Clipped from: https://taxguru.in/income-tax/itat-hyderabad-ao-exceed-limited-scrutiny-scope-entire-assessment-held-invalid.html

Krishna Constructions Vs ITO (ITAT Hyderabad)

ITAT Hyderabad: AO Cannot Exceed Limited Scrutiny Scope – Entire Assessment Held Invalid

In this case, the assessee’s scrutiny was specifically limited to verification of cash deposits under CASS. However, the Assessing Officer (AO) went beyond this mandate and examined the entire bank credits, ultimately making additions of over ₹2.20 crore by treating them as business income and unexplained money.

The Tribunal held that such action is clearly beyond jurisdiction, as CBDT instructions strictly restrict the AO from expanding the scope of limited scrutiny without prior approval of the competent authority and without specific triggering information from enforcement agencies.

Since:

- No approval was taken for converting limited scrutiny into complete scrutiny

- No external information justifying expansion existed

- AO made additions on issues unrelated to the original scrutiny (cash deposits)

the ITAT concluded that the AO had violated binding CBDT instructions and travelled beyond jurisdiction.

Accordingly, the entire assessment was held invalid (void ab initio) and the additions were liable to be deleted.

In limited scrutiny cases, any addition beyond the specified issue-without proper procedure-renders the assessment itself unsustainable in law.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

This appeal by the Assessee is directed against the Order dated 03.07.2025 of the learned CIT(A)-National Faceless Appeal Centre [in short “NFAC], Delhi, for the assessment year 2017-2018.

2. The assessee has raised the following grounds of appeal:

i. “On the facts and in the circumstances of the case, and in law, the order passed by the Learned Assessing Officer (“AO”) u/s 143(3) of the Income-tax Act, 1961 (“the Act”) for AY 2017-18 and confirmed by the Learned Commissioner of Income-tax (Appeals), hereinafter referred to as CIT(A), is bad in law and liable to be quashed.

ii. On the facts and in the circumstances of the case, and in law, the Learned AO erred in making additions in the assessment order passed u/s 143(3) of the Act, which are beyond the scope of the limited scrutiny of the assessee’s case for AY 2017-18, and are without jurisdiction and liable to be deleted.

iii. On facts and in the circumstances of the case and in law, the Ld. CIT(A) erred in confirming action of AO in passing assessment order for AY 2017-18 by ignoring relevant CBDT (Central Board of Direct Taxes) Instruction issued vide F.No. F.No. 225/ 402/ 2018/ ITA.II dated 28.11.2018 for scope of enquiry in limited scrutiny cases that in limited scrutiny cases AO cannot travel beyond the issues for which the case was selected and AO shall not expand the scope of enquiry/ investigation beyond the issues on which the case was flagged for limited scrutiny whereas in this case scope of enquiry/ investigation and assessment order should have been limited to cash deposits made during demonetization period and not on the issue of examination of all the credits made in the bank accounts of the assessee.

iv. On the facts and in the circumstances of the case, and in law, the Learned Assessing Officer (“AO”) erred in expanding the scope of “limited scrutiny” of the assessee beyond the examination of “cash deposits”, covering additional issues that were not identified for examination under the scrutiny as per the notice issued u/ s 143(2) of the Income-tax Act, 1961 (“the Act”) for AY 2017-18. In fact, the total amount of cash deposited in the two bank accounts of the assessee for AY 2017-18 stands at Rs. 8,22,000/ -, whereas the AO examined all the credits made in the bank accounts of the assessee and made an unjustifiable addition of Rs. 2,20,45,610/ –

v. On the facts and in the circumstances of the case, and in law, the Ld. AO erred in expanding the scope of limited scrutiny in the case of the assessee for AY 2017-18 as against the mandatory prohibition laid down by the CBDT Instruction to expand the scope of limited scrutiny or to convert into complete scrutiny of the case except to the issue where credible material or information has been/ is provided by any law-enforcement/ intelligence/ regulatory authority or agency regarding tax-evasion by an assessee, which is not case here.

vi. On the facts and in the circumstances of the case, and in law, the Ld. CIT(Appeals) erred in confirming the action of the Ld. AO in treating the entire deposits made into the bank account of Rs.2,17,54,080/ – as the income of the assessee.

vii. On the facts and in the circumstances of the case, and in law, the Ld. CIT(Appeals) erred in confirming the action of the Ld. AO in treating the investment made by the partners into the firm out of their contract income of Rs.2,20,45,610/ – as the income of the assessee.

viii. On the facts and in the circumstances of the case, and in law, the Ld. CIT(A) erred in not accepting the explanation submitted by the assessee based on the evidences to this effect that were filed before him and in spite of the fact that the entire amount from the partners was received through banking channels.

ix. On the facts and in the circumstances of the case, and in law, and without prejudice to other grounds, the Ld. CIT(A) erred in confirming the action of the Ld. AO in treating entire gross receipts of Rs.2,20,45,610/ – as business income instead of profit element embedded in it.

x. On the facts and in the circumstances of the case and in law, Ld. CIT(Appeals) erred in upholding the addition of Rs.2,20,45,610/ – made by Ld. AO without properly appreciating the submission advanced by the assessee and hence, the said addition of Rs.2,20,45,610/ – is not sustainable in law.]

xi. On the facts and in the circumstances of the case and in law. Ld. CIT(Appeals) as well as Ld. AO erred in rejecting the proper and valid explanations and evidences submitted by the assessee in support of source of partner’s contribution to the firm and Ld. CIT(Appeals)/ AO should have allowed the same as explained.

xii. On the facts and in the circumstances of the case and in law, Ld. CIT(Appeals) erred in concluding that the whole amount of deposits/ credits amounts to unexplained money in the hands of the appellant firm and deemed to be its income u/s 69A of the Act, when the AO assessed such income as business income and moreover when the amount received by the assessee through banking channel would not amount to any “money” as contemplated u/s 69A of the Act.

xiii. On the facts and in the circumstances of the case and in law, Ld. CIT(Appeals) erred in confirming the action of the AO who concluded that the gross business receipts of the assessee amount to Rs.2,20,45,610/ – as against NIL revenue shown by the assessee and that the assessee ought to have maintained the books of account and get the same audited as per the provisions of sec.44AB of the Act.

xiv. On the facts and in the circumstances of the case and in law, Ld. CIT(Appeals) erred in confirming the action of the AO that the assessee did not file Form 3CB/ 3CD thereby violated the provisions of Sec.44AB and that as the assessee has neither maintained any books of account nor got them audited as per the provisions of Section 44AB of the Act, the assessee is liable for penalty for noncompliance to the provisions of Sec.44AA and 44AB of the Act.

xv. On the facts and in the circumstances of the case and in law, Ld. CIT(Appeals) erred in confirming the action of the AO that assessee though having turnover above Rs. 1 crore has failed to file the Form 3CB and 3CD Report under the Income-tax Rules, 1962.

xvi. The Appellant craves leave to add, amend, modify, alter, revise, substitute, or not press any or all grounds of the appeal, if deemed necessary at the time of hearing of the appeal, in the interest of justice.”

3. Ground nos.(i) to (v) are regarding validity of the assessment order passed u/sec.143 (3) of the Income Tax Act [in short “the Act], 1961 as the Assessing Officer has breached the jurisdiction by expanding the scope of scrutiny from limited scrutiny under Computer Assisted Scrutiny Selection [in short “CASS”‘ without proper sanction of the Competent Authority. The assessee has also filed a petition under Rule-11 of I.T. Rules, 1962 for raising these grounds as additional grounds.

4. The learned Authorised Representative of the Assessee has submitted that this issue raised by the assessee is purely legal in nature and can be adjudicated on the basis of material and facts available on record. Therefore, he has submitted that the legal issue goes to the root of the matter may be admitted by this Tribunal. In support of his contention, he has relied upon the Judgment of Hon’ble Supreme Court in the case of National Thermal Power Co. Ltd. vs. CIT [1998] 229 ITR 383 (SC). The learned Authorised Representative of the Assessee has submitted that the Assessing Officer has undisputedly travelled beyond the scope of limited scrutiny as the case of the assessee was selected for limited scrutiny under CASS only on the issue of cash deposit during the year. However, the Assessing Officer while framing the assessment has made the additions of the entire credits/deposits in the bank account of the assessee firm which is in complete violation of CBDT’s instructions issued from time to time including Instruction No.20/2015, 5/2015 and F.225/402/18 dated 28.11.2018 which mandates that the scope of enquiry shall be confined strictly to the issues for which the case was selected. Extension to the complete scrutiny requires prior written approval of the Competent Authority with the condition that the assessee must be informed for such conversion. Thus, the learned Authorised Representative of the Assessee has submitted that the additional grounds raised by the assessee challenging the jurisdiction of the Assessing Officer be admitted for adjudication.

