Clipped from: https://taxguru.in/income-tax/reopening-quashed-itat-slams-casual-148a-action-rs-50l-threshold-met.html?utm_source=follow.it

Nikhil Chandran Vs ITO (ITAT Bangalore)

The Bangalore ITAT quashed the reassessment proceedings against an NRI assessee, holding that the extended limitation under Section 149(1)(b) cannot be invoked unless income escaping assessment exceeds ₹50 lakh.

The case was reopened based on property purchase of ₹57 lakh. However, the assessee had clearly explained that the investment was largely funded through a housing loan (₹42.75 lakh) and the balance from taxed savings. The Tribunal observed that even if the explanation for the balance amount was doubted, the possible unexplained portion was far below ₹50 lakh, making extended reopening invalid.

The ITAT strongly criticized the AO’s approach as casual, non-speaking, and mechanical, noting that:

- The reply and evidences (loan sanction, bank statements, 26AS) were ignored without proper reasoning

- Reopening was based on mere suspicion, leading to a roving and fishing enquiry

- The AO himself was inconsistent—initiating reopening for ₹57 lakh but ultimately making additions of only ~₹6 lakh

It was further held that once, during Section 148A proceedings, it becomes clear that escaped income is below ₹50 lakh, the AO must drop proceedings if normal limitation has expired.

Accordingly, the ITAT:

- Set aside the order u/s 148A(d)

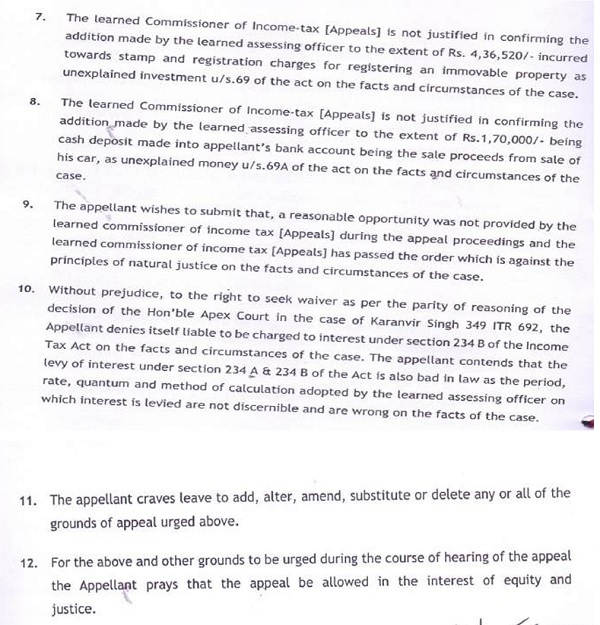

- Quashed notice u/s 148 as time-barred

- Quashed the entire reassessment u/s 147

The appeal of the assessee was allowed in full.

The Bangalore ITAT held that unaccounted cash receipts collected by Al-Badar Educational & Charitable Trust from students for management quota (MD seats) were in the nature of capitation fees, and therefore not eligible for exemption under Sections 11 and 12.

During search, 300 receipts were seized-124 accounted and 176 unaccounted receipts found in the books. Based on seized material and statements recorded under Section 132(4), the AO treated these as capitation fee receipts and taxed them. Though the CIT(A) accepted the existence of unaccounted income, relief was granted on the ground of application for charitable purposes.

The ITAT reversed this, holding that once the nature of receipt itself is non-charitable (capitation fee), exemption fails at the threshold, irrespective of application. The Tribunal emphasized that education must remain charitable and cannot involve profiteering or sale of seats.

Importantly, the ITAT relied on and discussed multiple judicial precedents:

- Delhi High Court in PCIT v. Maharaji Education Trust (2024)– holding that exemption under Section 11 cannot be granted where activities violate the charitable character, especially involving capitation fees.

- Madras High Court in Mac Public Charitable Trust (2022) 450 ITR 368– categorically holding that collection of capitation fee renders the activity non-genuine, disentitling exemption under Sections 11 & 12.

- Supreme Court in T.M.A. Pai Foundation– emphasizing that education is charitable in nature and capitation fee/profiteering is impermissible.

- Supreme Court in P.A. Inamdar– reiterating that capitation fee and commercialization of education are illegal and against public policy.

- Supreme Court in East India Industries (Madras) Pvt. Ltd. v. CIT (1967) 65 ITR 611(with reference to Ibrahim Riza) – holding that if a trust has mixed objects (charitable and non-charitable with discretion), exemption fails entirely.

