (a) of Explanation states that an order shall be deemed to be erroneous, if it has been passed without making enquiries or verification, which should have been made. In our considered view, this provision shall apply, if the order has been passed without making enquiries or verification which a reasonable and prudent officer shall have carried out in such cases, which means that the opinion formed by Ld Pr. CIT cannot be taken as final one, without scrutinising the nature of enquiry or verification carried out by the AO vis-à-vis its reasonableness in the facts and circumstances of the case. Hence, in our considered view, what is relevant for clause (a) of Explanation 2 to sec. 263 is whether the AO has passed the order after carrying our enquiries or verification, which a reasonable and prudent officer would have carried out or not. It does not authorise or give unfettered powers to the Ld Pr. CIT to revise each and every order, if in his opinion, the same has been passed without making enquiries or verification which should have been made. In our view, it is the responsibility of the Ld Pr. CIT to show that the enquiries or verification conducted by the AO was not in accordance with the enquries or verification that would have been carried out by a prudent officer. Hence, in our view, the question as to whether the amendment brought in by way of Explanation 2(a) shall have retrospective or prospective application shall not be relevant.

21. In the instant case, as noticed earlier, the AO has accepted the explanations of the assessee, since there is no fool proof evidence to link the assessee with the document and M/s RNS Infrastructure Ltd, from whose hands it was seized, also did not implicate the assessee. Thus, the assessee has been expected to prove a negative fact, which is humanely not possible. No other corroborative material was available with the department to show that the explanations given by the assessee were wrong or incorrect. Under these set of facts, the AO appears to have been satisfied with the explanations given by the assessee and did not make any addition. We have noticed that the Hon’ble Supreme Court has held in the case of Central Bureau of Investigation (supra) that the entries in the books of account by themselves are not sufficient to charge any person with liability. Hence, in our view, it cannot be held that the assessing officer did not carry out enquiry or verification which should have been done, since the facts and circumstances of the case and the incriminating document was not considered to be strong by the AO to implicate the assessee. Thus, we are of the view that the assessing officer has taken a plausible view in the facts and circumstances of the case. Even though the Ld Pr. CIT has drawn certain adverse inferences from the document, yet it can seen that they are debatable in nature. Further, as noticed earlier, the Ld Pr. CIT has not brought any material on record by making enquiries or verifications to substantiate his inferences. He has also not shown that the view taken by him is not sustainable in law. Thus, we are of the view that the Ld Pr. CIT has passed the impugned revision orders only to carry out fishing and roving enquiries with the objective of substituting his views with that of the AO. Hence we are of the view that the Ld Pr. CIT was not justified was not correct in law in holding that the impugned assessment orders were erroneous.” Unquote.

11. The Hon‟ble High Court of Madras in the case of Arul Industries v. Asst. Commissioner of Income-tax, Central Circle II [2025] 177 taxmann.com 607 (Madras) has held as under :

Quote, “16. Therefore, on facts, it cannot be said to be a case where opinion was formed without any inquiry and without any material. Consequently, it could not be classified as a case of “lack of inquiry” but at the most even if the case of the Revenue is accepted on the basis of the order passed by the Commissioner, this was a case of “inadequate inquiry”. Once there is an inquiry, even inadequate, that would not by itself, give occasion to the Commissioner to pass order under Section 263 of the Act merely because he has a different opinion in the matter. It cannot, therefore, be said to be a case of erroneous order and prejudicial to the interest of the Revenue.

17. A Division Bench of Delhi High Court in the case of Sunbeam Auto Ltd. (cited supra) examined the aforesaid legal position as regards the scope and ambit of power under Section 263 of the Act. It was held to be a settled principle that the Assessing Officer in the assessment order is not required to give detailed reason in respect of each and every item of deduction etc. One has to see from the records as to whether there was any application of mind. Distinction between “lack of inquiry” and “inadequate inquiry” was also highlighted in the said decision. It was held that if there was any inquiry, even inadequate, that would not by itself, give occasion to the Commissioner to pass orders under Section 263 of the Act, merely because he has different opinion in the matter and it is only in cases of “lack of inquiry” that such a course of action would be open.

18. Similar view was taken by the Bombay High Court in the case of Gabriel India Ltd. [supra]. Based on logical and rational reading of the provisions contained in Sub-section (1) of Section 263 of the Act, it was observed that suo motu revision can be exercised by the Commissioner only if, on examination of the records of any proceedings under the Act, it is found that any order passed therein by the Income Tax Officer is ‘erroneous insofar as it is prejudicial to the interests of the Revenue’. It is not an arbitrary or unchartered power, and can be exercised only on fulfilment of the requirements laid down in Sub-section (1) of Section 263 of the Act. The consideration of the Commissioner as to whether an order is erroneous insofar as it is prejudicial to the interests of the Revenue, must be based on the materials on the record of the proceedings called for by him. If there are no materials on record on the basis of which it can be said that the Commissioner, acting in a reasonable manner, could have come to such a conclusion, the very initiation of proceedings by him will be illegal and without jurisdiction. The Commissioner cannot initiate proceedings with a view to starting fishing and roving enquiries in the matters or orders which are already concluded. Such action will be against the well-accepted policy of law that there must be a point of finality in all legal proceedings, that stale issues should not be reactivated beyond a particular stage and that lapse of time must induce, repose in and set at rest judicial and quasi-judicial controversies as it must in other spheres of human activity.

19. Therefore, an order cannot be termed as erroneous unless it is not in accordance with law. If the Income Tax Officer, acting in accordance with law, makes certain assessment, the same cannot be branded as erroneous by the Commissioner, simply because, according to the Commissioner, the order should have been written more elaborately. The Section does not visualize a case of substitution of the judgment of the Commissioner or that of the Income Tax Officer, who passed the order, unless the decision is held to be erroneous. There must be some prima facie material on record to show that the tax which was lawfully eligible has not been imposed or that by wrong application of the relevant statute on an incorrect or incomplete interpretation, a lesser tax than what was just has been imposed.

20. On facts of the present case, it cannot be said to be a case of violation of any provision of law but appears to be more a case of alleged inadequate inquiry rather than lack of inquiry or material, warranting inference with the order that was drawn by the Assessing Officer in the assessment proceedings, pursuant to notice under Section 153C of the Act.

21. Accordingly, the first question of law is answered in favour of the assessee and against the Revenue.”

12. In these facts and circumstances of the case for all the reasons discussed above, since the AO has taken a plausible view based on the submission of the assessee and the Ld.CIT(IT85TP) has not pointed out any fault in the submission of the Assessee, Ld.CIT(IT85TP) has not commented that the assessee do not fulfill any particular condition of eligibility u/s 80JJAA and 10AA of the Act, respectfully following the proposition of law laid down by Hon’ble Supreme Court, Hon’ble High Court and ITAT Mumbai Bench, for all the reasons discussed in earlier paragraphs, we are of the considered opinion that the Order u/s 263 cannot be sustained, accordingly the Order u/s 263 is quashed.

13. In the result, the appeal of the assessee is allowed.

Order pronounced in the open Court on 25thJune, 2026