5. On the other hand, the learned DR has objected to the admission of the additional grounds and submitted that once the assessee was given an opportunity during the assessment proceedings on the issue of deposits in the bank account as well as other transactions carried out in the bank account of the assessee, then there is no violation of any instruction of the CBDT.

6. We have considered the rival submissions as well as relevant material on record. There is no dispute that the case of the assessee was selected for limited scrutiny under CASS for examination of the issue of cash deposits during the year. The Assessing Officer in the assessment framed u/sec.143(3) of the Act has made the additions on account of the entire credit in the bank account of the assessee. Therefore, prima facie it appears that the Assessing Officer has expanded the scope of scrutiny without any sanction from the Competent Authority. This issue is purely legal in nature and can be decided based on the facts already available on record. Therefore, for adjudication of this issue no fresh investigation or examination of the fact are required. Accordingly, in view of the Judgment of Hon’ble Supreme Court in the case of National Thermal Power Co. Ltd. vs. CIT (supra), we admit the additional grounds raised by the assessee challenging the jurisdiction of the Assessing Officer while passing the assessment order.

7. On merits of the additional grounds, the learned Authorised Representative of the Assessee has submitted that the Assessing Officer issued notice u/sec.143(2) of the Act for taking up the case of the assessee for limited scrutiny under CASS for examination of the issue of cash deposit during the year. In response to the said notice as well as notice u/sec.142(1) of the act, the assessee filed complete record and bank account statement, computation of total income as well as the source of cash deposit in the bank account. The Assessing Officer in the scrutiny assessment has made the addition of Rs.2,17,54,080/- on account of the entire deposit made in the bank account and further, the Assessing Officer has also made the addition of Rs.2,20,45,610/- as business income by treating the entire receipts as business income of the assessee instead of profit element which is also beyond the scope of limited scrutiny. The learned Authorised Representative of the Assessee has referred to the CBDT instruction dated 28.11.2018 as well as 20.08.2018 and submitted that the CBDT has clearly laid down the guidelines and instructions for cases of tax evasion based on the information provided by the law enforcement/ intelligence/regulatory authority can be examined during the course of assessment proceedings in such limited scrutiny cases with prior administrative approval of the concerned Pr. CIT/ CIT. Thus, the learned Authorised Representative of the Assessee has submitted that if the Assessing Officer received any information from the law enforcement/intelligence/ regulatory authority, he can conduct an enquiry in respect of the issue after prior administrative approval of the Competent Authority. However, in the case of the assessee there is no such information received by the Assessing Officer during the course of assessment proceedings from the law enforcement/ intelligence/regulatory authority for expanding the scope of enquiry or converting the limited scrutiny to complete scrutiny. Thus, even under the latest instruction of the CBDT dated 28.11.2018, the Assessing Officer cannot expand the scope of enquiry without satisfaction of the conditions as laid down by the CBDT. Therefore, the learned Authorised Representative of the Assessee has submitted that travelling beyond the scope of limited scrutiny by the Assessing Officer renders the assessment order illegal and liable to be set aside. In support of his contention, he has relied upon the Order of ITAT, Pune Bench in the case of Mr. Anil Jagannath Kedar vs. ITO, Ward-1(2), Solapur in ITA.No.567/Pun./2024, dated 26.06.2025 as well as decision of ITAT, Bangalore Bench in the case of Anantula Vijay Mohan, Hyderabad vs. DCIT, Circle-6(1)(1), Bangalore in ITA.Nos.2059 & 2060/ Bang./2024 dated 07.05.2025. He has also relied upon the Order of ITAT, Chennai Bench, Chennai in the case of Aadarsh Surana, Chennai vs. DCIT, Corporate Circle-1(1), Chennai in ITA.No.1840/Chny./2025, dated 15.12.2025.

7.1. Thus, the learned Authorised Representative of the Assessee has submitted that the assessment order passed by the Assessing Officer without jurisdiction to examine the issue beyond the limited scrutiny is invalid and liable to be set aside.

8. On the other hand, the learned DR has submitted that as per the information available on record no approval has been taken by the Assessing Officer to enquire about the bank credits of the assessee. However, he has submitted that since the case of the assessee was selected for limited scrutiny on the issue of cash deposit during the year therefore, the Assessing Officer ought to have examine the bank account statement of the assessee and found that there are other deposits in the bank account apart from cash deposits which are falling under the scope of the issue taken up for scrutiny. Thus, the learned DR has submitted that the only logical inference can be taken that for meaningful verification of the issue taken up under the scrutiny the Assessing Officer was required to analyze complete pattern of bank account credits which has resulted other deposits in the bank account apart from the cash deposits and therefore, the same are not separate subject matter or issue but arising from the same issue/subject matter taken up for scrutiny by the Assessing Officer. Therefore, there was no requirement for the Assessing Officer to take the approval of the Competent Authority for examining the issue and consequently framing the assessment u/sec.143(3) of the Act. Thus, the learned DR submitted that there is no illegality in the Order passed by the Assessing Officer when the transactions in the bank account of the assessee are considered and examined by the Assessing Officer while framing the assessment.

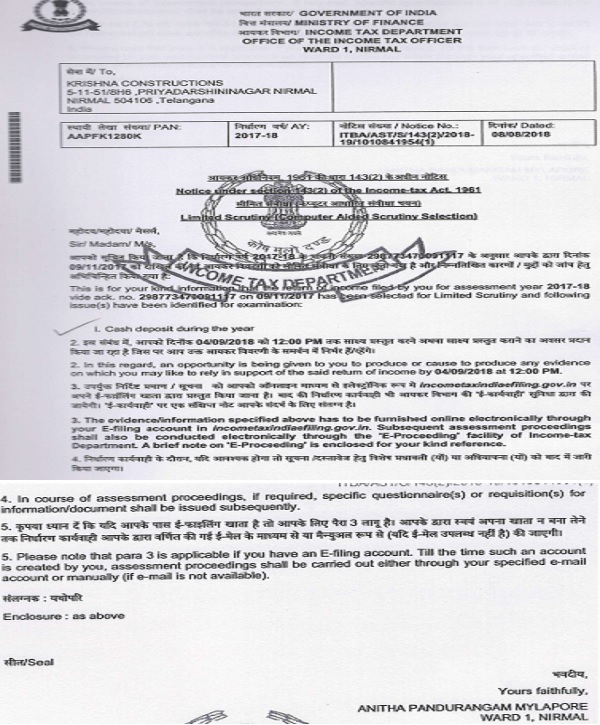

9. We have considered the rival submissions as well as relevant material on record. There is no dispute that the return of income of the assessee was taken up for limited scrutiny under CASS for examination of the issue of cash deposits during the year. These facts are manifest from the notice issued by the Assessing Officer u/sec.143(2) of the Act dated 08.08.2018 as under:

9.1. The department has not disputed that the assessee’s case was selected for limited scrutiny under CASS for examination of the issue of cash deposit during the year. While passing the assessment order u/sec.143(3) of the Act dated 29.12.2019 the Assessing Officer has taken up the other issues regarding the entire credits/deposits in the bank account of the assessee which are in the nature of deposits made by the partners and finally made an addition of Rs.2,20,45,610/- as under:

“Further, is seen that as the gross receipts amount to Rs.2,20,45,610/ the assessee has to maintain the books of account and get the same audited as per the provisions of sec.44AB of the Income-tax Act. However it is seen that the assessee has not filed Form 3CB/ 3CD thereby violated the provisions of Sec.44AB. As the assessee has neither maintained any books of account nor got them audited as per the provisions of Section 44AB of the Act, the assessee is liable for penalty for noncompliance to the provisions of Sec.44AA and 44AB of the Act and the same are initiated separately. The assessee though having turnover above Rs.1 crore has failed to file the Form 3CB and 3CD report there attracting penal proceedings, hence initiated separately.”

