Read more at: https://taxguru.in/income-tax/pune-itat-rs-10-lakh-addition-deleted-weak-cash-payment-evidence.html?utm_source=follow.it

Copyright © Taxguru.in

Ashutosh Pandurang Patil Vs ITO (ITAT Pune)

Pune ITAT Deletes ₹10 Lakh Addition for Alleged Cash Payment on Flat Purchase – Truncated Seized Document & Uncorroborated Statement Have No Evidentiary Value

The Pune ITAT deleted the addition of ₹10 lakh made on account of an alleged cash payment for the purchase of a flat, holding that the Revenue had failed to establish that any cash consideration had actually passed from the assessee to the builder. The assessee consistently denied making any cash payment and produced the registered sale agreement, housing loan sanction letter, bank statements, payment receipts and a chart of payments, demonstrating that the entire consideration was paid through banking channels. The Tribunal found that the Assessing Officer had relied only on a truncated copy of a seized loose paper, without furnishing the complete document to the assessee or establishing that it related to the Sai Vista project or evidenced any cash payment by the assessee.

The Tribunal further held that the statement of the builder’s representative, Mr. Kanhaiyalal Matani, was of no evidentiary value, as it did not specifically allege receipt of cash from the assessee, the complete statement was not supplied, and no opportunity for cross-examination was provided. Once the assessee had rebutted the allegation with documentary evidence, the burden shifted to the Revenue, which failed to produce any cogent material proving the alleged on-money payment. Relying on the Rajasthan High Court’s decision in CIT v. Bhanwarlal Murwatiya, the Tribunal held that mere suspicion or uncorroborated documents cannot justify an addition unless actual payment is proved, and accordingly directed the Assessing Officer to delete the addition of ₹10 lakh. The assessee’s appeal was allowed.

FULL TEXT OF THE ORDER OF ITAT PUNE

This is an appeal filed by the Assessee against the order of the Learned Commissioner of Income Tax (Appeals), NFAC, Delhi [Ld.CIT(A)], passed u/s. 250 of the Income Tax Act, 1961 (‘the Act’) for AY2023-24 on27.01.2026, emanating from the Assessment Order u/s 143(3) r.w.s.144B of the Act, dated04.02.2025.

2. Submission of Ld. AR:

Ld. AR submitted statement of facts. The relevant paragraphs of the same are reproduced hereunder:

“1. The assessee, Ashutosh Pandurang Patil, PAN-APBPP0957M, filed his return of income u/s 139(1) of the Income Tax Act, 1961 (here-in-referred to as “the Act”) on 22.07.2023 declaring total income of Rs.23,68,910/- for the A. Y.- 202324.

2. The assessee is an employee of Mahindra and Mahindra Limited and working at their Pune Branch. The assessee has purchased a flat in Pune on 31-03- 2022.

3. The case of the assessee has been selected for compulsory complete scrutiny on the basis of information disseminated after the search report in the case of GK Associate and SSD Group and its related entities.

4. A search and seizure operation were conducted on SSD Group on May 4, 2023. During the search, incriminating documents were found at the residence of Yash Jhan Giyani (an SSD Group employee).

5. The assessee denied making any unaccounted cash payment of Rs. 10,00,000 to SSD Promoters and Builders. He argued that the purchase transaction was carried out as per the registered agreement value, and no additional cash payment was made. The assessee provided his bank statements and financial records to show that he had no such unaccounted cash flow.

6. The response by the assessee was accepted but was held unsatisfied explanation regarding source of payment of Rs. 10,00,000 in cash to the SSD promoters.”

2.1 The Ld. AR vehemently submitted that the assessee had not paid any cash for purchase of flat. The Ld. AR invited our attention to the Registered Sale Agreement for Flat No. E-503 which is at page No. 75 of the paper book, Housing Loan Sanction Letter at page No. 76 of the paper book, Payment details at page No. 91 of the paper book and Bank statements is at page No. 92 of the paper book. The Ld. AR submitted that all the payments have been made through banking channel. The Ld. AR also submitted that in the statement recorded of Mr. Kanhaiyalal Matani that he has not said that the assessee had made any payments in cash. Mr. Kanhaiyalal Matani’s statement has been recorded by the Assessing Officer which is general in nature. The Ld. AR also submitted that no opportunity of cross-examination was provided. The Ld. AR submitted that the documents relied by the Assessing Officer is dumb documents.

3. Submission of Ld. DR:

The Ld. DR relied on the order of the AO and Ld. CIT(A).

4. Findings and analysis:

We have heard both the parties and perused the records. In this case, admittedly, the assessee had filed return of income u/s 139(1) of the Act for AY 2023-24 declaring total income at Rs.23,68,910/-. The assessee’s case was selected for scrutiny based on information received from Investigation Wing by the Assessing Officer. The assessee was asked to explain regarding alleged cash payments made by the assessee for purchase of Flat E-503 in Sai Vista. The assessee categorically denied any cash payments made to the builder. Assessee submitted that the entire payments have been made through banking channel as per the terms of the agreement. During assessment assessee filed following documents :

i. Copy of ICICI Bank statement

ii. Copy of State Bank of India loan statement

iii. Copy of receipts issued by the Sai Vista

iv. Chart showing sources of money paid for the flat.

