Listen to this article in summarized format

For many salaried employees, the appraisal season was not a regular affair this year. Some organisations rolled out increments effective 1 April and aligned the salary structures with the new labour codes. Some also decided to incorporate taxexempt allowances such as meal coupons, children’s education and hostel expenses, whose limits were hiked under the new Income Tax rules, among others, to optimise employees’ tax outgo.

Income Tax Guide

Income Tax Union Budget FY 2026-27 LiveIncome Tax Slabs FY 2025-26Income Tax Calculator 2025

Preparing for the changes

To be sure, many organisations are yet to implement the norms, even though they are actively reviewing and testing structures. “While the April-May appraisal cycle has prompted many companies to review compensation structures, a broadbased labour code-compliant rollout across India Inc. is still not evident,” says Shailesh Khanna, Business Lead, ManpowerGroup India. Larger and more structured employers are using this cycle to assess impact, test revised salary breakups and prepare payroll systems. “Many others remain cautious, preferring to align changes with clearer implementation timelines, state-level readiness and market practice,” he says.

Now that the labour ministry has also notified the final central labour code rules, the process is likely to gain momentum. “While several organisations have evaluated their structure with the wage definition under the codes and realigned the same as part of the annual appraisal cycle, others are still in the process. However, given that the final central rules have been notified in May, there is a growing sense of urgency,” says Radhika Viswanathan, Executive Director, Deloitte India.

Central rules are applicable to establishments in specific sectors. “For example, railways, air transport, telecommunication, banking, oil fields, ports, etc. In other instances, the state government is the appropriate authority, and hence the state rules need to be operationalised for on-ground implementation,” she adds. The process is likely to be staggered and depend on the organisations’ policies.

“Some organisations have rolled out increments along with labour codes’ compliant compensation structure in April. Many others are likely to announce hikes only in May and June,” says Balasubramanian A., Senior Vice-President, Teamlease Services. By combining appraisals with labour codelinked implementation, organisations are mitigating the impact of reduced take-home pay due to the increased statutory social security obligations. “There is still some degree of fluidity, there is no 100% certainty yet, though the broad direction is becoming clearer,” he says.

According to him, the adoption is currently more visible among large enterprises and compliance-intensive sectors, while smaller firms are adopting a more wait-andwatch approach due to concerns around cost impact and take-home pay adjustments.

Labour code impact decoded

Salaried individuals who have received their appraisal letters now have the onerous task of decoding their revised compensation structures and evaluating the newly-introduced tax exemptions, effective 1 April.

The immediate takeaway for employees is that a salary hike this appraisal season may not necessarily translate into a proportionate increase in take-home pay. This is because the revised wage definition under the labour codes requires at least 50% of total remuneration to be treated as wages for the calculation of social security obligations, including gratuity and Employees’ State Insurance (ESI).

“For example, if someone earning a Rs.100 CTC (cost to company) receives an 8% increment, they may expect take-home pay to rise by Rs.8. However, if their employees’ provident fund (EPF) wages (basic salary component, primarily) were below Rs.50 to begin with, or they come under the ambit of ESI (employee state insurance) for the first time, then, it is possible that out of the Rs.8 increment, a part of it, say Rs.3, could go towards meeting the additional statutory obligations, leaving an actual increase in take-home salary of only around Rs.5,” says Subramanian. Employees whose basic salaries are below Rs.15,000 will likely see a dip in their take-home salaries as gratuity and EPF components rise. Gratuity is now linked to 50% of the total remuneration, unlike earlier when it was pegged to the basic pay, which was typically 30-40% of the CTC. It is bound to go up across salary levels and organisations.

Employees also need to keep an eye on the impact on the EPF contribution. “The basic salary is predominantly retained at the same levels in the realigned structure and hence there is no impact on the EPF contribution for those with the monthly basic salary of over Rs.15,000,” says Vishwanathan.

Balasubramian of Teamlease says a broad pattern is emerging, with companies gradually moving towards a higher basic pay component as a proportion of total compensation, in line with the labour codelinked wage definitions. “This shift is not limited to employees earning below the Rs.15,000 EPF threshold; in many organisedsector roles, basic pay revisions are being applied more uniformly across grades to maintain internal parity and simplify payroll structures,” he says. As a result, EPF contributions have increased in several cases, particularly for employees where EPF is calculated on actual basic wages rather than being capped. “While this strengthens long-term retirement savings and social security coverage, it can also reduce immediate take-home pay, which is why some firms are adopting phased adjustments rather than abrupt restructuring,” he adds.

