Synopsis

For years, a mid-cap company told shareholders it was one of the world’s largest players in its line of business by revenue. The claim was not small. Its reported turnover ran into lakhs of crores, making it look bigger than many of India’s well-known listed companies. Then one shareholder asked a basic question: Why was so much money owed to the company not coming in? That email sparked a SEBI investigation, which, beyond delayed receivables, struggled to find the real business behind the reported numbers. This is the story of how a company can appear enormous in its annual reports, while the transactions behind that size remain difficult to trace. It is also a story of warning signs that were not hidden. They were sitting inside the company’s own disclosures, year after year.

For years, Rajesh Exports reported the revenue of a corporate giant. The market regulator now says the audited operating numbers never supported it.

SEBI’s case turns on a simple distinction: Handling gold is not the same as owning it. In the regulator’s telling, banks and bullion dealers sent gold to Valcambi, the Swiss refinery in the Rajesh Exports Group, to be melted, purified, and stamped into fresh bars. For that work, the refinery earned a fee.

But year after year, SEBI says, the full value of the gold that passed through the refining chain surfaced in the consolidated accounts of a company as sales, until those sales added up to roughly Rs. 15 lakh crore over five years, a figure large enough to rank it among the biggest companies in the country.

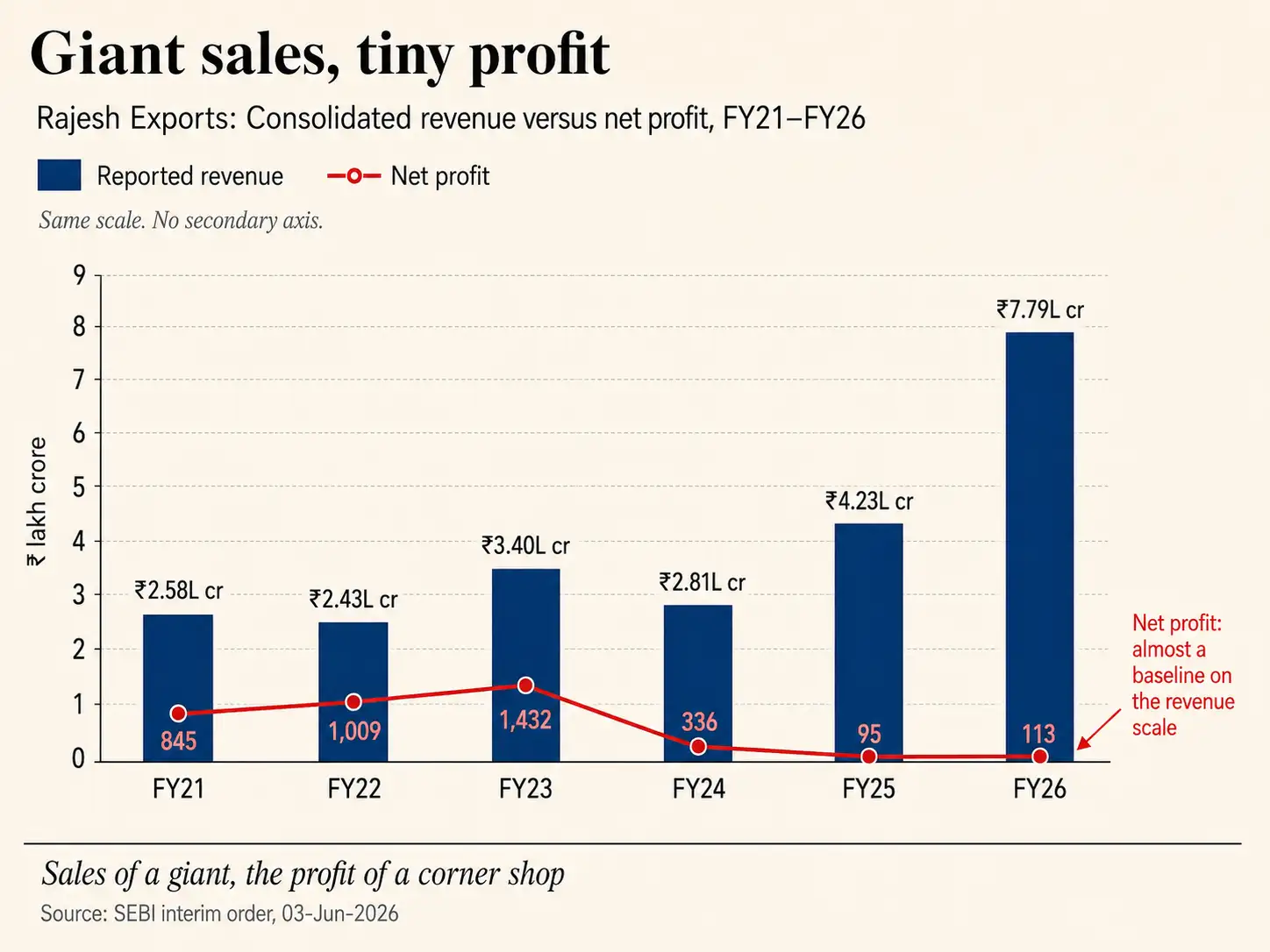

It made for a strange kind of giant. Here was a company whose sales rivalled the largest names in India, yet whose profit was so slight that in some years it kept only about two paise out of every hundred rupees of revenue.

Top Line Colossus, Bottom Line Minnow

A business can run on thin margins but a near-invisible profit on a mountain of turnover invites one plain question, the question that runs through this whole affair: Could the mountain be verified?

That is what makes the SEBI order serious. Yes, it is still an interim order. Rajesh Exports still has time to place its defence, respond to SEBI’s findings and support its stance that there was no wrongdoing. But this is not a case where a regulator raised an alarm after a quick look at one disclosure.