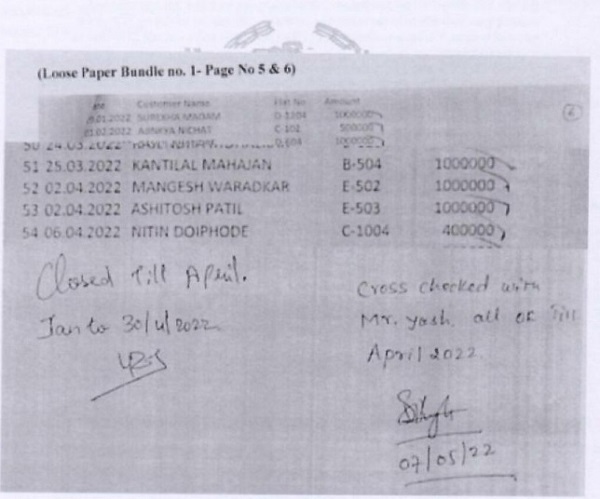

4.1 In the assessment order, Assessing Officer has referred to some loose papers Bundle No. 1 page Nos. 5 and 6 which has been scanned by the AO in the assessment order at page No. 10 of the assessment order. The same scanned is reproduced here as under :

4.2 First and foremost thing the said scanned copy which appears on page No. 10 of the assessment order is not the complete page which was allegedly found during the search. The AO had never provided the complete set of seized papers to the assessee. Revenue has not produced copy of the entire page of the impugned seized documents referred by the AO in the assessment order at page No. 10. The scanned copy appearing in the assessment order is a truncated copy of some papers. From the scanned copy it cannot be understood that it was found during search and documents pertains to some transactions related to Sai Vista project. Therefore, the entire addition made by AO is based on some documents which does not specify that it pertains to Sai Vista project. Be it as it may be, on perusal of the said truncated documents it is not evident that cash payment was made by the assessee to builder.

4.3 The AO has reproduced Q. No. 9 and its answer and Q. No. 10 of statement of Mr. Kanhaiyalal Matani. Again, no opportunity of cross-examination was provided to the assessee. Also, complete set of statement was not provided to the assessee. After reading the answer to Q. No. 9 of Mr. Kanhaiyalal Matani, nowhere, Mr. Kanhaiyalal Matani has alleged receipts of cash from assessee Ashutosh Patil. Therefore, the statement reproduced is of no evidentiary value to establish cash payment by Ashutosh Patil.

4.4 In these facts and circumstances of the case, Revenue has miserably failed to prove cash payments by Ashutosh Patil for purchase of flat. Once, assessee has denied the allegation, submitted relevant bank statements to prove payments through banking channel, onus shifted to ITO. In this case, the ITO has miserably failed to prove cash payments by assessee. The ITO has relied on the documents which do not prove any cash payments.

4.5 The Revenue’s appeal was dismissed by the Hon’ble Rajasthan High Court in the case of CIT Vs. Bhanwarlal Murwatiya, [2008] 215 CTR 489 (RAJ.)as under :

Quote, “7. We have considered the submissions, and after going through the impugned orders, are of the view that all said and done, the question as to what was the price of the land at the relevant time, is a pure question of fact. Apart from the fact, that even if, it were to be assumed, that the price of the land was different than the one, recited in the sale deed, unless it is established on record by the department, that as a matter of fact, the consideration, as alleged by the department, did pass to. the seller from the purchaser, it cannot be said, that the department had any right to make any additions. It is a different story as to, to what extent and how, the statement of Suresh Kumar Soni, as given before different authorities, at different times, can be used against the assessee. More so, when none of the witnesses were examined before the assessing officer, and the assessee did not have any opportunity to cross examine them.

8. In any case, the question as to whether the consideration of Rs.61 lakhs, or any other higher consideration than the one, mentioned in the sale deed, did pass from the assessee to the seller or not, does nonetheless remain a question of fact, and it is not shown by the department, that any relevant material has been ignored, or misread by the learned Commissioner, or the learned Tribunal.

9. In that view of the matter, in our view, the questions, as framed, cannot be even said to be arising, and in any case, are required to be answered against the revenue , and in favour of the assessee.

10. Accordingly, the questions are answered as above, and the appeals are dismissed.”

5. In these facts and circumstances of the case for all the reasons discussed above, we do not find any merit in the addition of Rs.10,00,000/- made in the assessment order, accordingly, AO is directed to delete the addition.

6. In the result, the appeal of the assessee is allowed.

Order pronounced in the open Court on 24thJune, 2026