Consumers will be in trouble, given rising European demand from India’s traditional suppliers, the absence of gas storage facilities and the lack of a clear LNG procurement strategy

It would be an understatement to say India is in trouble this year if liquefied natural gas (LNG) prices seesaw wildly between $10 per million British thermal units (mBtu) and $50 per mBtu, as they did in 2022. And, unlike oil, where the country has a cheap supply source in Russia, and other affordable sources in West Asia, there is none to supply the liquefied fuel to India at rates that consumers can afford. Yet India’s fertiliser and domestic city gas businesses are heavily dependent on natural gas supplies, and India’s 2070 net-zero climate change target is contingent on increasing gas as a fuel in the economy.

What are the key warning signals for India’s gas industry in 2023?

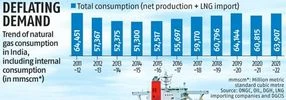

The demand scenario: Demand for gas in India declined for the first time in eight years this fiscal (excluding a Covid 19-induced dip in 2020-21) after rising steadily until 2019-20. Consumption in the April-November period of this fiscal (2022-23) fell 6.3 per cent at 40.9 billion cubic metres from the same period in pandemic-hit 2021-22.

Consumption of the fuel in normal times last fell in 2014-15, when the Modi government was first elected, by 2 per cent from the previous fiscal. Since then, gas use has increased by a cumulative 25 per cent to around 64 billion cubic metres in 2021-22, according to oil ministry data. The growth was still negligible, despite gas prices falling as low as $2 per mBtu, compared to China. Overall, gas demand is still below 2011-12 levels when India’s economy was a third of current GDP, and dependence on imported LNG was at around half of current levels.

LNG prices: These are expected to stay strong but volatile, compared with sustained levels of $2 per mBtu seen in 2020, after western sanctions on Russian gas disrupted supplies of 85 billion cubic metres of gas last year (which is equivalent to a little less than what India and Bangladesh together consume annually). Russian state-run Gazprom’s sales to Europe and Turkey were at their lowest this century, with shipments falling to 87 billion cubic metres in calendar 2022 from 174 billion cubic metres in 2021, according to data from London-based market intelligence provider Argus and Gazprom.

The squeeze on European supplies sent benchmark gas prices at Dutch TTF to a record in August equivalent to $94 per mBtu LNG levels. But TTF month-ahead prices now average $36 per mBtu, 5 per cent below last year’s levels, said Greg Molnar, gas analyst at Paris-based International Energy Agency (IEA), because of mild weather in Europe and adequate storage. Asia’s JKM gas benchmark is down by 12 per cent on the year to $32 per mBtu — but it is still more than three times what India paid for LNG in 2021-22. The drastic decline in gas prices since August owes more to weather and inventories rather than higher supplies.

Europe will need around 75 million tonnes a year of LNG, equivalent to over three times of what India consumes, to substitute 100 billion cubic metres of Russian gas this year. But Qatar, the world’s biggest LNG producer, plans to increase output by only 33 million tonnes a year, and North America and Africa plan to add 40-50 million tonnes a year. Most of this capacity will be operational by 2026-27, exposing countries like India to volatility in rates in the meantime.

Storage facilities: Nikos Tsafos, an international energy expert and energy adviser to the Greek government, said governments and consumers must prepare for the most unlikely scenarios in 2023, and have contingency plans. But India has little recourse. There are almost no gas storage facilities, unlike in China, the US and Europe because the government did not focus on this aspect of the gas supply chain. This renders India even more vulnerable to global price swings. India’s crude-linked LNG term contracts, another form of insurance against gas price volatility, also came under risk in 2022 — Gazprom abruptly ceased shipments under a 20-year, 2.5 million-tonne-a-year supply contract with Gail. Supplies will not resume soon, and the penalty clauses are too meagre to substitute with spot LNG, a Gail official said.

Moreover, over a third of India’s annual LNG supplies comes from a single Qatari supply contract, set to expire in a few years. Even as China snapped up tens of millions of tonnes of term LNG in the last two years at a competitive 10 per cent indexation to crude, Petronet LNG, India’s biggest LNG importer, missed the bus. Now Indian importers must compete with Europe, which has the ability to pay steep premiums for term volumes. Structural supplies of LNG will be difficult as it’s sold out until 2026, says Yiyong He, founder/CEO at Singapore-based LNG Easy.

Exploration: India’s latest price caps on domestic gas supplies threaten to deter exploration because it is expensive and high-risk to drill in deep waters, where India’s potential gas reserves lie. The government, under pressure from city gas companies, will accept recommendations of the Kirit Parikh committee, capping rates at 24 per cent less than the $8.57 per mBtu that explorer ONGC currently charges for supplies. These caps will whittle investor interest to drill in India even more.

Lack of local supplies and storage facilities make the Modi government’s target of gas meeting 15 per cent of India’s energy mix by 2030 from 6 per cent look even more distant. Yet, LNG import dependency will surge from current 50 per cent levels, creating uncertainties for investors who have Rs 2 trillion riding on gas infrastructure investments, industry officials say.

So, the Indian natural gas business, key to the country achieving its net-zero targets in 2070, steps gingerly into a 2023 laden with egg shells. Indian consumers and investors will be hanging on the coat-tails of hopes for milder weather to reduce volatility in LNG price levels, which at one point last year exceeded Indian affordability by a factor of three.

Tsafos said governments must be nimble, creative, targeted and pragmatic in this new global gas environment. For that, New Delhi must free fuel prices instead of meddling with them, and regulators must stop sitting on proposals for months and move faster.