9.2. Thus, the Assessing Officer treated the gross receipts as undisclosed business income of the assessee which are mainly comprising of the deposits made by the partners of the assessee firm which were declared as income in their individual capacity and therefore, the transactions of deposits/credits made by the partners from their bank account to the assessee firm account is clearly beyond the scope of limited scrutiny on the issue of cash deposit during the year. The CBDT has issued instructions from time to time regarding the return selected for scrutiny under CASS as well as compulsory manual scrutiny. The CBDT issued instruction vide File No.225/157/2017 dated 23.06.2017 for issuing notice u/sec.143(2) of the Act prescribing the revised Form of the notice u/sec.143(2) in respect of the case selected for limited scrutiny under CASS, complete scrutiny under CASS and compulsory manual scrutiny. Therefore, there are 03 Forms of notices which are prescribed by the CBDT in the revised Form. The relevant part of the said CBDT instruction and the revised Form/Format for issuing notice u/sec.143(2) in case of limited scrutiny under CASS are as under:

F.No. 225/157/2017/ITAII

Government of India

Ministry of Finance

Department of Revenue (CBDT)

North Block, New Delhi, dated the 23rd of June. 2017

To

All Pr. CCsIT/Pr. CCIT(International-tax)/CCIT(Exemptions)/Pr. DsGIT

Sir/Madam

Subject. – Issue of notices under section 143(2) of Income-tax Act. 1961 in revised format-regd.-

With reference to the above, I am directed to state that Central Board of Direct Taxes has decided to modify format of notice(s) issued under section 143(2) of the Income-tax Act which intimate the concerned assesse about selection of his/her case for scrutiny. This has become necessary in view of Board’s decision to utilise ‘E-Proceeding’ facility for electronic conduct of assessment proceedings in a widespread manner from this financial year.

2. The three formats of notice(s) are:

-

- Limited Scrutiny (Computer Aided Scrutiny Selection)

- Complete Scrutiny (Computer Aided Scrutiny Selection)

- Compulsory Manual Scrutiny

The revised format of 143(2) notice(s) with a note on benefits & Procedures of ‘E-Proceeding’ facility are enclosed for information of the field authorities.

3. I am further directed to state that all scrutiny notices under section 143(2) of the Act, shall henceforth, be issued in these revised formats only. The Systems Directorate is effecting necessary changes In the ITBA module in this regard.

4. The above may be brought to the notice of all for necessary compliance. Enclosures(s): as above

(Rohit Garg)

Director-ITA.II, CBDT

Copy to:

i. Chairman, CBDT and all Members, CBDT

ii. CIT, Data base Cell for uploading on Departmental Website

Limited Scrutiny (Computer Aided Scrutiny Selection)

Notice under Section 143(21 of the Income-tax Act, 1961

PAN No ………………………………………………………………………………………………….. Dated: ………….

To

Sir/Madam

This is for your kind information that the return of income for Assessment Year………………………………. filed vide ack no …………………………………. on has been selected for Scrutiny. Following issue(s) have been identified for examination:

2. In view of the above, I would like to give you an opportunity to produce any evidence/information which you feel is necessary in support of the said return of income on or before…………..

3. The above mentioned evidence/information is to be furnished online electronically in ‘E-Proceeding’ facility through your account in e-Filing website of Income-tax Department. Further proceedings shall also be conducted electronically (*). A brief note on salient features of ‘E-Proceeding’ is enclosed.

4. In case you do not wish to produce any evidence/information, as mentioned in para 2, you are requested to intimate the same electronically on or before………..

5. Specific questionnaires/requisition of information or documents would be sent subsequently, if required.

6. Para(s) (2) to (4) are applicable if you have an account in e-Filing website of Income-tax Department. Till such an account is created by you, assessment proceedings shall be carried out either through your e-mail account or manually (if e-mail is not available).

(*) Subject to exceptions as per the enclosed note

Yours faithfully,

Seal

(Name of the Assessing Officer)

(Designation)

(Telephone No./Fax No.)

(E-mail ID)

9.3. Therefore, the CBDT has even specified the Format for issuing notice u/sec.143(2) in respect of different types of scrutiny undertaken by the Assessing Officer. The CBDT has also expressed its concern about the instances where the Assessing Officers are routinely calling for information which is not relevant for the enquiry into the issue taken up for limited scrutiny and accordingly, in the instruction no.7/2024 dated 26.09.2024 the CBDT directed that the cases selected for scrutiny on the basis of AIR Data/CIB information, the scope of enquiry should be limited to verification of the particular aspect only. It was further clarified that the Assessing Officer shall confine the questionnaire and subsequent enquiry or verification only to the specified points on the basis of which the particular return has been selected for scrutiny. In the cases where during the course of assessment proceedings it is found that there is a potential escapement of income, the cases selected under CASS require substantial verification, the case may be taken up for comprehensive scrutiny with the approval of Pr. CIT/DIT in writing after being satisfied about the merits of the issue necessitates wider and detailed scrutiny in the cases and such cases so taken up for detailed scrutiny shall be monitored by the JCIT/Addl. CIT concerned. Further, the CBDT issued Instruction 20/2025 dated 29.12.2015 which also reiterates that the Assessing Officer should confine to the issue which is taken up under the limited scrutiny cases and only if during the assessment proceedings in the limited scrutiny, it comes to the notice of the Assessing Officer that there is a potential escapement of income, he shall with prior approval of the Competent Authority expand the scope of enquiry/scrutiny from limited to complete scrutiny. For the year under consideration, the CBDT issued Instruction F.225/402/2018/ITA.II dated 28.11.2018 which reads as under :

“F.No. 225/ 402/ 2018/ ITA.II

Government of India

Ministry of Finance

Department of Revenue (CBDT)

North Block, New Delhi, the 28 of November, 2018

To

All Principal Chief-Commissioners of Income-tax/All Principal Director-Generals of Income-tax

Sir/ Madam,

Subject: Scope of enquiry in Limited Scrutiny cases selected under CASS cycles 2017 and 2018 in the context of information provided by any law enforcement/intelligence/regulatory authority or agency regd.

Under CASS cycles 2017 and 2018, some of the cases were selected for scrutiny as a “Limited Scrutiny case. In ‘Limited Scrutiny cases, Assessing Officer cannot travel beyond the issue(s) for which the case was selected. The idea behind such a stipulation is to enforce checks and balances upon powers of an Assessing Officer to do fishing and roving enquiries in cases under “Limited Scrutiny.

2. In this regard, several representations have been received in the Board from the field authorities that in several cases under “Limited Scrutiny, information pointing out specific tax-evasion for the relevant year, given by any law-enforcement/ intelligence/ regulatory authority or agency is available with the concerned Assessing Officer, however, in view of the restrictive nature of enquiry/ investigation which can be made in “Limited Scrutiny’ cases, the same presently cannot be acted upon.

3. The matter has been considered by the Board. In order to enable proper enquiry/ investigation in pending “Limited Scrutiny cases which were selected through CASS cycles of 2017 and 2018, where credible material or information has been/ is provided by any law enforcement/ intelligence/ regulatory authority or agency regarding tax-evasion by an assessee, it has been decided by the Board that issues arising from such information can also be examined during the course of conduct of assessment proceedings in such “Limited Scrutiny cases with prior administrative approval of the concerned Pr. CIT/ CIT.

4. It is pertinent to mention that unlike CASS 2015 and 2016 cycles, where consideration of any additional issue lead to the conversion of case to ‘Complete Scrutiny as laid down in Instruction No. 5/2016 dated 14.07.16, the pending “Limited Scrutiny cases of CASS 2017 and 2018 cycles would not be taken up for ‘Complete Scrutiny’ as the present directive is only to facilitate consideration of those issues wherein specific Information of tax-evasion has been furnished by any law-enforcement/ intelligence/ regulatory authority or agency. Therefore, in such ‘Limited Scrutiny cases, Assessing Officer shall not expand the scope of enquiry/ investigation beyond the issue(s) on which the case was flagged for ‘Limited Scrutiny & issue arising from nature of information mentioned in para 2 and 3, above.

5. The following procedure shall be adopted while examining the additional issue:

i. The Assessing Officer shall duly record the reasons for expanding the scope of ‘Limited Scrutiny to the extent mentioned in para 2 and 3, above;

ii. The same shall be placed before the Pr. CIT/ CIT concerned and upon his approval, further issue can be considered during the assessment proceeding;

iii. The Assessing Officer shall issue an intimation to the assessee concerned that additional issue would also be considered during the course of pending assessment proceeding;

iv. To ensure proper monitoring in these cases, provisions of section 144A of the Income-tax Act, 1961 may be Invoked in suitable cases. Further, to prevent fishing and roving enquiries in these cases, it is desirable that these cases are invariably picked up for Review/ Inspection by the administrative authorities.

6. The above directive shall be applicable from the date of its issue and shall apply to the pending “Limited Scrutiny cases which were selected under the CASS 2017 and 2018 cycles. It is reiterated that the grounds mentioned in para 3 above are the only grounds on which a ‘Limited Scrutiny case of CASS 2017 and 2018 cycles can be expanded in its scope and that too only to the extent of the issues referred to by the law-enforcement/ intelligence/ regulatory authority or agency.