A shareholder complaint came in March 2024. SEBI appointed an investigating authority in October 2024. BDO India Services Pvt Ltd was brought in as the forensic auditor in December 2024. Its forensic audit report came only in March 2026. By then, the regulator and the forensic auditor had spent well over a year trying to test the company’s numbers.

If the business behind the lakhs of crores of reported revenue was clean, clear, and fully traceable, the company had the most direct way to answer the regulator: Produce the records. Customer-wise sales, vendor-wise purchases, invoices, books of account, ERP data, journal entries, and subsidiary financials should have settled the central question.

Instead, SEBI says it was met with incomplete submissions, missing primary records, limited access, and explanations that did not bridge the gap between the scale shown in the annual reports and the evidence available for verification.

That is why “prima facie” should not be viewed lightly. It only means SEBI has not passed its final finding yet. But on the record available so far, the regulator has found enough to treat the matter as serious.

Its case is that Rajesh Exports presented a scale to the market that was largely unsupported by audited operating numbers and primary documents. The order names both the company and its promoter and Executive Chairman, Rajesh Mehta.

The allegation is not about a small accounting error. It goes to the heart of what shareholders were told the company was. SEBI says almost the entire consolidated scale came from overseas entities, yet the records and subsidiary-level disclosures needed to verify that scale were either unavailable, incomplete, or not provided.

In simple terms, the company looked enormous on paper. But when the regulator asked for the paper trail behind that size, SEBI says the trail did not hold up.

What follows is the regulator’s case, and the company’s reply. But the starting point is clear: This is not a routine disclosure issue. It is a case where SEBI is questioning whether one of India’s companies had shown the market a business far larger than what could be independently verified.