The Tribunal also rejected the assessee’s retraction of statements as belated and unsupported, relying again on Mac Public Charitable Trust, which requires prompt and substantiated retraction. Further, student affidavits denying capitation payments were held unreliable, as they were self-serving.

Accordingly, the ITAT held that collection of capitation fee destroys the very foundation of charitable status, allowed the Revenue’s appeals, and dismissed the assessee’s appeal.

FULL TEXT OF THE ORDER OF ITAT BANGALORE

This appeal at the instance of the assessee is directed against the order of ld. CIT(A), Bengaluru-12 dated 29.07.2025vide DIN & Order No: ITBA/APL/S/250/2025-26/1079024975(1) passed u/s. 250 of the Income Tax Act, 1961 (in short “the Act”) for the AY 2015-16.

2. The assessee has raised the following grounds of appeal: –

1. The appellate order passed by the Learned Commissioner of Income-tax [Appeals] NFAC, Delhi passed under Section 250 of the Act dated 29/07/2025 for the impugned Assessment Year 2015-16, in so far as it is against the Appellant is opposed to law, weight of evidence, probabilities, facts and circumstances of the Appellant’s case, requires to be quashed.

2. The appellant denies himself liable to be assessed on a total income of Rs. 6,22,198/-on the facts and circumstances of the case.

3. The Order passed u/s.147 of the act is bad in law, since the order issued u/s.148A(d) dated 30.03.2022 is without jurisdiction since the Order was issued by the Jurisdictional Assessing officer [International Taxation], Ward 1[1], Bangalore, which was ought to have been issued by National Faceless Assessemnt Cente in accordance with Notification No. 15/2022/F. No. 370142/13/2022-TPL “Faceless Jurisdiction of Income tax Authorities Scheme, 2022”, dated 28.03.2022

4. The Order passed u/s.147 of the act is bad in law, since the notice issued u/s.148 of the act dated 30.03.2022 was issued by the Jurisdictional Assessing officer [International Taxation], Ward 1[1], Bangalore, instead which was ought to have been issued by taxational Faceless Assessement Centre in accordance with Notification No. 15/2022/F. No. 370142/13/2022-TPL “Faceless Jurisdiction of Income tax Authorities Scheme, 2022”, dated 28.03.2022. The appellant places reliance on the following decisions –

i) Kankanala Ravindra Reddy v. ITO (2023) 156 com178 (Tel.)

ii) Hexaware Technologies Ltd. v. ACIT (2024) 162 com225 (Born.)

iii) Jatinder Singh Bhangu (2024) 165 com115 (P&H)

iv) Venus Jewel v. ACIT (2024) 164 com414 (Born.)

v) Paras Mahendra Shah v. U01 [2024] 165 com546 (Born.)

vi) Ram Narayan Sah v. U0112024] 163 com478 (Gauhati)

vii) Navita S. Hetampuria v. Income-tax officer [2024] 165 com424 (Born.)

viii) Royal Bitumen Private Limited v. ACIT [2024] 164 com606 (Born.)

ix) Pravina Jagdish Patel v. Income-tax officer [2024] 164 com659 (Born.)

x) Sushila Sureshbabu Malge v. Income-tax officer [2024] 164 com633 (Born.)

xi) Jasjit Singh v. U01 [2024] 165 com114 (P a H)

xii) Govind Singh v. Income-tax officer [2024] 165 com113 (Himachal Pradesh)

xiii) Sandeep Kumar Gupta v. U01 [2024] 165 com438 (P & H)

xiv) Vidhyadhar Shetty v. Income-tax officer [2024] 165 com265 (Born.)

xv) LET Finance Ltd. v. ACIT [2024] 165 com331 (Born.)

xvi) Everest Kanto Cylinder Ltd. v. DCIT [2024] 165 com192 (Born.)

xvii) Ramachandra Reddy Ravikumar v. DCIT in W.P. No. 28182 of 2024 dated 28.08.2025

xviii) Dadha Pharma LLP v. DCIT in W.P. No. 35385 of 2024 and connected matters dated 24.06.2025 (Mad.)

xix) Southern Power Distribution Company of Telangana Ltd. v. ACIT (2025) 175 com800 (Tel.)