Essentially, for those with basic pay over Rs.15,000, the impact on in-hand pay will, therefore, depend on the employers’ approach. “(For such employees), the salarystructure changes have usually had limited direct impact on monthly take-home, unless the company also changed its EPF contribution policy. In many companies, EPF for higher-salaried employees was already being capped rather than calculated on the full basic,” says Khanna. For such employees, EPF will not automatically rise even if basic pay moves up as part of salary restructuring. What will change instead is the mix of components, higher basic, lower special/ flexible allowances and higher gratuity provisioning.

“EPF contribution at the rate of 12% is not mandatory if the basic salary is well over the EPF wage ceiling of Rs.15,000 per month. In many cases, provident fund contributions may still remain capped at Rs.1,800, depending on the employee’s choice and employers’ policies. In such cases, take-home will not be impacted by increased EPF contributions,” explains Subramanian.

New tax regime retains the edge over old despite higher exemptions

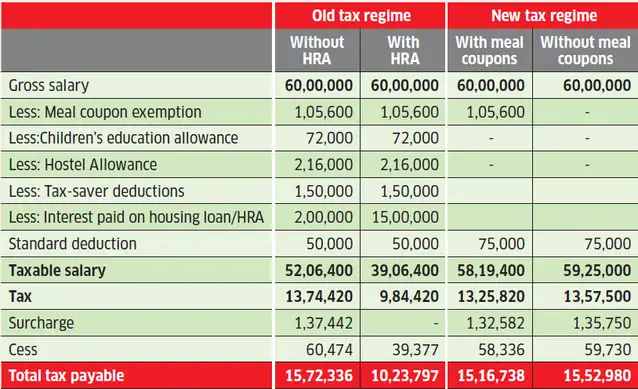

Despite the recently-enhanced children’s education and hostel allowances under the new I-T rules, new tax regime scores unless you claim HRA under the old regime.

Notes and assumptions: 1. Children’s education allowance and hostel allowance are allowed as exemptions only under the old tax regime, as per the new I-T Act rules. 2. Meal coupons @ Rs.200 per meal (44 a month) are allowed under both the regimes. 3. Old tax regime calculations exclude HRA when home loan interest deduction is claimed and vice- versa. 4. Actual HRA claimed is fully tax-exempt; 5. Employers’ contribution to NPS not taken into account 6. All amounts in rupees

Source: ClearTax

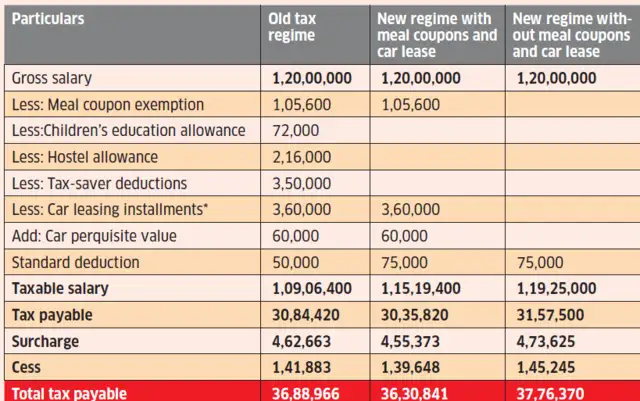

How car lease impacts your tax outgo

Note: Under old regime, tax-saver deductions include tax-saving investments (Rs.1.5 lakh) and home loan interest deduction (Rs.2 lakh); 2. For car leasing, the engine capacity is assumed to be within 1.6L, and no chaffeur provided by the company. Installment per month of Rs.30,000 is deducted from salary; 3. All amounts in Rs..

Source: ClearTax

ALSO READ | 8 ways India’s Labour Codes can help build a modern, expanding, and increasingly diverse workforce

I-T rules 2026: Old tax regime back in focus

Advantage: employees with multiple deductions

- Employees whose companies offer generous flexible benefit components

- Salaried employees living in rented accommodation and claiming HRA

- Parents with two children, both of whom live in hostels

- Higher HRA exemption limit (50%) for employees in Bengaluru, Hyderabad, Pune and Ahmedabad

- Individuals with large deductions (home loan interest + insurance + NPS)

Limited benefit

- High earners without HRA

- Employees with rigid salary structures across the organisation

- Taxpayers who want to avoid extensive paperwork, risk of I-T queries

- Professionals working in companies that offer simplified CTC structures

Take note

- Higher exemption limits will not necessarily translate into significant savings under the old regime

- For high earners, HRA will remain the chief source of meaningful tax savings

- Many taxpayers will continue to benefit from the new regime’s simplicity, lower rates

Deciding factor

Choose old regime if: You claim HRA + multiple deductions

Choose new regime if: You claim limited exemptions, want simplicity and minimal paperwork

Take note of higher exemption limits

Old regime back into focus

This appraisal season has also seen greater use of flexible benefit components after the new income tax rules linked to the Income Tax Act, 2025 came into effect on 1 April.