Follow the Company’s Shape

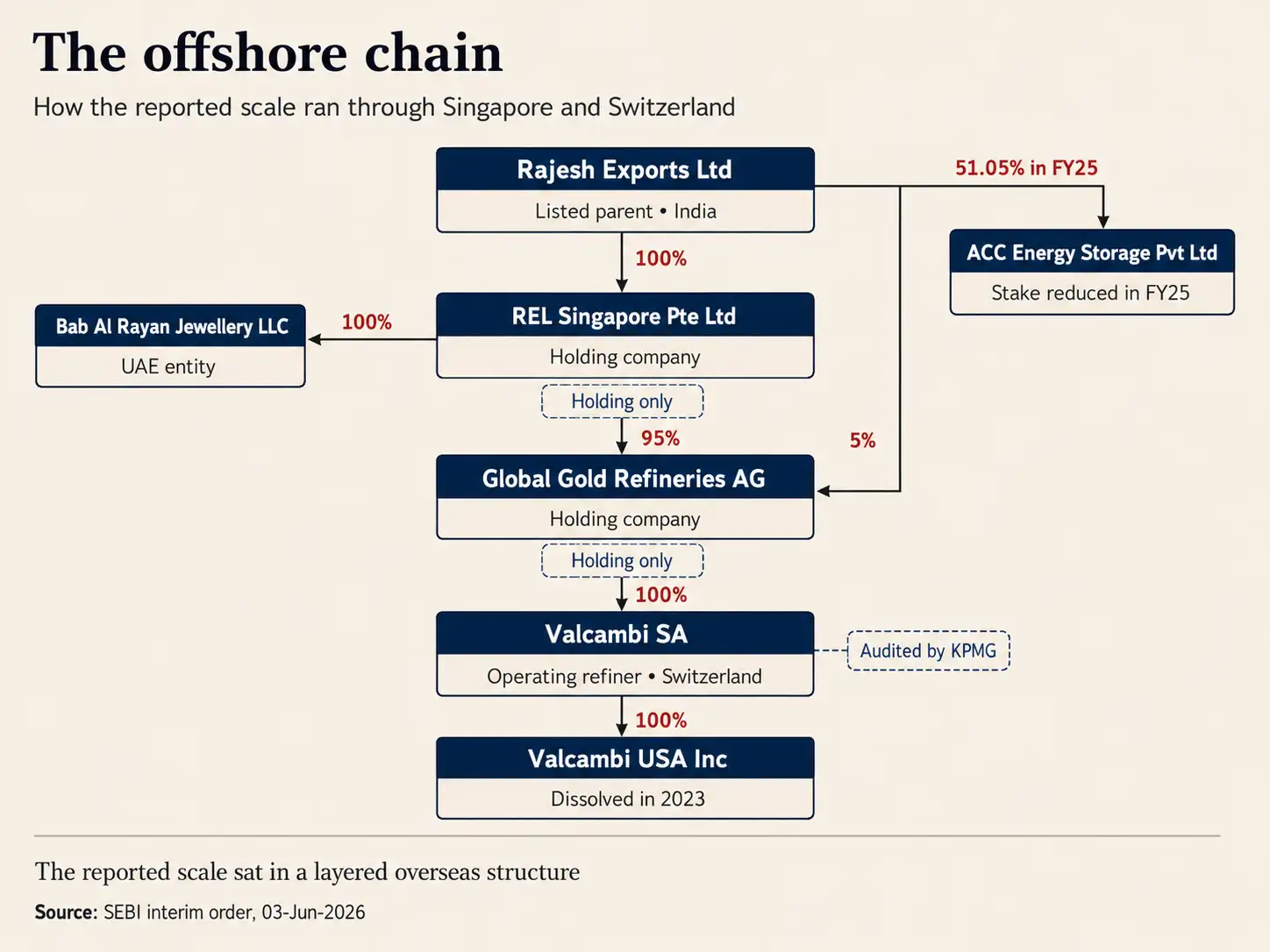

To understand the allegation, you first have to see how Rajesh Exports is built, because the shape is the story. The listed company you can buy on the BSE and NSE is the Indian parent, a gold refiner and jeweller that runs the Shubh Jewellers chain.

But that Indian business is at the small end. Above the rest of the group sits a chain of companies in other countries. The Indian parent owns a holding company in Singapore. That Singapore company sits above a Swiss holding company, Global Gold Refineries or GGR for short. GGR owns Valcambi, a Swiss firm which Rajesh Exports bought in 2015.

Two details matter for later. First, by the group’s own account, the Singapore company and GGR are holding companies as they own other companies but do no day-to-day business themselves. Only Valcambi, at the very end of the chain, actually refines gold.

Second, the ownership is deliberately layered: GGR is held 95% through Singapore and 5% directly by the Indian parent, and below Valcambi sits Valcambi USA that was dissolved in 2023.