5. The Order passed by the learned Assessing Officer u/s.148A(d) is bad in Law as the Appellant had clearly explained the source of income of Rs. 52,41,475/- which was the information mentioned by the learned Assessing officer in the notice u/s. 148A(b) and accordingly, there was no unexplained income in excess of Rs. 50 lakhs and accordingly the entire Order u/s. 148A(d) is bad in Law. Reliance is placed on the following case laws:

i. Income Tax Officer Vs. Sanath Kumar Murali reported in 172 com290 [ Kar High Court]

ii. Anand Kumar Somasheshkaraya Lonarmath Vs. Income Tax Officer, Ward – I in Writ Petition No. 201029 of 2024, Hon’ble Karnataka High Court, KaLburgi Bench

iii. Hon’ble Karnataka High Court in Pramila Mahadev Tadkase Vs. Income Tax Officer reported in 158 com246.

iv. Hon’ble Jurisdictional Income Tax Appellate Tribunal in the case of Smt. Neelamma Vs. ITO, Ward – 1, Shivmogga.

6. The learned assessing officer has erred in re-opening the assessment u/s.148A(d) of the act, since the learned assessing officer has accepted the same documents submitted by the appellant in response to the notice issued u/s.148A of the act, explaining the source of investments made by the appellant to the tune of Rs.52,41,475/- while passing the assessment order u/s.147 of the act.

3. The Brief facts of the case are that the assessee, being a non-resident, did not file his return of income on the footing that his income in India was way below the maximum amount, which is not chargeable to income tax for the assessment year 2015-16. There was credible information available with the department which suggested that for the assessment year 2015-16, the assessee had received/derived income being excess of Rs.50 lakhs, which represented in the form of an asset i.e. immovable property being land or building or both as per explanation to section 149(1) of the Act. On examination of information available on record, it was seen that the assessee had purchased immovable property for a consideration of Rs.57,47,954/. Further, it was also seen that the assessee had received taxable interest income of Rs.14,655/- from Axis Bank Ltd and accordingly, a show cause notice u/s 148A(b) of the Act was issued to the assessee on 19.3.2022 along with the details of the information and enquiry contained in Annexure. The assessee in response to the said show cause notice issued u/s 148A(b) of the Act, filed his reply on 25.3.2022 vide Acknowledgement No. 424448901250322 affirming that he is a non-resident and did not have any sources of income in India except interest on deposits and therefore, he was not required/liable to file any return of income for the assessment year 2015-16 in India. The assessee also confirmed to have purchased an immovable property worth Rs.57,47,954/-, which was acquired by borrowing housing loan worth Rs.42,75,000/- from the Axis Bank Ltd. jointly with Mrs. Anisha Ann Dsouza, wife of Nikhil Chandran and the balance amount of Rs.14,72,954/- was paid out of the assessee’s personal savings which was earned in the form of salary abroad as well as while he was resident in India and paid the applicable tax due thereon. Lastly, regarding the interest income of Rs.14,655/- from the deposit with Axis Bank Ltd, the assessee submitted that the bank had already deducted the TDS@ 30%amounting to Rs.4,531/-& there was no escapement of Income. Further, while uploading the reply to the said show cause notice on 25/03/2022, the assessee had also uploaded the housing loan sanction letter, copy of 26AS, evidence in respect of investment made in properties & Bank statement for the FY 2014-15 relevant for the AY 2015-16. The AO, thereafter, passed an order u/s 148A(d) of the Act on 30.3.2022 by merely asserting that the assessee had not furnished any evidence in the sources of income other than bank statements and accordingly held that the assessee had not explained the sources for investment with documentary evidence. In view of the above, the AO was of the opinion that it is a fit case to issue notice u/s 148 of the Act. The AO, thereafter on the same day i.e. on 30.3.2022 issued notice u/s 148 of the Act and directed the assessee to furnish return of income for the assessment year 2015-16 within 30 days from the date of service of notice.

