ICICI Lombard General Insurance has leapfrogged from fifth to second spot in terms of market share after its merger with Bharti Axa. Now, it is gunning for the top spot on the back of organic growth and a focus on the retail health segment

Eyes on the Prize: ICICI Lombard MD & CEO Bhargav Dasgupta is the company’s longest-serving CEO

Eyes on the Prize: ICICI Lombard MD & CEO Bhargav Dasgupta is the company’s longest-serving CEO

Near the bustling lanes of the Siddhivinayak Temple at Prabhadevi in Mumbai stands a four-storey building that was earlier known as Tata Press. Today, it hosts the buzzing headquarters of ICICI Lombard General Insurance. On its top floor sits its MD & CEO, Bhargav Dasgupta, one of the longest-serving CEOs in the general insurance industry, who has now been in the insurer’s corner room for almost 14 years.

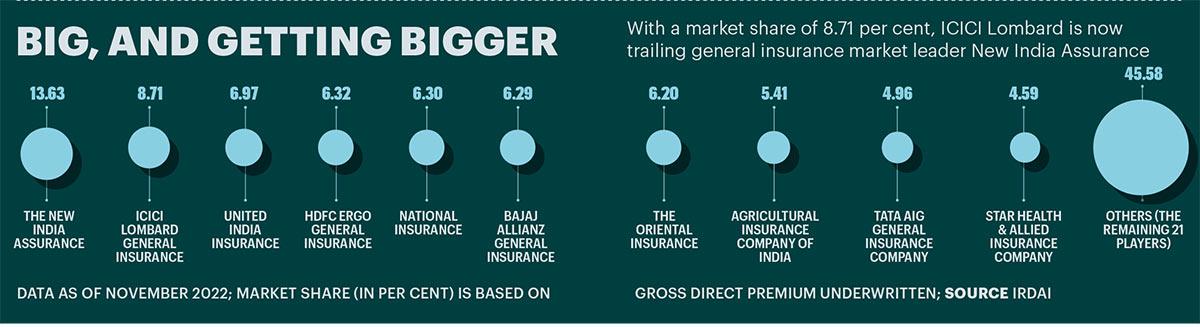

The 56-year-old management graduate from IIM Bangalore took over the reins of the insurer in 2009, but his association with the group goes back to 1992 when he joined ICICI Bank as a Senior General Manager, and then worked in various roles across the group, including as Executive Director in ICICI Prudential Life Insurance. If familiarity gives comfort, then Dasgupta certainly makes one feel at ease with his simplicity and demeanour. His easy approach is reflected in the recent merger of Bharti AXA General Insurance with ICICI Lombard, which became seamlessly effective within days of getting the final approval from regulator Insurance Regulatory and Development Authority of India (IRDAI) in September 2021. After the merger, ICICI Lombard has become the second largest general insurer (on gross direct premium underwritten) with 8.71 per cent market share (till November 2022) after state-owned The New India Assurance(13.63 per cent).

But the hawk-eyed leader of ICICI Lombard—which had a market cap of Rs 61,095 crore on December 27—knows that he can’t rest on his laurels. Although the merger has helped the insurer jump three positions, leaving behind one of its closest competitors, Bajaj Allianz General Insurance, its next challenge is to drive organic growth and also keep competitors at bay.

On the cut-throat competition in the sector, Tapan Singhel, MD & CEO of Bajaj Allianz General Insurance, says, “Acquiring is a different ball game. My belief is to build a solid culture through organic growth. I am not ruling out inorganic growth, but to acquire just to become No. 1 is not our philosophy. Our philosophy is to work really hard to build a 100-year system.”

Moreover, while the merger of three public sector insurers—United India Insurance Co., The Oriental Insurance Company and National Insurance Company—has been put on hold, these insurance firms are snapping at ICICI Lombard’s heels to gain market share. “We do not know in what shape and form it would happen, or if it is going to happen. Obviously, we have to wait and see,” says Gopal Balachandran, 47, CFO & CRO of ICICI Lombard. As per monthly data released by IRDAI, around 20 per cent of the market share was cornered by these three insurers (till November 2022).