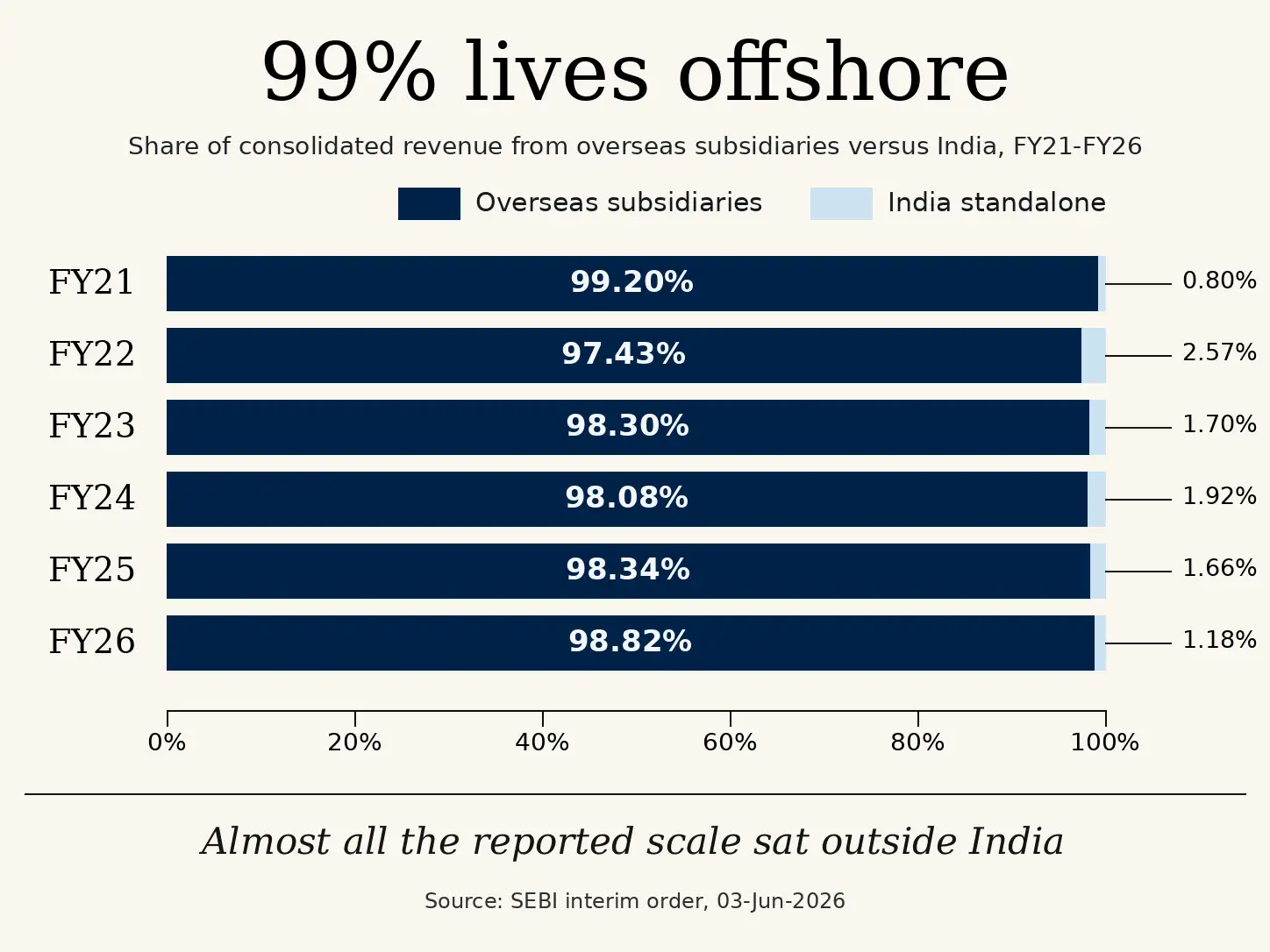

Now the first hard fact. Almost none of the group’s revenue comes from the Indian company you can actually invest in. By SEBI’s reckoning, between 97% and 99% of the consolidated revenue every year came from the overseas subsidiaries, not from India.

To put numbers on it: The Indian standalone business reported sales of roughly Rs. 2,000 crore to Rs. 7,000 crore a year over the five years, while the consolidated group reported between Rs. 2.4 lakh crore and Rs. 4.2 lakh crore.

The giant lives almost entirely overseas, in the part of the group hardest for an Indian investor, auditor, or regulator to see.

The Tailor’s Fee

Here is the crux, and it turns on a distinction that sounds technical but is really common sense. A refinery like Valcambi works the way a tailor works when you bring him your own cloth. Banks and bullion dealers send Valcambi their gold; it melts, purifies, and re-stamps the metal and sends it back; and it charges for the work.