7. It may be brought to the notice of all for necessary compliance.

Sd/ -(Rohit Garg)

Director (ITA.II), CBDT

Copy to:-

-

- Chairman, CBDT & All Members, CBDT

- CIT (Database Cell) for uploading on the departmental website.”

9.4. Thus, in para no.6 of the instruction, the CBDT again reiterated the directions that the limited scrutiny under CASS can be expanded its scope only to the extent of issue referred by law enforcement/intelligence/regulatory authority or agency with prior approval of the Competent Authority. In the case in hand, undisputedly, there is no material or information provided by the law enforcement/ intelligence/regulatory authority or agency. Further, the Assessing Officer has not taken the approval for expanding the scope of limited scrutiny. Thus, it is a clear case of breaching the scope of limited scrutiny under CASS by the Assessing Officer while passing the impugned order and making the additions which are beyond the scope of the limited scrutiny taken up for examination of the issue of cash deposit in the bank during the year. The Pune Bench of the Tribunal in the case of Mr. Anil Jagannath Kedar vs. ITO, Ward-1(2), Solapur (supra), has considered an identical issue in Para nos.3 to 6 as under:

“Findings & Analysis:

3. We have heard both the parties and perused the records. In this case, Assessee had filed Return of Income electronically on 30.11.2017, declaring total income at Rs.8,66,840/ – for A. Y.2017-18. Assessee’s case was selected for scrutiny. In the assessment order, Assessing Officer has mentioned as under:

“The case was selected for scrutiny under CASS with the reason that “Large cash deposits in bank account(s) during the year and other income in Part A P&L of ITR utilized as turnover.” A System generated notice u/ s 143(2) of the Income Tax Act, 1961, was issued on 21.08.2018 and served on assessee’s registered E-mail ID. Further notice under Sec. 142(1) of the Act along with questionnaire was issued on 14.03.2019 and served on the assessee.”

3.1. Thus, as per the assessment order, case was selected for two reasons.

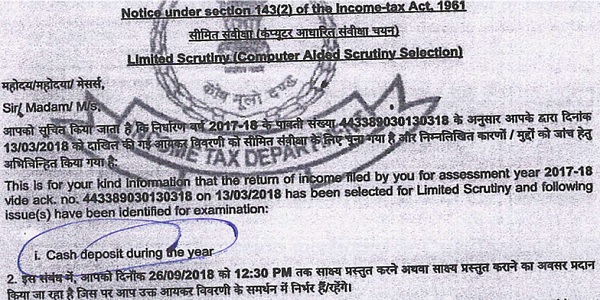

3.2. However, Id.AR invited our attention to the notice u/ s.143(2) dated 21.08.2018(copy was filed by AR), wherein the reasons mentioned is limited scrutiny for verification of cash deposits during the year. The relevant part of the notice u/ s.143(2) is scanned and reproduced as under:

3.3. Thus, it is clear from the Notice u/ s. 143(2) that Assessee’s case was selected for limited scrutiny for examination of cash deposits during the year. We have studied the assessment order, nowhere Assessing Officer has discussed about the cash deposits made by Assessee during the year. Rather, on reading the assessment order, we could not find out the exact amount of cash deposits during the year, Id. DR for the Revenue also could not find out the same from the assessment order. The entire discussion is about Assessee’s business, his turnover and applicability of Section 44AD. The final sentence of the assessment order determining the income is as under:

“As, the assessee had not shown the trading income and not submitted any explanation on the same, therefore, the trading income of the assessee is determined @ 8% of the trading turnover of Rs.2,59,08,018/-which comes to Rs.20,72,641/-. Hence, the addition of Rs.20,72,641/-is made to the total income of the assessee, on account of business or profession.”

3.4. Thus, the Assessing Officer has made addition outside the scope of limited scrutiny. Though in the assessment order, one more reason is mentioned i.e. other income in P & L Account, however, in the notice u/ s.143(2), the reason mentioned is Cash Deposits. The Notice u/ s. 143(2) is system generated, therefore, it has to be taken as Correct. No evidence has been brought by ld.DR for the Revenue, on record to rebut the reasons appearing in the notice u/ s.143(2) of the Act. In these facts and circumstances, we are convinced that Assessee’s case was selected for limited scrutiny for examination of cash deposits during the year. However, Assessing Officer has travelled outside the scope of limited scrutiny. The Central Board of Direct Taxes had issued Instruction No.05/ 2016 dated 14.07.2016 regarding Scope of Limited Scrutiny. Similarly, CBDT had issued a letter dated 20.11.2018 explaining Scope of Enquiry in Limited Scrutiny. The Instructions issued by CBDT are binding on the Assessing Officer.

4. The Hon’ble Calcutta High Court in the decision of PCIT Vs. Weilburger Coatings (India) (P.) Ltd., [2023] 155 taxmann.com 580 (Calcutta) dated 11.10.2023 has held as under:

“4. The revenue has raised the following substantial questions of law for consideration:-

(a) Whether in the facts and circumstances of the case and in law the Learned Tribunal has committed substantial error in law in deleting the disallowance of carry forward of losses of earlier years ?

(b) Whether the Learned Tribunal has substantially erred in law in holding that the Assessing Officer exceeded his jurisdiction in enquiring into those issues which were beyond the scope of limited scrutiny, without taking into consideration the fact that the claim of the assessee pertaining to carried forward losses was inadmissible since the beginning itself and therefore the Assessing Officer was justified in disallowing the same without converting the case into complete scrutiny?

5. We have heard Mr. Amit Sharma, learned standing Counsel appearing for the appellant and Mr. Abhratosh Majumder, learned senior Advocate for the respondent.

6. The short issue which falls for consideration in the instant case is whether the Assessing Officer exceeded his jurisdiction in completing the assessment on grounds which were not subject matter of the limited scrutiny.

7. The contention of the learned standing Counsel for the appellant is that the assessee was put on notice on that particular issue by the Assessing Officer, the assessee participated in the proceedings and thereafter the assessment was completed by order dated 27th December, 2017 under Section 143(3) of the Act. The assessee carried the matter on appeal before the Commissioner of Income Tax (Appeals) 5 [CIT(A)] and the appeal was contested on merits and the appeal stood partly allowed on certain issues by order dated 14th January, 2019. The assessee being aggrieved by the disallowed portion of the order passed by the CIT(A) preferred appeal before the Tribunal and in the appeal additional ground was raised contending that the action of the CIT(A) in confirming the action of the Assessing Officer in making additions in respect of issues not mentioned in limited scrutiny were beyond jurisdiction of the Assessing Officer as the scrutiny assessment was selected for limited scrutiny under Section 143(2) and not complete scrutiny. The Department objected to the additional ground which were raised by the appellant before the Tribunal. However, the learned Tribunal overruled the said objection holding that the issue is jurisdictional issue and can be raised by the assessee at any point of time. This finding of the learned Tribunal is well justified and in accordance with the settled legal principle. Thereafter the learned Tribunal has re-examined the factual position and found that the issue which was decided by the Assessing Officer was not part of the limited scrutiny for which the assessment was directed to be scrutinised. That apart, the learned Tribunal has also taken note of the CBDT Instruction No.5 of 2016 to hold that the Assessing Officer has exceeded his jurisdiction.

8. Learned senior Counsel for the respondent/assessee has placed before us another Instruction issued by the CBDT dated 30th November, 2017, being F.No. DGIT(Vig)/HQ/SI/2017-18, wherein the CBDT has noted instances where some of the Assessing Officer were travelling beyond the issues while making assessment in limited scrutiny cases by initiating inquiries on new issue without complying with mandatory requirements of the relevant CBDT Instruction dated 26.09.2014, 29.12.2015 and 14.07.2016. It has been stated that these instances have been viewed seriously by the CBDT and in one case the Central Inspection Team of the CBDT was tasked with examination of assessment records on receipt of allegations of several irregularities and among other irregularities it was found that no reasons had been recorded for expanding the scope of limited scrutiny, no approval was taken from the PCIT for conversion of the limited scrutiny case to a complete scrutiny case and the order sheet was maintained very perfunctorily. Further, the CBDT has recorded that this gave rise to a very strong suspicion of mala fide intentions and the Officer concerned has been placed under suspension. Therefore, it was reiterated that the Assessing Officer should abide by the Instructions of CBDT while completing limited scrutiny assessment and should be scrupulous about maintenance of note sheets in assessment folders.