Health Conscious

One big positive that has come from the merger for the insurer is the distribution franchise it got in the deal. The number of agents with ICICI Lombard increased by 38 per cent from 59,545 agents in FY21 to around 82,000 by the end of December 2021, apart from the rebranding of over 140-plus branches of Bharti AXA. The merger has also resulted in annualised synergies worth Rs 200 crore of which Rs 70 crore was realised in FY22, with the balance expected to be realised in FY23. “Since it’s a direct benefit of synergies, it’ll accrue to the P&L. But… we are reinvesting into expanding distribution on retail health, and our digital franchise,” says Balachandran. The company’s stock was trading at Rs 1,244 on December 27; it has given negative returns of over 10 per cent year-to-date.

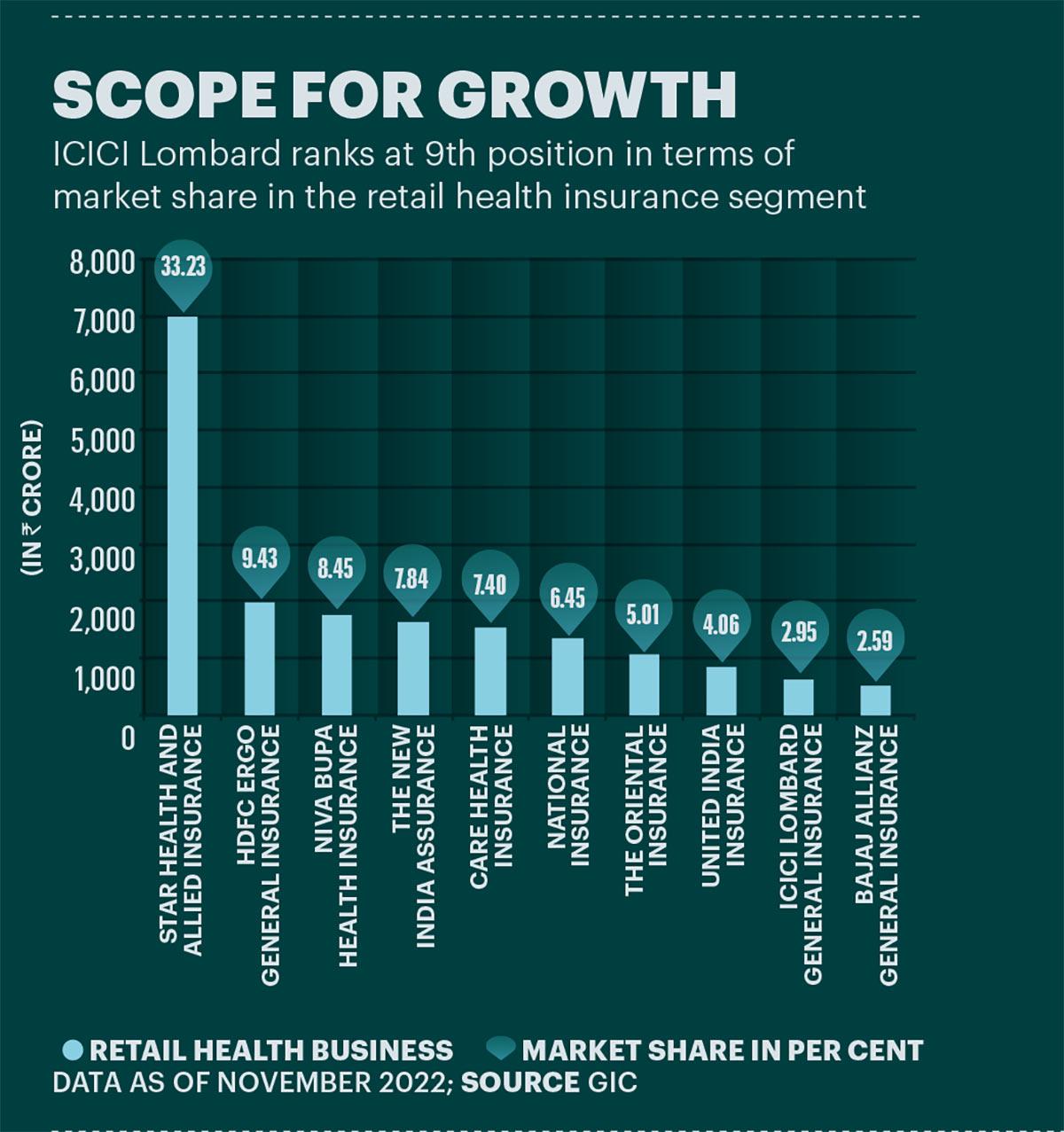

With the benefit of synergies flowing in, Dasgupta knows where to push forward next. As its share in the retail health segment in January-November 2022 was 3 per cent compared to 8 per cent in the general insurance segment, it wants to grow health fast. “We are investing and focussing on retail distribution. In commercial lines, we are anyway large and strong,” says Dasgupta.

“We need to make sure that from 3 per cent, we get to 8 per cent in retail health. That’s clearly the road map one would want to look for at the minimum,” adds Balachandran. ICICI Lombard’s net earned premium (NEP) from health and personal accident (PA) policies stood at Rs 3,354 crore in FY22 compared to Rs 1,115 crore in FY18, growing at a CAGR of 32 per cent. Post-merger, its share in the product mix stood at 27 per cent (H1FY23), compared to 23 per cent in H1FY22.

So, how does the company plan to increase its market share? For higher growth in the retail health segment, it has put in place a strategy of recruiting agency managers who hire agents, and the agents then bring in the business. The insurer wants to hire close to 1,000 health agency managers, who will add about 15 to 20 agents each. “We will add close to 15,000 to 20,000 agents. This is an area of focus, and we will continue to make those investments,” says Balachandran.