SEBI’s reading is that Valcambi’s audited standalone accounts treated this activity as processing or value-addition revenue, not as the sale of the entire gold value.

By that audited operating-company measure, Valcambi was a real but modest business: Its revenue ran to only a few hundred crore a year, between about Rs. 430 crore and Rs. 740 crore.

This is the point on which the whole case rests. If you count only the processing fee, Valcambi is a mid-sized company. If you count the entire market value of all the gold passing through its furnaces, gold that SEBI says belonged to customers, the same activity becomes a figure in the lakhs of crores.

SEBI’s allegation is that the group did the second thing: It reported the gross value of third-party gold as group revenue.

Number With No Home

And here is the oddity that troubles the regulator most. That giant figure does not sit in Valcambi’s audited standalone books. It sits one rung above, in GGR, which, on the group’s own description, did no day-to-day business of its own. SEBI says a company described as non-operating was carrying more revenue than the working refinery beneath it.

The two sets of accounts were also checked very differently. Valcambi’s standalone accounts were audited by KPMG. GGR’s consolidated accounts were prepared under what the group called a “group accounting manual”, and KPMG specifically clarified that its work on those GGR figures was not a statutory audit.

So the smaller audited operating number sat at the refinery, while the much larger unaudited consolidated number sat one level above. And it is the larger number that was carried up into Rajesh Exports’ consolidated accounts and shown to investors.

Look at one year to feel the size of the gap. In 2023, Valcambi’s audited revenue was about Rs. 543 crore. The unaudited GGR accounts for the same period showed revenue of about Rs. 2.93 lakh crore, more than five hundred times larger, and Rajesh Exports’ consolidated revenue came to about Rs. 2.81 lakh crore.

The operating company that did the actual refining recorded a few hundred crore; the holding company above it, which by its own account did nothing, recorded the better part of Rs. 3 lakh crore. SEBI calls this treatment internally inconsistent, commercially implausible, and unsupported by any primary records.

That single gap, audited and small at the bottom, unaudited and vast one level up, is the entire case in miniature. Strip everything else away and SEBI’s reading comes to this: The revenue that made Rajesh Exports look like a giant was not supported by the audited numbers of the operating refinery.

The Other SEBI Redflags

The overseas revenue is the heart of the case, but SEBI says there were other accounting red flags in the Indian accounts as well.

Foreign exchange swings and interest, dressed as sales: Gains made when the rupee moved against foreign currencies – more than Rs. 860 crore over four years – were counted inside “revenue from operations”, as was around Rs. 200 crore of interest earned on bank deposits and mutual funds.

SEBI says these were not operating sales and should have been shown separately; the company’s own stated policy also placed interest under “other income”. Reported inside revenue, such items made the operating business look busier than it otherwise would have.

The investment that appeared from nowhere: Then there is an asset that SEBI says was not adequately explained in the audited accounts. When a stock exchange asked Rajesh Exports about an investment of roughly Rs. 1,035 crore sitting in its accounts, the company said it represented an “investment in gold mines in Africa”.

But, according to SEBI, that phrase appears nowhere in the company’s audited financial statements across the relevant years. The money sat as an unlabelled “other investment”, with no public detail on what it was, where it was, or what it was worth.