9. Thus, considering these aspects, we are of the view that the learned Tribunal rightly allowed the assessee’ s appeal on the said issue. This Court had an occasion to consider a somewhat similar issue in the case of Pr. CIT v. Sukhdham Infrastructures LLP, in [ITAT No. 164 of 2023, dated 14-8-2023]. In the said case an identical contention as raised before us was raised stating that at best the action of the Assessing Officer could be construed to be an irregularity. While considering such a contention in Sukhdham Infrastructures LLP the Court rejected the same with the following observation :-

“While considering the said issue, the Hon’ ble Supreme Court noted the distinction between the statutes affecting rights and those affecting mere procedure. The revenue cannot rely upon the said decision as the scheme of assessment as provided under Section 143 of the Act is a complete code by itself and the circumstances under which the power under sub-section (2) of Section 143 could be invoked has been clearly spelt out and on a reading of subsection (3) of Section 143, it s evidently clear that on the day specified in the notice issued under sub-section (2), or as soon afterwards as may be, after hearing such evidence as the assessee may produce and such other evidence as the Assessing Officer may require on specified points, and after taking into account all relevant material which he has gathered, the Assessing Officer shall, by an order in writing, make an assessment of the total income or loss of the assessee, and determine the sum payable by him or refund of any amount due to him on the basis of such assessment.

Therefore, the question of part of the provision being procedural is an incorrect interpretation of the scheme provided under Section 143 of the Act. Further, as noted above, the CIT (A) has examined the merits of the matter and after taking note of the facts granted relief to the assessee to the extent indicated therein. ‘Thus, for the above reasons, we find that the revenue has not made out any case for interference of the order passed by the Tribunal. Accordingly, the appeal fails and is dismissed.

The substantial questions of law are answered against the revenue.

The application for stay being GA 1 of 2023 is also dismissed.”

In the light of the above, no grounds have been made out to interfere with the order passed by the Tribunal.

10. Accordingly, the appeal fails and is dismissed.

11. The substantial questions of law are answered against the revenue.”

5. The above-mentioned decision of Hon’ble Calcutta High Court was followed by Patna Bench of ITAT in the case of Narendra Kuamr Singh Vs. ITO in ITA No.468/ PAT/ 2024 A.Y.2017-18, dated 18.11.2024. The assessment year and facts are identical to the case of the assessee. The relevant Paragraphs 7, 8 and 9 of the order of ITAT Patna Bench are reproduced here as under:

“7. After hearing the rival contentions and perusing the material available on record including the case law cited before us as well as Circular No. 3/2019 issued by the CBDT, we observe that undisputedly the case of the assessee was selected for scrutiny for examination and verification of large cash deposits during the impugned financial year. However, upon verification of facts by the Id. Assessing Officer during the course of assessment proceedings, the ld. Assessing Officer did not make any addition after verification of Bank accounts towards large cash deposits. However, he made two additions of Rs.1,02,17,061/-on peak credit of unexplained deposits which were not on account of cash deposits and second in respect of under misreporting of income of Rs.34,43,814/-as per Form 26AS. It is pertinent to state that during the course of hearing, Id. Assessing Officer noticed that the assessee has deposited Rs.1,73,10,349/- in Canara Bank account out of which cash deposit was of Rs.4,01,390/- whereas credit entries of Rs.6,26,597/- in ICICI Bank account were there out of which cash deposit was of Rs.96,565/- during the financial year. We note that the assessee did not comply with the show-cause notice issued by the ld. Assessing Officer and finally Id. Assessing Officer framed the assessment under section 144 of the Act vide order dated 19.12.2019 making two additions as stated above. Therefore, it is abundantly clear that the additions made by the Id. Assessing Officer were not in respect of the issue, which was the subject matter of the limited scrutiny as is apparent from the notice issued under section 143(2) of the Act dated 10.08.2018 and the ld. Assessing Officer passed the assessment order by making the above said additions without converting the limited scrutiny into complete scrutiny in terms of Circular issued by CBDT bearing No. 3/2017 dated 21.02.2019. In our opinion, the said additions made by the ld. Assessing Officer are without jurisdiction and cannot be sustained. The assessee finds support from the decision of the Hon’ble Jurisdictional High Court in the case of PCIT vs. Weilburger Coatings (India) Pvt. Limited [2023] 155 taxmann.com 580 (Calcutta), wherein Hon’ble Court has held as under:-

“The assessee has placed Instruction issued by the CBDT dated 30-11-2017, being F. No. DGIT(Vig)/HQ/S1/2017-18, wherein the CBDT has noted instances where some of the Assessing Officer were travelling beyond the issues while making assessment in limited scrutiny cases by initiating inquiries on new issue without complying with mandatory requirements of the relevant CBLYT Instruction dated 26-92014, 29-12-2015 and 14-7-2016 It has been stated that these instances have been viewed seriously by the CBDT and in one case the Central Inspection Team of the CBDT was tasked with examination of assessment records on receipt of allegations of several irregularities and among other irregularities it was found that no reasons had been recorded for expanding the scope of limited scrutiny, no approval was taken from the Principal Commissioner for conversion of the limited scrutiny case to a complete scrutiny case and the order sheet wat maintained very perfunctorily. Further, the CBDT has recorded that this gave rise to a very strong suspicion of mala fide intentions and the Officer concerned has been placed under suspension. Therefore, it was reiterated that the Assessing Officer should abide by the Instructions of CBDT while completing limited scrutiny assessment and should be scrupulous about maintenance of note sheets in assessment folders. Thus, considering these aspects, it is viewed that the Tribunal rightly allowed the assessee’ s oppeal on the said issue.

8. Similarly, the above issue is also covered by the decision of the Coordinate Bench in the case of Vudatha Vani Rao -vs. Income Tax Officer [2024] 159 com 1394 (Visakhapatnam – Trib.), wherein the issue has been decided in favour of the assessee by holding that the additions made in the assessment order, which were not subject matter of the limited scrutiny, are beyond the jurisdiction of the Id. Assessing Officer and therefore, have to be deleted.

9. Considering the above facts and in the light of above judicial precedences, we are inclined to set aside the order of Id. CIT(Appeals) and direct the Id. Assessing Officer to delete the additions.”

6. We have already discussed the facts of the case. No contrary decision of Hon’ble Jurisdictional High Court has been brought to our notice. Therefore, respectfully following the Hon’ble Calcutta High Court, ITAT Patna Bench and ITAT Pune Bench(supra), we direct the Assessing Officer to delete the addition. Accordingly. Legal Ground No.1 raised by the Assessee is allowed.”

9.5. Similar view has been taken by the Bangalore Bench of the Tribunal in the case of Anantula Vijay Mohan, Hyderabad vs. DCIT, Circle-6(1)(1), Bangalore (supra), in Para nos.9 to 9.12 as under:

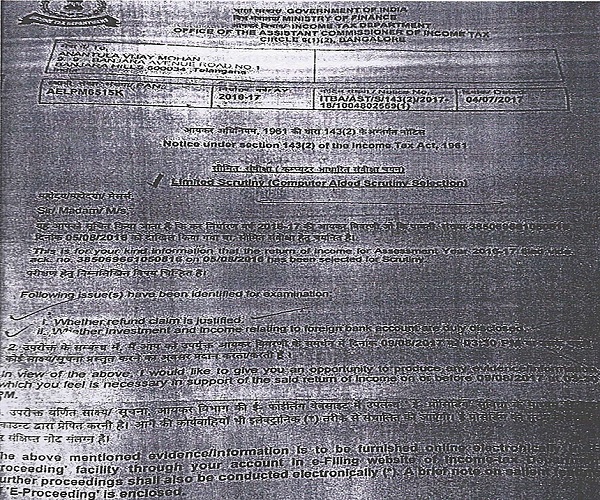

“9. We have heard the rival submissions and perused the materials available on record. It is undisputed fact that the case of the assessee was selected for limited scrutiny under the CASS by issuing notice u/ s 143(2) of the Act dated 4.7.2017 which are reproduced below for the sake of convenience and brevity:

9.1. On going through the above, we take a note of the fact that the case was identified for limited scrutiny (CASS) for the examination of the following two issues only:

i. Whether refund claim is justified ?

ii. Whether investment and income relating to foreign bank account are duly disclosed?