Even as the number of agents grows, the insurer has started seeing the results of investing in the health segment with premiums growing by 15.8 per cent in Q2FY23 compared to 8 per cent in Q1FY23. Dasgupta said in an analyst call that ICICI Bank (a sister company) has also restarted distributing indemnity policies on the home side. Also, with the rise in credit disbursals, the attachment business (upselling loan insurance) has picked up.

As per IRDAI, the penetration of general insurance in India in FY22 was nearly 1 per cent, and it has announced a target of 2.52 per cent by 2027. Health insurance is going to play an important role in this growth path, especially post-Covid-19. Per a report from ResearchAndMarkets.com, India’s health insurance market is pegged at $122.11 billion in 2022, which is expected to reach $198.45 billion by 2027 at a CAGR of 10.2 per cent. Calling the opportunity in health enormous, Balachandran says that although health insurance covers out-of-pocket spends, it is not meaningfully utilised. “That’s an area we are significantly looking to tap into for its potential,” he adds. ICICI Lombard’s Cashless OPD policy numbers have grown from an average of 4,400 policies per month to 8,200 policies by the end of H1FY23.

A Ratio of Loss

As the setting sun starts glaring through the tinted windows, Dasgupta is quick to call his assistant to draw the curtains so that the ambience in the room feels comfortable. Once the curtains are drawn, he starts talking about the pain points of post-Covid-19. Apart from a surge in elective surgeries, the industry has been seeing an increase in the frequency of regular medical and critical cases. “Apart from electives, the frequency of normal medical cases has increased. Even for ailments like cancer, we are seeing a higher frequency than pre-Covid-19. In terms of people falling sick and going to the hospital, that percentage has gone up, too,” he says.

Prasun Sikdar, MD and CEO of ManipalCigna Health Insurance, agrees with the trend. “The claim ratio, while stable in the first two quarters of CY22, has seen a steep increase from September onwards. The increase is due to high incidence rates across ailments, especially planned surgeries and critical ailments.”

