From April 1, 2026, the TDS/TCS regime will see a major overhaul under the new Income Tax Act, with renumbered sections and simplified compliance processes. In NRI property deals, buyers can use PAN instead of TAN from October 2026, while lower/nil TDS certificates will move to a fully electronic system.

The Income Tax Act 2025/Rules 2026 come into force, requiring updated systems. Key changes include renumbering sections into 392, 393, and 394.

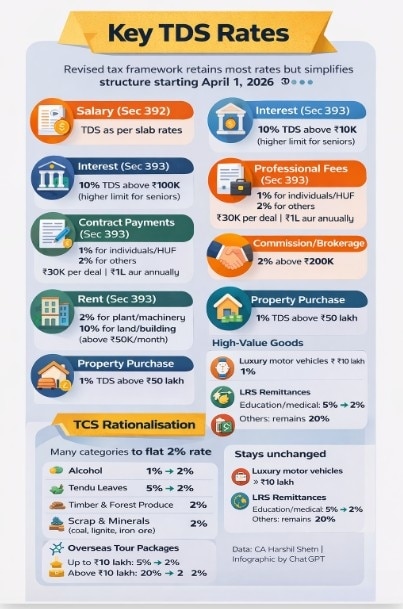

TDS, TCS rates: India’s tax compliance framework is set for a structural overhaul in Tax Year 2026–27 (FY 2026–27), with sweeping changes to Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) under the new Income Tax Act. Effective April 1, 2026, the reforms aim to simplify compliance, standardise rates, and introduce a clear cross-mapping of sections between the old and new regimes. Key provisions include renumbering of TDS sections into 392, 393, and 394, along with procedural simplification across multiple areas.

For property transactions involving NRI sellers, resident buyers and HUFs will no longer need a TAN from October 1, 2026, and can rely on PAN, easing compliance. The process for obtaining lower or nil TDS certificates will shift to a fully electronic system, replacing manual assessments, according to a detailed compilation by CA Harshil Sheth.

Section renumbering

One of the most notable changes is the renumbering of TDS/TCS provisions. As highlighted by CA Sheth:

Section 192 (salary) becomes Section 392 (Code 1002)

Section 194A (interest) shifts to Section 393 (Code 1022)

Section 194C (contract payments) maps to Section 393 (Codes 1023/1024)

TCS Section 206C transitions to Section 394 series (Codes 1068 onwards)

This restructuring introduces a uniform coding system, making compliance and tracking more efficient.

New TDS/TCS Return Forms

Sheth’s analysis also points to a major shift in return filing formats:

Form 24Q (salary TDS) → Form 138

Form 26Q (non-salary TDS) → Form 140

Forms 26QC/26QB/26QD/26QE → consolidated into Form 141

Form 27EQ (TCS) → Form 143

This consolidation reduces complexity and aligns filings with the new law.

Key TDS Rates and Thresholds

According to CA Sheth’s compilation, the revised framework largely retains existing rates but standardises their application:

Salary (Sec 392): TDS as per slab rates, factoring rebate under Section 87A

Interest (Sec 393): 10% TDS; threshold ₹10,000, with higher limits for specified cases

Contract payments:

1% for individuals/HUF

2% for others (₹30,000 per transaction; ₹1 lakh annually)

Professional fees:

10% for professional services

2% for technical services

Commission/Brokerage: 2% above ₹20,000

Rent:

2% for plant/machinery

10% for land/building (₹50,000/month threshold)

Property purchase: 1% TDS above ₹50 lakh

Purchase of goods: 0.1% where turnover exceeds ₹10 crore and purchases exceed ₹50 lakh

Provisions such as payments by individuals/HUFs above ₹50 lakh continue to attract 2% TDS under the revised structure.

TCS rationalisation

A key highlight flagged by Sheth is the rationalisation of TCS rates, with several categories converging to a 2% rate from April 2026:

Alcohol: 1% → 2%

Tendu leaves: 5% → 2%

Timber and forest produce: 2%

Scrap and minerals: 2%

Overseas tour packages:

Up to ₹10 lakh: 5% → 2%

Above ₹10 lakh: 20% → 2%

However, certain categories remain unchanged:

Motor vehicles above ₹10 lakh: 1%

LRS remittances:

Education/medical: 5% → 2%

Others: 20%

High-value transactions

Sheth’s note also highlights continued TCS applicability on luxury and high-value goods, including watches, handbags, collectibles, yachts, and premium equipment. These fall under newly mapped codes, enabling better reporting and tracking of discretionary spending.

Simplified compliance

The changes are designed to simplify compliance, particularly through:

Consolidated return forms

Clear thresholds across sections

Standardised rates

“This is a move towards a cleaner, more structured TDS-TCS regime with better alignment between provisions and reporting,” CA Sheth notes.

As per CA Sheth’s comprehensive snapshot, the TDS and TCS overhaul for Tax Year 2026–27 focuses less on changing rates and more on simplification, consistency, and ease of compliance. For taxpayers and businesses alike, adapting to new section codes, forms, and standardised rates will be key to smooth compliance under the new tax regime.