9.2. However, on going through the assessment order passed u/ s 143(3) of the Act dated 12.12.2018, we take a note of the fact that on the ground of artificial arrangement to generate capital loss, The AO has disallowed the capital loss of Rs.20,24,90,717/ – and further business loss of Rs.44,91,482/ is determined by allowing the assessee to set off against capital gain from acquisition of smartplay startup by aricent, which in our opinion was not identified for examination under the limited scrutiny. The sole basis of the assessment is completely based on the AO’s presumption that there is a artificial arrangement to generate capital loss whereas the case was selected for the examination of whether refund claim is justified & whether investment and income relating to foreign bank account are duly disclosed. Further, it is also an admitted fact that the AO had also failed to convert the limited scrutiny to complete scrutiny by following the due procedures as directed in various instructions/ orders issued by the CBDT which is binding on him. On going through the various instructions/ order issued by the CBDT regarding scope of the limited scrutiny under CASS, we take a note of the important directions as below:

9.3 The instruction no.20/2015 dated 29.12.2015 clarifies the scope and applicability of the limited scrutiny cases. The procedure for handling “limited scrutiny case clarified are as under:

a) In “limited scrutiny cases, the reasons/issues shall be forthwith communicated to the assessee concerned.

b) The questionnaire under section 142(1) of the Act in “limited scrutiny cases shall remain confined only to the specific reasons/ issues for which case has been picked up for scrutiny. Further, the scope of enquiry shall be restricted to the “limited scrutiny” issues.

c) These cases shall be completed expeditiously in a limited number of hearings.

d) During the course of assessment proceedings in “limited scrutiny cases, if it comes to the notice of the AO that there is potential escapement of income exceeding Rs.5 lakhs (for Metro Rs.10 lakhs) requiring substantial verification on any other issues then, the case may be taken up for complete scrutiny with the approval of the Principal CIT/ CIT concerned.

e) The Principal CIT/ CIT shall accord the approval in writing after being satisfied about the merits of the issue necessitating “complete scrutiny”.

f) Further, such cases shall be monitored by the Range Head concerned and the procedure indicated at point No.(a), (b) & (c) above shall no longer remain binding in such cases.

9.4. Further the instruction No. 5/2016 dated 14.7.2016 state that in order to ensure that maximum objectivity is maintained in converting a case falling under “limited scrutiny” into a “complete scrutiny” case, the AO while forming the reasonable view would ensure that:

i) There exist credible material or information available on record for forming such view.

ii) This reasonable view should not be based on mere suspicion, conjecture or unreliable source and

iii) There must be direct nexus between the available material and formation of such view.

9.5. In the said instruction, it is further clarified that in cases under “limited scrutiny”, the scrutiny assessment proceeding would be confined only to issues under “limited scrutiny and questionnaires, inquiry, investigation, etc. would be restricted to such issues.

9.6. Further, the CBDT vide F.No.225/ 402/ 2018/ ‘TAX dated 28.11.2018 has again reiterated that in “limited scrutiny” cases the AO shall not expand the scope of enquiry/ investigation beyond the issues on which the case was flagged for “limited scrutiny”. Further, it is also provided that the scope of “limited scrutiny” may be expanded only if the matter is placed before the Id. PCIT/ CIT for his administrative approval and subject to monitory limits as per earlier instruction dated 29.12.2015.

9.7. The CBDT vide F.No.225/ 402/ 2018/ ITA.II dated 28.11.2018 also directed to adopt the following procedures while examining the additional issue-

i) The AO shall duly record the reasons for expanding the scope of Limited Scrutiny’ to the extent where credible material or information has been /is provided by any law-enforcement/ intelligence/ regulatory authority or agency regarding tax-evasion by an assessee.

ii) The same shall be placed before the Pr. CIT/ CIT concerned and upon his approval, further issue can be considered during the assessment proceeding;

iii) The AO shall issue an intimation to the assessee concerned that additional issue would also be considered during the course of pending assessment proceeding;

iv) To ensure proper monitoring in these cases, provisions of section 144A of the Act may be invoked in suitable cases. Further, to prevent fishing and roving enquiries in these cases, it is desirable that these cases are invariably picked up for review/ inspection by the administrative authority.

9.8. In the present case, admittedly the same AO who had issued the notice u/s 143(2) of the Act, while issuing notice u/s 142(1) of the Act dated 31.5.2018 had asked to submit details only with regard to high ratio of refund to TDS (part B-TTI of ITR) and large balance in foreign bank account (Schedule FA of ITR) along with the copy of Return, Computation of Income, Audited accounts & report as identified for the examination under limited scrutiny.’ However, after the change in incumbency, on going through the notice u/s 142 (1) of the Act dated 5.10.2018 issued by the new AO, we find that AO has asked detailed questionnaire relating to number of shares purchased and sold along with the details of bonus shares and cost of acquisition as well as the details of dividend received, which in our view was not the issues identified for examination under the notice u/s 143(2) of the Act under the “limited scrutiny”. We are further of the opinion that the AO has over stepped his jurisdiction without duly recording the reasons for expanding the scope of Limited Scrutiny’. The same also not placed before the Pr. CIT/ CIT concerned for his approval & the assessee had also not been intimated that additional issue would also be considered during the course of pending assessment proceeding. If we consider the argument of the Id. D.R. that since the refund arises out of all the items included in “computation of income”, the AO can verify all the heads of income because of which refund results, then in our view, it will completely frustrate the very objective of “limited scrutiny”.

9.9. We are of the considered opinion that when the tax authorities are scrutinizing/ examining whether refund claimed is justified, they should confined themselves whether the gross receipts on which the TDS credit is sought has been declared in the return or not, Whether TDS claimed are reflecting in the Form 26AS of not, whether the assessee had actually paid any excess advance tax or not & the reasons for claiming the refund. In the present case, the AO completed the assessment on the sole presumption that that the assessee has made artificial arrangements to generate the capital loss and accordingly the claim of capital loss amounting to Rs.20,24,90,717/ – was disallowed & business loss of Rs.44,91,482 was determined which in our opinion are not identified for the limited examination u/s 143(2) of the Act. Under these circumstances, in our opinion, even if some other issues comes to the notice of AO during the course of assessment proceedings, he cannot make any other addition/ disallowance without obtaining prior approval from concerned PCIT/ CIT as per the instruction issued by the CBDT cited (supra). In our opinion, the AO has exceeded the jurisdiction by calling for details and carrying out inquiries by issuing notice u/s 142(1) of the Act dated 5.10.2018.

9.10. Considering the facts of assessee’s case and also the CBDT instruction cited (supra) we are of the considered view that the AO has exceeded his jurisdiction in inquiring into those issues which are beyond the scope of “limited scrutiny” which is clear violation of mandate given by the CBDT in the above instructions/ orders which are binding on the AO and accordingly without jurisdiction & bad in law. We are of the view that CBDT has specifically clarified that in a “limited scrutiny”, the scope of enquiry shall be restricted to the “limited scrutiny” issues. It will be confined only to issues and questionnaire, inquiry, investigation, etc. would be restricted to such issues in the “limited scrutiny”.

9.11. In view of the above, the bench is of considered opinion that the very exercise of jurisdiction to examine/ scrutinize the transaction in BEL shares are not covered in the any of the issues identified for the examination under the “limited scrutiny”. The examination of refund claim in a limited scrutiny cannot be construed as giving jurisdiction to a complete scrutiny. The AO has expanded the scope of “limited scrutiny” without following due procedure as directed under various instructions/ orders. Therefore we are inclined to hold that the AO has exceeded his jurisdiction in disallowing the capital loss of Rs.20,24,90,717/ – and further determining the business loss of Rs.44,91,482/ – by allowing the assessee to set off against capital gain from acquisition of smart play startup by aricent and accordingly we set a-side the order of the AO being without jurisdiction & bad in law.

9.12. As the additional grounds raised by the assessee are allowed and accordingly other ground of appeal on merits of the case are not adjudicated and are kept open.”

9.6. Thus, the Tribunal has taken a consistent view that the order passed by the Assessing Officer travelling beyond the scope of limited scrutiny without prior approval of the Competent Authority is void abinitio and liable to be set aside. The Chennai Benches of the Tribunal in the case of Aadarsh Surana, Chennai vs. DCIT, Corporate Circle-1(1), Chennai (supra), has again considered an identical issue in Para nos.73 to 101 as under:

“73. We have considered the additional ground raised by the assessee. whereby the validity of the assessment order itself has been challenged. On perusal of the records, it is observed that the said ground was duly raised by the assessee before the Ld.CIT(A) and the Ld.CIT(A) has also adjudicated upon the same. However, due to inadvertence, the said ground was not specifically incorporated in the grounds of appeal filed by the assessee before this Tribunal. It is further noted that the additional ground so raised is purely jurisdictional in nature and goes to the very root of the matter. Admittedly, the facts necessary for adjudication of the said ground are already borne out from the material available on record and do not require any further investigation of facts. Therefore, no prejudice would be caused to the Revenue by admitting the said additional ground at this stage. In view of the settled legal position and respectfully following the ratio laid down by the Hon’ble Supreme Court in the case of National Thermal Power Co. Ltd. v. CIT (1998) 229 ITR 383 (SC), wherein it has been held that a pure question of law, which does not require investigation into fresh facts and arises from the facts already on record, can be raised at any stage of the proceedings, we are of the considered opinion that the additional ground raised by the assessee deserves to be admitted. Accordingly, the additional ground raised by the assessee is admitted for adjudication.