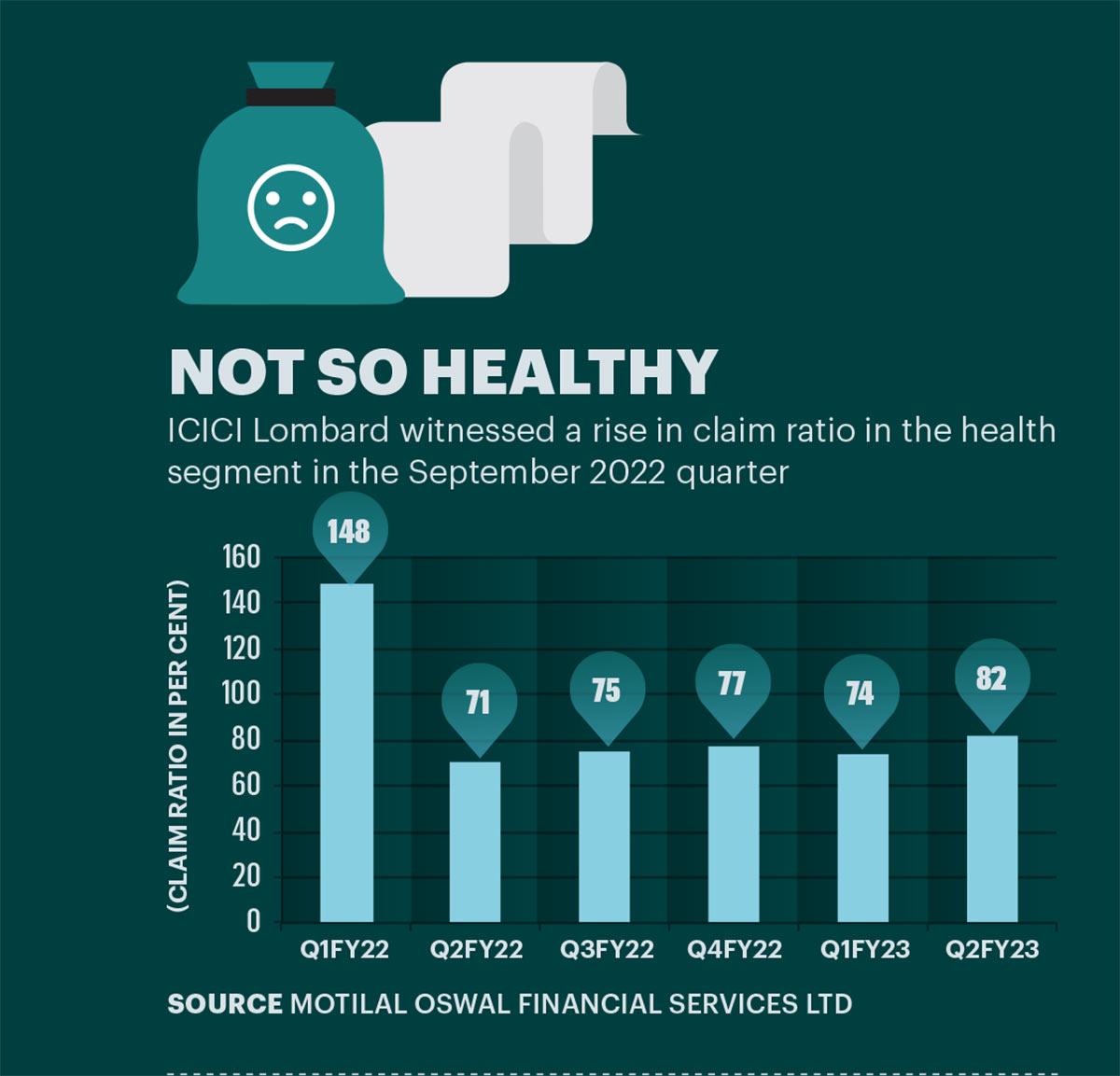

Accordingly, the loss ratio in the health segment (along with travel and PA) for ICICI Lombard increased to 81.8 per cent in Q2FY23 from 71.4 per cent in Q2FY22, and its overall claim ratio increased to 72.8 per cent in Q2FY23 from 69.8 in Q2FY22. Moving in tandem, its combined ratio also continued to be high at 105 per cent in H1FY23. It was at 108.8 per cent in FY22 against 99.8 per cent in FY21 due to the second wave of the pandemic. Consequently, this resulted in a decline in profits to Rs 1,271 crore in FY22 compared to a profit of Rs 1,473 crore in FY21. Dasgupta says that while the claims continue to be high, the combined ratio should be within the target range of 103-104 per cent in FY23.

In the motor insurance business, ICICI Lombard is already a leader with a market share of 11.8 per cent in FY22. The segment is also the largest contributor to its product mix at 46 per cent. But one area of concern was the intense competition in the motor own-damage (OD) segment that resulted in an increase in loss ratio to 74.3 per cent in Q2FY23 from 62.8 per cent in Q2FY22. However, the management expects some cooling off in competition intensity in the next few quarters. “OD pricing is far more aggressive and, hence, we have taken a cautious approach to write businesses in that segment,” says Balachandran. Incidentally, the loss ratio in the motor third party (TP) segment improved to 66.6 per cent in Q2FY23 from 74.6 per cent in Q2FY22.

Loss ratio is calculated by dividing the total claims paid by the total premiums collected. The lower the ratio, the more profitable an insurer is. Combined ratio is calculated by taking the sum of incurred losses and expenses and then dividing them by the earned premium.

While the insurer’s health insurance premiums are growing, its claims are also rising, which can prove to be costly. Another looming threat is the rising Covid-19 cases around the globe. “Consequent to the billings that we see from the hospitals, we are able to get reasonable price increases on the overall corporate health book. That’s why we continue to write those policies. And despite the revisions in pricing, our customer retention rate [remains] at 90 per cent-plus,” says Balachandran, adding that retail health is a long-term portfolio. And therefore, its outcome needs to be constantly monitored to make effective price revisions when needed.