3.1 In response to the notice issued u/s 148 of the Act, the assessee filed his return of income for the assessment year 2015-16 on 25.4.22 declaring total income of Rs.15,678/- only and claimed refund of Rs.4,531/- along with interest u/s 244A thereon. Thereafter, the AO issued notice u/s 143(2) of the Act as well as u/s 142(1) of the Act along with the show cause notice dated 23.2.2023 calling for various details. In response to the notices, the assessee responded and furnished the details as called for by the AO. During the course of the assessment proceedings, the AO observed that the assessee had purchased an immovable property situated at Flat No.A404, A-Block, 4th Floor, Plasma Heights, Hennure Village, Bengaluru-560043 and paid consideration of Rs.52,41,475/-. The AO also observed that for this purchase, the assessee had also incurred an expenditure of Rs.4,36,520/-towards stamp duty and registration charges. The AO further observed that the assessee although responded to the notices but did not furnish any explanation regarding the sources of stamp duty and registration charges paid and in the absence of any details furnished by the assessee regarding stamp duty and registration charges amounting to Rs.4,36,520/-, the same was proposed to be treated as unexplained investment u/s 69 of the Act. Further, during the course of assessment proceedings, the AO noticed that during the year under consideration, the assessee had also made cash deposit of Rs.1,70,000/- in the Axis Bank account on 18.10.2014. As the assessee failed to explain the sources of cash deposit of Rs.1,70,000/- along with supporting documentary evidences to establish the genuineness of his claim, the cash deposits made in the bank account amounting to Rs.1,70,000/-was also treated as unexplained money u/s 69A of the Act and the same is taxed u/s 115BBE of the Act. Thus, the AO completed the assessment proceedings u/s 147 r.w.s. 143(3) of the Act on 14.3.2023 on a total assessed income of Rs.6,06,520/- by completely ignoring the return of income filed by the assessee on 25.4.2022 declaring income of Rs. 15,678/-.

4. Aggrieved by the assessment completed u/s 147 r.w.s. 143(3) of the Act on 14.3.2023, the assessee preferred an appeal before the ld. CIT(A), Bengaluru-12.

5. The ld. CIT(A) dismissed the appeal of the assessee since despite issuing 5 number of notices, the assessee neither appeared nor filed any written submission in respect of grounds of appeal and statement of facts. In view of the above, the ld. CIT(A) believed that the assessee was not aggrieved with the assessment order and therefore, not interested in prosecuting the same and accordingly left with no option but to dismiss the appeal of the assessee.

6. Again, aggrieved by the order of the ld. CIT(A)-12, Bengaluru, the assessee has filed the present appeal before this Tribunal. The assessee has also filed a paper book comprising 121 pages in support of his case.

7. Before us, the ld. A.R. of the assessee vehemently submitted that the assessee is a non-resident and did not have any source of income in India except interest on deposits. Further, during the year under consideration, the assessee had purchased an immovable property amounting to Rs.57,47,954/- and obtained a housing loan of Rs.42,75,000/- from the Axis Bank Ltd. and the balance amount of Rs.14,72,954/- was paid from the assessee’s personal savings earned in the form of salary abroad as well as in India in past years. Further, the ld. A.R. of the assessee vehemently submitted that during the course of proceedings u/s 148A of the Act, the assessee had submitted the housing loan sanctioned letter along with the copy of the Bank statement and statement of the Plama Developers Ltd. However, the AO ignoring all these materials proceeded to pass an order u/s 148A(d) of the Act by merely stating that the assessee had not furnished any evidences for the sources of investment other than bank statement. Lastly, the ld. A.R. submitted that the order passed u/s 147 of the Act is also time barred as there was no unexplained income in excess of Rs.50 lakhs and therefore, the AO grossly erred in law in invoking the extended period.

8. The ld. D.R. on the other hand, supported the order of the authorities below and vehemently submitted that as the assessee could not furnish the sources of investment as well as sources of the cash deposits as called for by the AO, the AO had rightly added the same u/s 69 & 69A of the Act. Further, it is submitted that as the assessee could not represent his case before the ld. CIT(A), the case may be remitted back to the file of ld. CIT(A) with a direction to the assessee to submit all the details in order to substantiate his claim.