74. Admittedly, for the impugned assessment year, the case of the assessee was selected for limited scrutiny with the specific purpose of examining the following issues:

i. expenses incurred for earning exempt income; and

ii. share capital/ capital.

75. It is a matter of record that, while completing the assessment, the AO proceeded to make three additions, namely:

a. addition on account of unexplained cash credits u/ s. 68 of the Act;

b. addition on account of unexplained investment u/ s.69 of the Act; and

c. disallowance of expenses allegedly incurred for earning exempt income u/ s.14A of the Act.

76. Before adverting to the merits of the additions so made, we deem it appropriate, at the threshold, to examine the jurisdiction and scope of enquiry permissible to the AO in cases selected for limited scrutiny. For this purpose, it would be relevant to refer to the instructions issued by the CBDT governing the procedure to be followed and the extent of enquiry permissible in limited scrutiny assessments. The relevant instructions, as relied upon and taken note of by us, are reproduced hereunder.

77. Instruction No.7/ 2014 dated 26.09.2014 issued by CBDT reads as under:

“It has come to the notice of the Board that during the scrutiny assessment proceedings some of the AOs are routinely calling for information which is not relevant, for enquiry into the issues to be considered. This has been causing undue harassment to the taxpayers and has also drawn adverse criticism from several quarters. Further, feedback and analysis of such orders indicates that many times the core issues, which formed the basis of selection of the case for scrutiny were not examined properly. Such instances primarily occurred in cases selected for scrutiny under Computer Aided Scrutiny Selection (CASS’) for verification of specific information obtained from third party sources which apparently did not match with the details submitted by the taxpayer in the return- of-income.

2. Therefore, for proper administration of the Income-tax Act, 1961 (Act’), Central Board of Direct Taxes, by virtue of its powers under section 119 of the Act, in supersession of earlier instructions/guidelines on this subject, hereby directs that the cases selected for scrutiny during the Financial Year 2014-2015 under CASS, on the basis of either AIR data or CIB information or for non re-conciliation with 26AS data, the scope of enquiry should be limited to verification of these particular aspects only. Therefore, in such cases, an Assessing Officer shall confine the questionnaire and subsequent enquiry or verification only to the 2 specific point(s) on the basis of which the particular return has been selected for scrutiny.

3. The reason(s) for selection of cases under CASS are displayed to the Assessing Officer in AST application and notice u/s 143(2), after generation from AST, is issued to the taxpayer with the remark “Selected under Computer Aided Scrutiny Selection (CASS)”. The functionality in AST is being modified suitably to flag the reasons for scrutiny selection in AIR/CIB/26AS cases. This functionality is expected to be operationalised by 15th October, 2014. Further, the Assessing Officer while issuing notice under section 142(1) of the Act which is enclosed with the first questionnaire would proceed to verify only the specific aspects requiring examination/verification. In such cases, all efforts would be made to ensure that assessment proceedings are completed expeditiously in minimum possible number of hearings without unnecessarily dragging the case till the time-barring date.

4. In case, during the course of assessment proceedings, it is found that there is potential escapement of income exceeding Rs. 10 lakhs (for non-metro charges, the monetary limit shall be Rs. 5 lakhs) on any other issue(s) apart from the AIR/CIB/26AS information based on which the case was selected under CASS requiring substantial verification, the case may be taken up for comprehensive scrutiny with the approval of the Pr. CIT/DIT concerned. However, such an approval shall be accorded by the Pr. CIT/DIT in writing after being satisfied about merits of the issue(s) necessitating wider and detailed scrutiny in the case. Cases so taken up for detailed scrutiny shall be monitored by the Jt. CIT/Addl. CIT concerned.

5. The contents of this Instruction should be immediately brought to the notice of all concerned for strict compliance.”

78. Further, relevant part of Instruction No.20/ 2015 dated 29.12.2015 issued by CBDT reads as under: –

3. As far as the returns selected for scrutiny through CASS-2015 are concerned, two type of cases have been selected for scrutiny in the current Financial Year-one is “Limited Scrutiny’ and other is ‘ Complete Scrutiny. The assessees concerned have duly been intimated about their cases falling either in ‘Limited Scrutiny’ or ‘Complete Scrutiny’ through notices issued under section 143(2) of the Income-tax Act, 1961 (‘ Act’ ). The procedure for handling Limited Scrutiny’ cases shall be as under:

a. In Limited Scrutiny cases, the reasons/issues shall be forthwith communicated to the assessee concerned.

b. The Questionnaire under section 142(1) of the Act in “Limited Scrutiny cases shall remain confined only to the specific reasons/issues for which case has been picked up for scrutiny. Further, the scope of enquiry shall be restricted to the ‘Limited Scrutiny issues.

c. These cases shall be completed expeditiously in a limited number of hearings.

d. During the course of assessment proceedings in ‘limited Scrutiny’ cases, if it comes to the notice of the Assessing Officer that there is potential escapement of income exceeding Rs. five lakhs (for metro charges, the monetary limit shall be Rs. ten lakhs) requiring substantial verification on any other issue(s), then, the case may be taken up for ‘Complete Scrutiny’ with the approval of the Pr. CIT/CIT concerned. However, such an approval shall be accorded by the Pr. GIT/CIT in writing after being satisfied about merits of the issue(s) necessitating Complete Scrutiny’ in that particular case. Such cases shall be monitored by the Range Head concerned. The procedure indicated at points (a), (b) and (c) above shall no longer remain binding in such cases. (For the present purpose, ‘Metro charges would mean Delhi, Mumbai, Chennai, Kolkata, Bengaluru, Hyderabad and Ahmedabad)

4. The Board further desires that in all cases under scrutiny, where the Assessing Officer proposes to make additions or disallowances, the assessee would be given a fair opportunity to explain his position on the proposed additions/disallowances in accordance with the principle of natural justice. In this regard, the Assessing Officer shall issue an appropriate show cause notice duly indicating the reasons for the proposed additions/disallowances along with necessary evidences/reasons forming the basis of the same. Before passing the final order against the proposed additions/disallowances, due consideration shall be given to the submissions made by the assessee in response to the show-cause notice.

5. The contents of this Instruction should be immediately brought to the notice of all concerned for strict compliance.”

79. Further, relevant part of Instruction No.5/ 2016 dated 14.07.2016 issued by CBDT reads as under: –

2. In order to ensure that maximum objectivity is maintained in converting a case falling under Limited Scrutiny’ into a ‘Complete Scrutiny case, the matter has been further examined and in partial modification to Para 3(d) of the earlier order dated 29.12.2015. Board hereby lays down that while proposing to take up ‘ Complete Scrutiny’ in a case which was originally earmarked for ‘Limited Scrutiny’, the Assessing Officer (‘ AO’ ) shall be required to form a reasonable view that there is possibility of under assessment of income if the case is not examined under ‘Complete Scrutiny’. In this regard, the monetary limits and requirement of administrative approval from Pr. CIT/CIT/Pr. DIT/DIT, as prescribed in Para 3(d) of earlier Instruction dated 29.12.2015, shall continue to remain applicable.

3. Further, while forming the reasonable view, the Assessing Officer would ensure that:

a. there exists credible material or information available on record for forming such a view;

b. this reasonable view should not be based on mere suspicion, conjecture or unreliable source: and

c. there must be a direct nexus between the available material and formation of such view.

4. It is further clarified that in cases under Limited Scrutiny’, the scrutiny assessment proceedings would initially be confined only to issues under Limited Scrutiny and questionnaires, enquiry, investigation etc. would be restricted to such issues. Only upon conversion of case to ‘ Complete Scrutiny after following the procedure outlined above, the AO may examine the additional issues besides the issue(s) involved in ‘Limited Scrutiny. The AO shall also expeditiously intimate the taxpayer concerned regarding conducting ‘Complete Scrutiny’ in such cases.

5. It is also clarified that once a case has been converted to ‘ Complete Scrutiny, the AO can deal with any issue emerging from ongoing scrutiny proceedings notwithstanding the fact that the reason for such issue have not been included in the Note.

6. To ensure proper monitoring in cases which have been converted from “Limited Scrutiny’ to ‘Complete Scrutiny’, it is suggested, that provisions of section 144A of the Act may be invoked in suitable cases. To prevent possibility of fishing and roving enquiries in such cases, it is desirable that these cases should invariably be picked up while conducting Review or Inspection by the administrative authorities.”