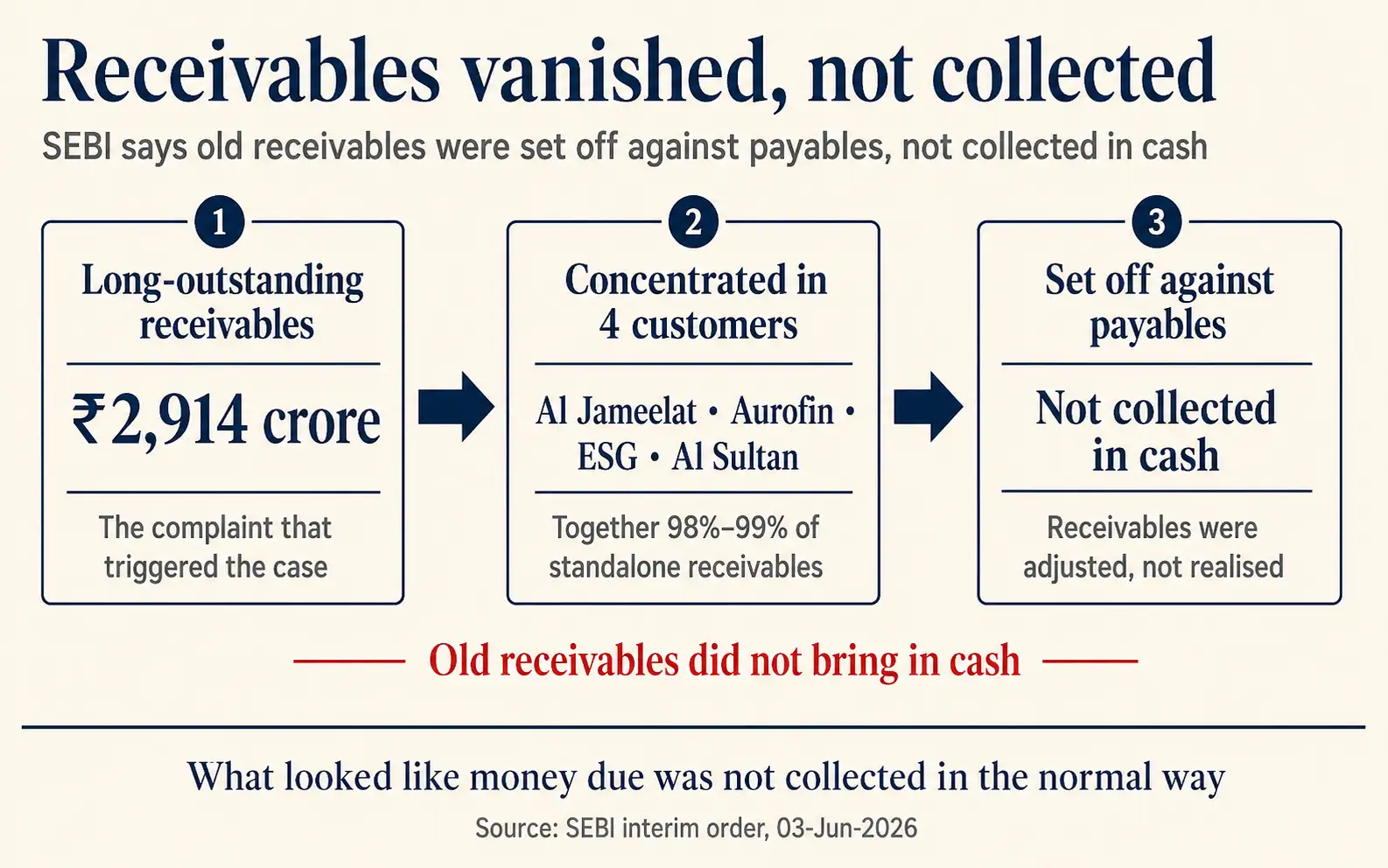

The receivables that quietly disappeared: The complaint that started it all concerned old receivables. The SEBI order finds that about Rs. 2,914 crore of long-outstanding receivables, concentrated in four overseas customers (Al Jameelat, Aurofin, ESG, and Al Sultan, together 98-99% of standalone receivables), were not collected in cash but netted off against payables.

SEBI reports that some of these counterparties could not be traced, one email address bounced as not configured to receive mail, one entity’s license actually belonged to a differently named company, and confirmation letters were obtained only after scrutiny began. It found these set-offs were made without enforceable rights of set-off and without disclosure, contrary to accounting standards.

The promoter’s personal trades, booked as company sales: On the standalone India books, the order describes a different mechanism. Rajesh Exports recorded sales of about Rs. 11,487 crore and purchases of about Rs. 11,488 crore over FY22 to FY24 with an entity called Affluence Shares and Stocks Pvt Ltd. Those near-identical figures meant almost no profit on transactions running into thousands of crores.

SEBI found that Affluence, a registered stockbroker, denied ever being Rajesh Exports’ client. The order says Affluence’s actual relationship was with Mr. Rajesh Mehta personally, who traded gold derivatives through it on 102 days, putting in Rs 7.45 crore of margin and making a net loss of about Rs. 3.50 crore.

SEBI’s finding is that the company took its promoter’s personal derivative trades and recorded them as its own large-scale sales and purchases, inflating standalone turnover by about Rs. 11,487 crore.