9. We have heard the rival submissions and perused the materials available on record. Undisputedly, the show cause notice u/s 148A(b) of the Act dated 19.3.2022 was issued after obtaining the prior approval of the ld. PCCIT, Karnataka & Goa for the sole reason that the assessee had purchased an immovable property for a consideration of 57,47,954/- and also received interest income of Rs.14,655/-, however, it was seen that the assessee had not filed any return of income for the assessment year 2015-16 and thus failed to disclose the sources of investment in the immovable property. We observed that in response to the said show cause notice dated 19/03/2022, the assessee had filed a detailed reply on 25.3.2022 vide e-proceedings response acknowledgement no.424448901250322 by submitting that the assessee is a non-resident during the assessment year 2015-16 and did not have any source of income in India except interest on deposits and therefore, he was not required to file any return of income for the AY 2015-16. Further, in his reply dated 19/03/2022, the assessee had categorically stated that he had purchased an immovable property from the Plama Developers Ltd. amounting to Rs.57,47,954/- by borrowing housing loan worth Rs.42,75,000/- from Axis Bank jointly with Mrs. Anisha Ann Dsouza (wife) and the balance of Rs.14,72,954/- was paid out of his personal savings which was earned in the form of salary abroad as well as in India for the past years. He had also categorically stated to have deducted TDS of Rs.57,480/- while making payment to the builder. The assessee had also submitted that the interest income of Rs.14,655/- from the deposit with Axis Bank was also subjected to the TDS @ 30% amounting to Rs.4,531/-& therefore there is no escapement of income. We take note of the fact that the assessee while uploading his reply on 25/03/2022 had also attached the copy of Axis Bank statements for the FY 2014-15 along with Axis Bank Housing Loan sanctioned letter, copy of form 26AS and evidence in respect of investment made in properties. We also take note of the fact that the AO while passing the order u/s 148A(d) of the Act on 30.3.2022 had merely stated that the assessee had not furnished any evidences for the sources of income other than bank statements and therefore, the AO was of the opinion that as the assessee had not explained the sources of investment with documentary evidences and accordingly held to be a fit case to issue notice u/s 148 of the Act by passing perverse order u/s 148A(d) of the Act.

9.1 We are of the considered opinion that the AO had not passed a speaking & reasoned order & merely stated that the assessee had not furnished any evidence other than bank statements. The AO while passing the order u/s 148A(d) had not discussed as to why the explanations & evidences like loan sanctioned letter, bank statements& statements of builders furnished by the assessee were not acceptable. It appears that while considering the reply of the assessee and before passing the impugned order u/s 148A(d) of the Act, highly casual and perfunctory approach was adopted, turning a Nelson’s eye towards the palpable & elementary aspect of Purchase of immovable property by obtaining the housing loan &sources from self-personal savings earned from salary in India & abroad & the income chargeable to tax. Merely because the assessee had purchased an immovable property, that would not ultimately culminate into the income escaping assessment. The provisions under section 148A were inserted in the Act w.e.f. 01/04/2021 to render the power of Revenue of reopening cases to more transparent so as to avoid casual invocation of section 147-148 of the Act. The insertion of section 148A of the Act not only saves the assessee from casual commencement of proceedings u/s 147-148 of the Act but also save the Revenue of precious time and energy which may be wasted in pursuing fruitless, frivolous and vexatious cases. The Hon’ble Madhya Pradesh High Court in the case of M/s Amrit Homes Private Limited Vs. Deputy Commissioner of Income Tax & Anr. in W.P. No. 15244/2023 dated 09/08/2023 has held as under-

“7.2 The object behind insertion of section 148A by the Legislature w.e.f. 01/04/2021 interalia appears as follows: –

(a) To prevent rampant and casual issuance of notice u/s 148 by the Revenue;

(b) To save unnecessary harassment to the assessee of being subjected to re-opening a case under section 148;

(c) To save the Revenue of the time and energy which may be vested pursuing frivolous and fruitless proceedings u/s 148.”

We observed that in fact when the assessee filed a reply to the notice u/s 148A(b) of the Act on 25/03/2022, it clearly revealed that the amount of Rs. 57,47,954/- paid towards the Purchase of immovable property was only after obtaining the housing loan of Rs.42,75,000/- from the Axis Bank. Meaning thereby the income chargeable to tax would obviously be less than 50 lakhs even if the AO disbelieved the explanation of the assessee with regard to balance amount of Rs.14,72,954/- which the assessee claimed to have earned in the form of salary in abroad as well as in India. Clearly when the procedure is followed culminating in an order passed u/s 148A(d) of the Act, the Authority is required to apply his/her mind and consider the reply of the assessee and pass a considered order. In the present case, the AO had not applied his mind to the reply filed, nor noticed the legal position while deciding as to the application of the extended period u/s 149(1)(b) of the Act.