The last price revision that ICICI Lombard did was in Q3FY21, where the weighted average price was increased by roughly 8 per cent. So, is an increase in premiums on the anvil? “As an industry we had not priced for Covid-19 because none of us anticipated it. Despite that, the industry paid a huge amount in claims. In the future, if there’s a consistent increase in healthcare costs in the country, or if more people go to the hospital because of [issues like] long Covid-19, or fear psychosis, then the premiums will have to work,” says Dasgupta.

Digital Boosters

Another area blinking on Dasgupta’s radar is digital. The fact that the insurer has carved out its digital business into a separate unit to compete like a start-up speaks volumes about its digital focus. Its digital business grew by 24.5 per cent in Q2FY23, and accounted for 4.4 per cent of its overall gross direct premium income in the quarter. Direct premiums are the total premiums received before deducting the reinsurance amount.

While the company has been focussing on digital sales, IRDAI has also announced the roll-out of an online marketplace called Bima Sugam, in 2023. So, how will it affect the digital business of insurers? “There’s a lot of discussion about what will be done there. One thought is to come up with new types of products that addresses certain customer segments, which will be available through Bima Sugam. Beyond that… a lot is being done to make it accessible to segments of customers who don’t have access to insurance,” says Dasgupta.

ICICI Lombard’s thrust on digital can also be gauged from the fact that its “IL TakeCare” app has surpassed 3 million user downloads to date, and the insurer spent Rs 823 crore in FY22 to develop its tech infra.

As Dasgupta focusses on the growth of the company, the insurance regulator has come up with a consultation paper to cap the tenure of MDs and CEOs of insurance firms at 15 years, in line with the Reserve Bank of India’s mandate for banks. Although it is still at the proposal stage, the winds of change might soon blow over the insurer as its seasoned leader heads into his 15th year at the helm of the company.

@teena_kaushal