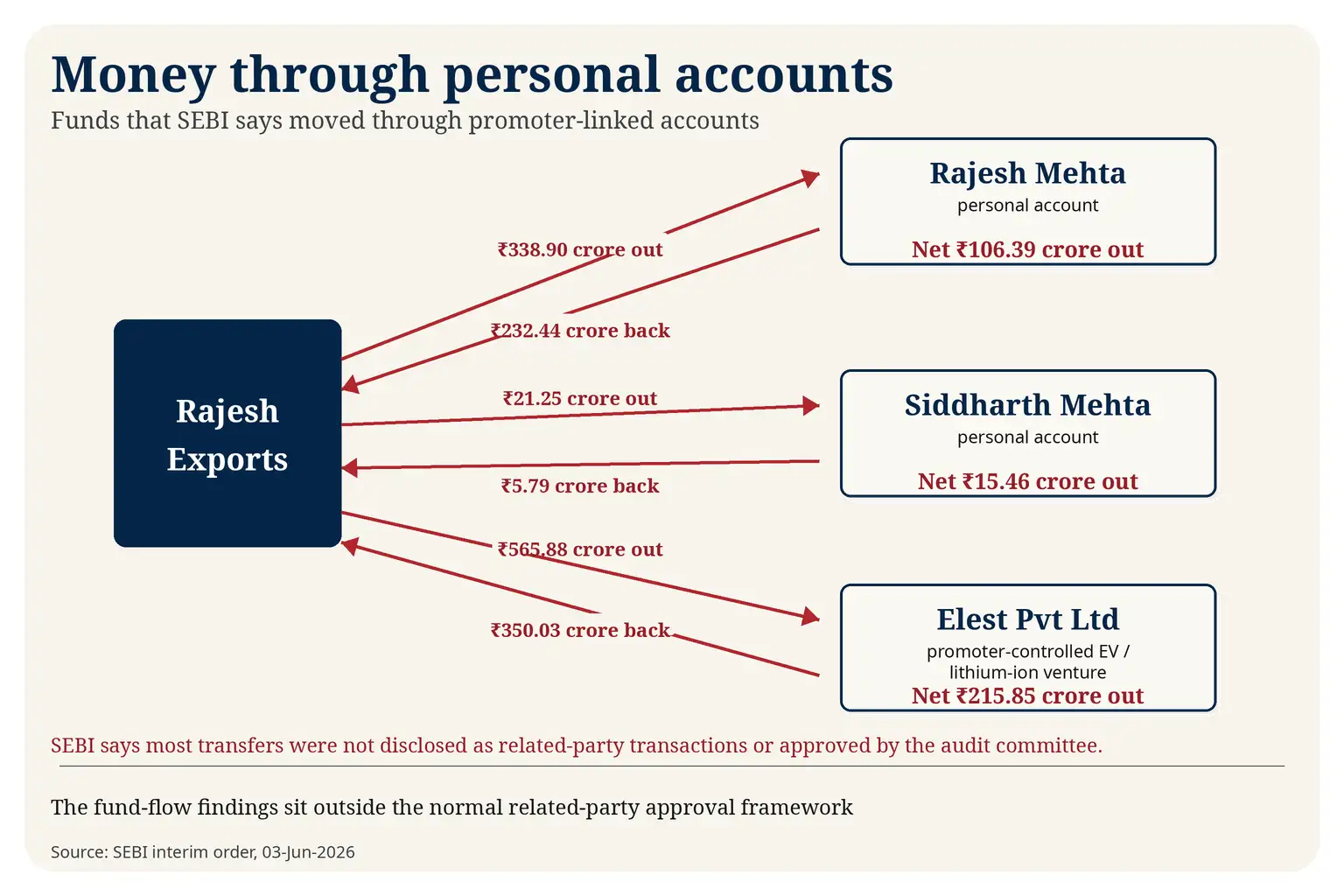

Company money through personal accounts: Finally, the order describes funds moving through the personal bank accounts of Mr. Rajesh Mehta (Rs. 338.90 crore out, Rs. 232.44 crore back over five years) and his son Siddharth Mehta (Rs. 21.25 crore out), plus net transfers of about Rs. 215.85 crore to Elest Pvt Ltd, a promoter-controlled lithium-ion and EV venture.