9.2 The contention of assessee that his income for the AY 2015-16 was way below the maximum amount which is not chargeable to income tax& for this reason he did not file his return of income found to be correct. This is also supported from the fact that even in response to notice u/s 148 of the Act, the assessee had filed his return of income by declaring Total income of Rs. 15,678/- only and claimed refund of Rs. 4531/- along with interest u/s 244A thereon which was completely ignored by the AO while passing the order u/s 147 of the Act. More surprisingly, ongoing through the assessment order passed u/s 147 r.w.s. 143(3) of the Act, we also observed that during the course of assessment proceedings, the AO had also issued a show cause notice on 23.2.2023 in which the assessee was asked to furnish the explanation regarding the proposed addition under the head “Unexplained money” u/s 69A of the Act amounting to Rs.1,70,000/- and addition under the capital gain u/s 45 of the Act amounting to Rs.4,36,520/-. We noticed that the AO in para 3 of the said show cause notice dated 23.2.2023 had alleged that since the assessee did not respond to the notice, the order u/s 148A(d) of the Act was passed on 30.3.2022 and accordingly notice u/s 148 of the Act was issued on 30.3.2022 which in our opinion is completely incorrect & baseless. We also observed that while concluding the assessment proceedings again surprisingly, the AO had finally added only Rs.4,36,520/- as unexplained investment u/s 69 of the Act r.w.s. 115BBE of the Act while in the show cause notice dated 23.2.2023, it was proposed to be added under the head capital gain u/s 45 of the Act. Thus, the AO himself was in dilemma under which head the addition is to be made. Further, while concluding the assessment proceedings, the AO had also added an amount of Rs.1,70,000/- as unexplained money u/s 69A of the Act since the assessee in the opinion of AO had failed to establish the sources of cash deposits which was never the case of the AO for reopening the assessment proceedings. Thus, from the discussion above, we noticed that the AO initiated the proceedings u/s 148A of the Act for the alleged income escaping of Rs.57,62,609/-, however, concluded the assessment proceedings on a total assessed income of Rs.6,06,520/- only. We are of the considered opinion that the AO in the guise of the reopening of the assessment proceedings had only made a roving & phishing enquiry based on unfounded suspicion only. We take note of the fact that in the present case, the income stated to have escaped assessment which has been taken note of seeking to re-open the assessment for AY 2015-16 is the purchase transaction with Plama Developers Ltd. on which the assessee had also deducted tax at source while making the payment.

9.3 Before proceeding further, it is apposite here also to take note of the erstwhile section 149 of Act as applicable at the time of issuing the notice u/s 148 of the Act for the purpose of this case which read as under-

2 [Time limit for notice.

149. (1) No notice under section 148 shall be issued for the relevant assessment year,—

(a) if three years have elapsed from the end of the relevant assessment year, unless the case falls under clause (b);

(b) if three years, but not more than ten years, have elapsed from the end of the relevant assessment year unless the Assessing Officer has in his possession books of account or other documents or evidence which reveal that the income chargeable to tax, represented in the form of asset, which has escaped assessment amounts to or is likely to amount to fifty lakh rupees or more for that year:

Provided that no notice under section 148 shall be issued at any time in a case for the relevant assessment year beginning on or before 1st day of April, 2021, if such notice could not have been issued at that time on account of being beyond the time limit specified under the provisions of clause (b) of subsection (1) of this section, as they stood immediately before the commencement of the Finance Act, 2021:

Provided further that the provisions of this sub-section shall not apply in a case, where a notice under section 153A, or section 153C read with section 153A, is required to be issued in relation to a search initiated under section 132 or books of account, other documents or any assets requisitioned under section 132A, on or before the 31st day of March, 2021:

Provided also that for the purposes of computing the period of limitation as per this section, the time or extended time allowed to the assessee, as per showcause notice issued under clause (b) of section 148A or the period during which the proceeding under section 148A is stayed by an order or injunction of any court, shall be excluded:

Provided also that where immediately after the exclusion of the period referred to in the immediately preceding proviso, the period of limitation available to the Assessing Officer for passing an order under clause (d) of section 148A is less than seven days, such remaining period shall be extended to seven days and the period of limitation under this sub-section shall be deemed to be extended accordingly. Explanation.—For the purposes of clause (b) of this sub-section, “asset” shall include immovable property, being land or building or both, shares and securities, loans and advances, deposits in bank account.

(2) The provisions of sub-section (1) as to the issue of notice shall be subject to the provisions of section 151.]