80. The CBDT taking a stern view on unauthorized expansion of limited scrutiny to complete scrutiny has issued a directive dated 30.11.2017 under reference F.No.DGIT (Vig.)/ HQ/ SI/ 2017-18, which reads as under: –

“CBDT has issued detailed guidelines/ directions for completion of cases of limited scrutiny selected through CASS module. These guidelines postulate that an Assessing Officer, in limited scrutiny cases, cannot travel beyond the issues for which the case was selected. The idea behind such stipulations was to enforce checks and balances upon powers of an AO to do fishing and roving inquiries in cases selected for limited scrutiny.

2. Further, the guidelines for proper maintenance of order sheets have been given in the Manual of Office Procedure issued by the Directorate of Organisation and Management Services. The Manual clearly lays down:

A. The minutes of the hearing must be entered with date, in the order-sheet.

B. Make proper order-sheet entries for each posting, hearing and seeking and granting of adjournments.

C. It nobody attends a hearing or the request for adjournment comes after the hearing date, enter the facts in the order-sheet.

Maintenance of a cursory and cryptic order sheet shows irresponsible, ad hoc and undisciplined working of any officer.

3. Instances have come to notice of CBDT where some Assessing Officers are travelling beyond their jurisdiction while making assessments in Limited Scrutiny cases by initiating inquiries on new issues without complying with mandatory requirements of the relevant CBDT Instructions dated 26.09.2014, 29.12.2015 and 14.07.2016. These instances have been viewed very seriously by the CBDT and in one case the Central Inspection Team of the CBDT was tasked with examination of assessment records on receipt of allegations of several irregularities. Amongst other irregularities it was found that no reasons had been recorded for expanding the scope of limited scrutiny, no approval was taken from the PCIT for conversion of the limited scrutiny case to a complete scrutiny case and the order sheet was maintained very perfunctorily. This gave rise to a very strong suspicion of mala tide intentions. The Officer concerned has been placed under suspension.

In view of discussion in the preceding paragraphs it is once again reiterated that the Assessing Officers should abide by the instructions of CBDT while completing limited scrutiny assessments and should be scrupulous about maintenance of note sheets in assessment folders.

81. Further, CBDT has issued a circular F.No.225/ 402/ 2018/ ‘TAX dated 28.11.2018 which is applicable for the cases selected for limited scrutiny under CASS cycles 2017 and 2018. The same is reproduced as under: –

“Under CASS cycles 2017 and 2018, some of the cases were selected for scrutiny as a Limited Scrutiny case. In limited Scrutiny cases, Assessing Officer cannot travel beyond the issue(s) for which the case was selected. The idea behind such a stipulation is to enforce checks and balances upon powers of an Assessing Officer to do fishing and roving enquiries in cases under Limited Scrutiny.

2. In this regard, several representations have been received in the Board from the field authorities that in several cases under “Limited Scrutiny, information pointing out specific tax-evasion for the relevant year, given by any law enforcement/intelligence/regulatory authority or agency is available with the concerned Assessing Officer, however, in view of the restrictive nature of enquiry/investigation which can be made in ‘Limited Scrutiny’ cases, the same presently cannot be acted upon.

3. The matter has been considered by the Board. In order to enable proper enquiry/ investigation in pending Limited Scrutiny cases which were selected through CASS cycles of 2017 and 2018, where credible material or information has by any law been/is provided enforcement/ intelligence/regulatory authority or agency regarding tax-evasion by an assessee, it has been decided by the Board that issues arising from such information can also be examined during the course of conduct of assessment proceedings in such ‘Limited Scrutiny’ cases with prior administrative approval of the concerned Pr. CIT/CIT.

4. It is pertinent to mention that unlike CASS 2015 and 2016 cycles, where consideration of any additional issue lead to the conversion of case to “Complete Scrutiny’ as laid down in Instruction No. 5/2016 dated 14.07.16, the pending ‘Limited Scrutiny cases of CASS 2017 and 2018 cycles would not be taken up for ‘ Complete Scrutiny’ as the present directive is only to facilitate consideration of those issues wherein specific information of tax-evasion has been furnished by any law enforcement/ intelligence/regulatory authority or agency. Therefore, in such ‘Limited Scrutiny’ cases, Assessing Officer shall not expand the scope of enquiry/investigation beyond the issue(s) on which the case was flagged for ‘Limited Scrutiny’ & issue arising from nature of information mentioned in para 2 and 3, above.

5. The following procedure shall be adopted while examining the additional issue:

i. The Assessing Officer shall duly record the reasons for expanding the scope of ‘Limited Scrutiny’ to the extent mentioned in para 2 and 3, above:

ii. The same shall be placed before the Pr. CIT/CIT concerned and upon his approval, further issue can be considered during the assessment proceeding;

iii. The Assessing Officer shall issue an intimation to the assessee concerned that additional issue would also be considered during the course of pending assessment proceeding;

iv. To ensure proper monitoring in these cases, provisions of section 144A of the Income-tax Act, 1961 may be invoked in suitable cases. Further, to prevent fishing and roving enquiries in these cases, it is desirable that these cases are invariably picked up for Review/Inspection by the administrative authorities.

6. The above directive shall be applicable from the date of its issue and shall apply to the pending “Limited Scrutiny’ cases which were selected under the CASS 2017 and 2018 cycles. It is reiterated that the grounds mentioned in para 3 above are the only grounds on which a ‘Limited Scrutiny case of CASS 2017 and 2018 cycles can be expanded in its scope and that too only to the extent of the issues referred to by the law enforcement/ intelligence/regulatory authority or agency.

7. It may be brought to the notice of all for necessary compliance.”

82. We have carefully perused the instructions issued by the CBDT from time to time governing selection of cases under CASS. From the said instructions, it emerges that during the Financial Year 2014-15, cases were selected for scrutiny under CASS primarily on the basis of AIR/ CIB/ 26AS data. However, with effect from Financial Year 2015-16, the CBDT introduced two distinct categories of scrutiny assessments, namely, ‘Limited Scrutiny” and “Complete Scrutiny’.

83. In cases selected for complete scrutiny, the AO is vested with wider jurisdiction to examine all issues arising from the return of income. In contrast, in cases selected for limited scrutiny, the jurisdiction of the AO is confined strictly to the specific issues for which the case has been selected, and the AO is prohibited from travelling beyond such issues. The underlying object of these instructions is to place effective checks and balances on the powers of the AO and to prevent fishing and roving enquiries in limited scrutiny assessments.

84. The CBDT instructions further provide that where, during the course of limited scrutiny assessment proceedings, the AO notices potential escapement of income exceeding Rs.5,00,000/ – in non-metro charges and Rs.10,00,000/ -in metro charges, the case may be converted into complete scrutiny, subject to prior approval of the Principal Commissioner of Income-tax (PCIT)/ Director of Income-tax (DIT). Such approval is required to be accorded in writing after due satisfaction regarding the merits of the proposal. The AO is mandatorily required to record reasons justifying the expansion of the scope of scrutiny and place the same before the PCIT/ DIT for approval. Only upon grant of such approval can the AO legally expand the scope of assessment from limited scrutiny to complete scrutiny.

85. It is also clarified that if the AO proceeds to examine issues other than those for which the case was originally selected under limited scrutiny, without following the prescribed procedure, such action would tantamount to an impermissible conversion of limited scrutiny into complete scrutiny.

86. In so far as cases selected under CASS for AYs 201718 and 2018-19 are concerned, the CBDT instructions further tighten the scope of enquiry. In such cases, the AO is not empowered to travel beyond the issues for which the case has been selected under limited scrutiny. The only exception carved out is where specific and credible information regarding tax evasion is received from an authorized external agency, and even in such circumstances, the AO can examine such additional issues only after obtaining prior approval of the ld. PCIT/ DIT.

87. Thus, with effect from A.Y.2017-18, in cases selected for limited scrutiny, the jurisdiction of the AO is strictly confined to the original limited scrutiny issues and such specific tax evasion issues as may be flagged by authorized external agencies, subject to prior approval of the competent authority.

88. We find that the aforesaid instructions have been issued by the CBDT in exercise of its statutory powers u/ s.119 of the Act. Such instructions, being binding in nature, are mandatorily required to be followed by the AO. It is a well-settled proposition of law that failure on the part of the AO to adhere to the specific circulars and instructions issued by the CBDT while framing the assessment vitiates the assessment proceedings, rendering the resultant assessment order unsustainable in the eyes of law. In this regard, reliance is placed on the following judicial precedents, wherein it has been consistently held that the circulars and instructions issued by the CBDT in exercise of its powers u/ s.119 of the Act are binding on the AO.

89. The Hon’ble Supreme Court in UCO Bank v. CIT [1999] 237 ITR 889 (SC) noted as under:-