The order says the company admitted routing funds through the promoter’s account “without revealing the bank account from which the funds had come”, which SEBI reads as deliberate obfuscation. Most of these transfers were not disclosed as related-party transactions or approved by the audit committee.

A balance sheet that did not eliminate itself: On consolidation, the order says, intra-group items that should have been cancelled out were left in, inflating the balance sheet, including about Rs. 2,501 crore of intra-group investments and about Rs. 1,457 crore of intra-group payables to Valcambi as of March 2025.

Why No One Could Simply Check

At this point a fair reader will ask the obvious question: If the gold really did flow through Valcambi, why couldn’t the company just prove the revenue and end the argument?

SEBI’s answer is that it asked, repeatedly, and the records were not provided in full. It sought the ordinary evidence any large business keeps – customer-by-customer sales, vendor-by-vendor purchases, invoices, confirmations, and the subsidiaries’ own financial statements.

Much of it was not produced, or arrived only in part. The forensic auditor the regulator appointed could fully support barely 2% of the purchases it tried to test, and only about a third of the sales. When pressed on the overseas data, the company cited a Swiss data-protection law; but SEBI points out that the law protects individuals, not the financial data of companies, and in any case allows disclosure to a regulator.

It is worth being precise about what the regulator is and is not claiming, because the distinction is the fair one.

The company points to Valcambi’s real global refining business; SEBI’s case is narrower. It says the scale shown to Indian investors depended on counting the gross value of customer gold, while the audited operating company treated the same activity as processing or value-addition revenue – and Rajesh Exports did not produce the records that could support the much larger presentation.

The Company’s Answer

Two days after the SEBI order, Rajesh Mehta wrote to the exchanges to push back. Rajesh Exports, he said, is debt-free, has never raised public money beyond a Rs. 10 crore share sale in 1995, and has never mis-reported anything; the huge revenues, he argued, come “primarily from Valcambi”, the world-renowned refinery; and the order is only interim, raising suspicions rather than reaching conclusions, which the company is confident it can answer with documents and evidence.

The reputation of Valcambi is real, and the debt-free point is a fair one.

SEBI’s problem with that defence is the same gap that runs through the order. If the revenue is “primarily from Valcambi”, the regulator asks why Valcambi’s audited standalone accounts show only a few hundred crore a year, while the lakhs of crores sit one level up, in a holding company described as non-operating and whose consolidated figures were not statutorily audited.

But again, the bigger question: If the company is confident of answering the allegations with documents and evidence, why hasn’t it been able to do so till now?

What the Fresh Audit Has to Settle

For now the SEBI order does a handful of concrete things. Rajesh Mehta is barred from buying or selling his own company’s shares until further notice. The company has 30 days to hand over the records it has so far withheld, and a fresh forensic auditor will be appointed to redo the work the first one could not finish.

The matter has been referred to the audit watchdog, the National Financial Reporting Authority, to examine the conduct of the company’s auditors. The shares have not been suspended, and for the moment only the promoter, not the other directors, has been restrained.

The questions the new audit must answer are now specific. Who, exactly, are the customers and suppliers behind lakhs of crores of overseas sales? On what basis did a non-operating holding company come to record the gross value of gold as its revenue when the operating refiner recorded only a fee?

And why do the subsidiaries’ own financial statements – the documents that would put the matter beyond doubt one way or the other – remain largely unproduced?

Until those are answered, the central figure stays exactly what the headline calls it.

Question That Remains

Strip it all down and the story rests on a single distinction: The difference between handling gold and owning it.

A refinery that touches a river of gold is not necessarily a company that sells one – and the regulator’s case is that, for years, Rajesh Exports reported the second when the audited operating-company numbers showed only the first.

None of it is proven yet. The order is interim, the company is contesting it, and a fresh audit has been ordered precisely because the first was left with too little to examine. But the question mark over that Rs. 15 lakh crore is now on the record.

Disclaimer: The views, scores, research and investment tips expressed herein are not that of Economic Times (“ET”) or its management and have been gathered from various third-party sources. ET does not guarantee the accuracy, adequacy or completeness of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. The content provided herein including any output of tools/analysis is for informational purposes only and should not be relied upon or construed as an investment advice. ET advises users to check with a certified professional before making any investment decision.