“For instance, companies are increasingly using meal benefits, education-related allowances, hostel allowances, wellness benefits and reimbursement-based components to maintain tax efficiency and employee retention while remaining within the new wage framework,” says Keyur D. Gandhi, Managing Partner at Gandhi Law Associates.

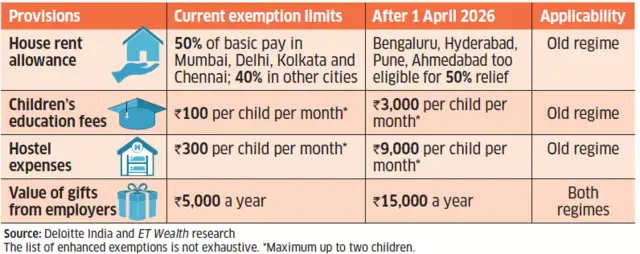

The rules have raised the tax-exemption limits on allowances such as children’s education and hostel expenses (for up to two children) under the old tax regime. Reflecting rising living and education costs, the monthly tax-exempt allowance for children’s education has been increased from Rs.100 to Rs.3,000 per child, while the hostel allowance has been raised from Rs.300 to Rs.9,000 per child. In another key change, salaried individuals in Bengaluru, Pune, Hyderabad and Ahmedabad will now be eligible for House Rent Allowance (HRA) exemption of up to 50% of their basic salary, up from 40%. This brings these cities at par with Delhi, Mumbai, Chennai and Kolkata.

Moreover, meal and refreshment coupon exemption has gone up from Rs.50 to Rs.200 per meal, and this is available under both the regimes from this year. Since Budget 2025, the new income tax regime had emerged as a clear winner with lower tax rates, friendlier tax slabs, and higher exemption and rebate limits. The higher exemption limits on these allowances will now necessitate a reworking of the math and re-evaluation of the tax outgo under the old and new tax regimes.

To be sure, not all organisations will offer these benefits as the exercise will entail increase in cumbersome paperwork for employers as well as employees. Until the new rules were rolled out, only 10-15% of corporates in India offered benefits such as children’s education and hostel allowances. If your employer has decided to incorporate such benefits into your pay packages, however, it’s decision-making time for you.

ClearTax calculations show that for highincome earners, for instance, individuals with gross salaries over Rs.60 lakh, the new regime is likely to have an edge. Even if the taxpayer were to exhaust the Section 80C tax-saver investments of Rs.1.5 lakh (Schedule XV under the new I-T Act), home loan interest (Rs.2 lakh) as well as children’s education and hostel expense allowances, her tax outgo will be higher by nearly Rs.19,000 under the old tax regime. What tilts the scales is essentially house rent allowance (HRA), as the tax payable under the old regime goes down by over Rs.4.93 lakh if she were to pay rent of Rs.15 lakh per annum and claim the exemption.

Under the new tax regime, utilise the meal coupons if your employer offers the same. This can cut your outgo by close to Rs.36,000 (when compared to a scenario where meal benefits are not offered).

Besides these allowances, you also need to take a call on opting for other tax optimisation measures like fuel reimbursement and car lease facilities offered by employers. However, these reimbursement-based benefits are allowed under both the tax regimes. Take note of the new motor car perquisite rules before you put a tax planning strategy in place at the beginning of the financial year. ClearTax calculations show that compared to not availing of such benefits under the new regime, a taxpayer earning Rs.1.2 crore per annum will save close to Rs.1.45 lakh, if she does.

Finally, the decision will also hinge on your willingness to deal with the voluminous paperwork involved in claiming multiple deductions and exemptions. Over the past few years, the income tax department has increased scrutiny of such claims and has been issuing notices seeking documentary proof for the tax benefits availed. If you do choose to avail of the benefits, ensure that you have the necessary documentary proof in place that can be furnished should I-T queries arise.