2. Sub. by the Act No. 13 of 2021, w.e.f. 1-4-2021.

Thus, as per Section 149(1) of the Act substituted by the Finance Act, 2021 w.e.f 01/04/2021 “No notice under section 148 shall be issued for the relevant assessment year-

(a) If three years have elapsed from the end of the relevant assessment year, unless the case falls under clause(b);

(b) If three years, but not more than ten years, have elapsed from the end of the relevant assessment year unless the Assessing Officer has in his possession books of accounts or other documents or evidences which reveal that the income chargeable to tax, represented in the form of asset, which has escaped assessment amounts to or is likely to amount to fifty lakh rupees or more for that year.

9.4 Thus, section 149 of the Act stipulates restrictions on issuance of notice u/s 148 of the Act & not on conducting any enquiry with respect to the information which suggests that the income chargeable to tax has escaped assessment by providing an opportunity of being heard to the assessee as per the provisions contained u/s 148A(b) of the Act. Thus, there is a clear distinction between 148A proceedings and 148-147 proceedings. The Revenue is free to conduct enquiry based on the information, but once during the course of 148A proceedings, the AO found that the income which has escaped assessment amounts to or likely to amount to less than fifty lakh rupees, the AO should restrain himself to proceed further & drop the proceedings if three years have already elapsed from the end of the relevant assessment year. The AO cannot invoke the extended period thereafter for reopening the assessment by issuing the notice u/s 148 of the Act. We are of the considered opinion that in order to grab the extended period of 10 Years as per clause (b) of the Section 149 (1) of the Act, the AO has to satisfy the conditions enumerated as below-

- AO has in possession——— Books of Accounts or other documents or evidence

- Which reveal——— Income Chargeable to Tax in the Form of Asset/Expenditure/entry(s) in books of A/c.

- Which escaped Assessment——— Amounts to or is likely to amount to 50 lakhs or more

As per the Clause (a) of Section 149(1) of the Act, the impugned notice U/s 148 dated 30/03/2022 could have been issued up to 31/03/2019. Thus, the time limit for issuing the notice U/s 148 for the Asst. Year 2015-16 was 31/03/2019 & have been time barred by virtue of the Clause (a) of section 149(1) of the Act. In the present case, the sole reason for the reopening of the case was based on credible information that the assessee had purchased an immovable property worth Rs.57,47,954/-. The assessee during the course of 148A proceedings demonstrated that investment in immovable property worth Rs.57,47,954/-, was made by borrowing housing loan worth Rs.42,75,000/- from the Axis Bank Ltd. jointly with Mrs. Anisha Ann Dsouza, wife of Nikhil Chandran and the balance amount of Rs.14,72,954/- was paid out of the assessee’s personal savings which was earned in the form of salary abroad as well as while he was resident in India and paid the applicable tax due thereon. The AO during the course of 148A proceedings neither brought any adverse material on record nor found the claim of obtaining the Housing loan to be sham. The assessee had produced the Housing loan sanctioned letter along with the bank statement to substantiate his claim. At most, the AO could have disbelieved is only the balance amount of Rs.14,72,954/- which was claimed to be paid out of the assessee’s personal savings earned in the form of salary abroad as well as while he was resident in India which is also way below the limit of 50 lakhs. In these circumstances, we are of the considered opinion that the case of the assessee does not fall under the Clause (b) of Section 149 of the Act as no income chargeable to tax, represented in the form of undisclosed asset, which has escaped assessment amounts to or is likely to amount to fifty lakh rupees or more for that year. Our view also gets support from the fact that the AO had initiated the proceedings based on a suspicion that the entire purchase of immovable property worth Rs.57,47,954/- had escaped assessment, however finally ended with the conclusion by saying only expenditure towards stamp duty & registration charges amounting to Rs.4,36,520/- remained unexplained & hence treated as unexplained investment u/s 69 of the Act. We are also of the firm opinion that AO was not in possession of any books of account or other documents or evidences which reveal that income chargeable to tax has escaped assessment is likely to amount to Rs. 50 lakhs or more for that year & therefore the AO grossly erred in invoking the extended time period provided u/s 149(1)(b) of the Act.

9.5 In view of the above, the order passed u/s 148A(d) of the Act is set aside and the notice issued u/s 148 of the Act for the AY 2015-16 is also quashed as barred by limitation and accordingly the Assessment order u/s 147 of the Act dated 14/03/2023 is also quashed.

10. In the result the appeal filed by the assessee is allowed.

Order pronounced in the open court on 24th Apr, 2026