Clipped from: https://learn.quicko.com/income-tax-notice-for-proposed-adjustment-section-143-1-a

What is Notice u/s 143(1)(a)

Communication received u/s 143(1)(a) is communication for proposed adjustment u/s 143(1)(a) received from the income tax department. This notice is issued for the following reasons:

| Section | Reason |

| 143(1)(a)(i) | Arithmetical Error in ITR |

| 143(1)(a)(ii) | Incorrect Claim in ITR |

| 143(1)(a)(iii) | Disallowance of loss claimed in ITR |

| 143(1)(a)(iv) | Disallowance of expense claimed in ITR |

| 143(1)(a)(v) | Disallowance of deduction claimed in ITR |

| 143(1)(a)(vi) | Addition of income appearing in Form 26AS, Form 16 or Form 16A |

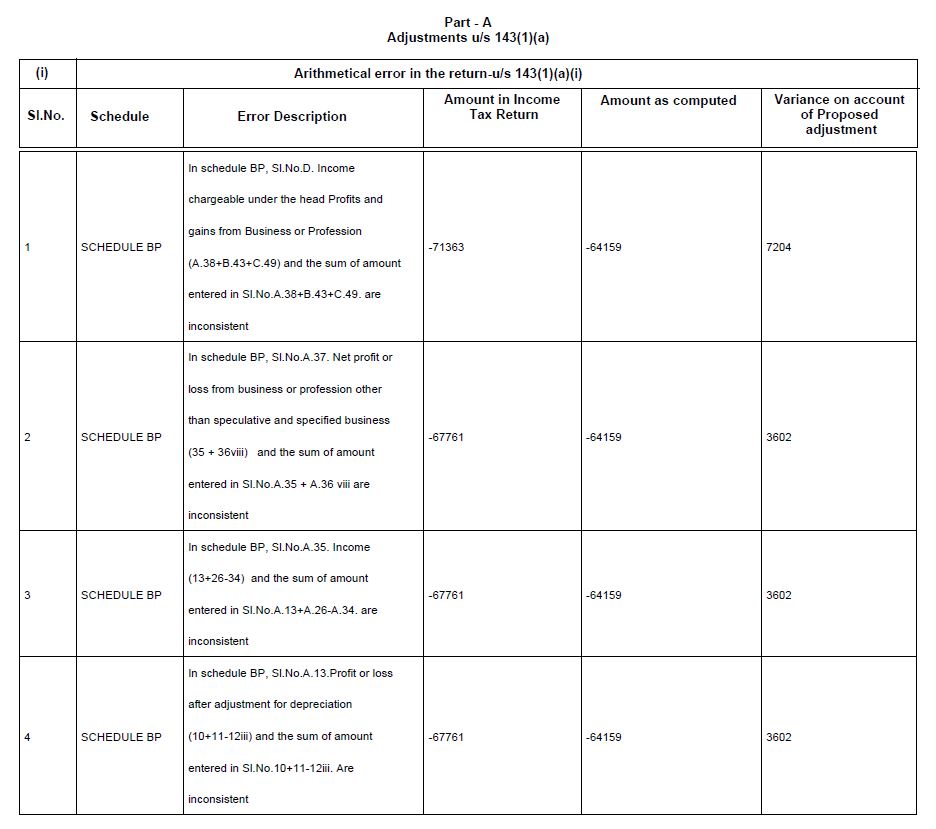

Notice u/s 143(1)(a)(i)

Notice u/s 143(1)(a)(i) is issued when there is an arithmetical error in the filed Income Tax Return. It is sent to the registered email of the assessee. The notice mentions income head, amount reported in ITR, amount as per computation, amount of variance and description of error. The assessee must submit a response to this notice within 30 days from the date of issue.

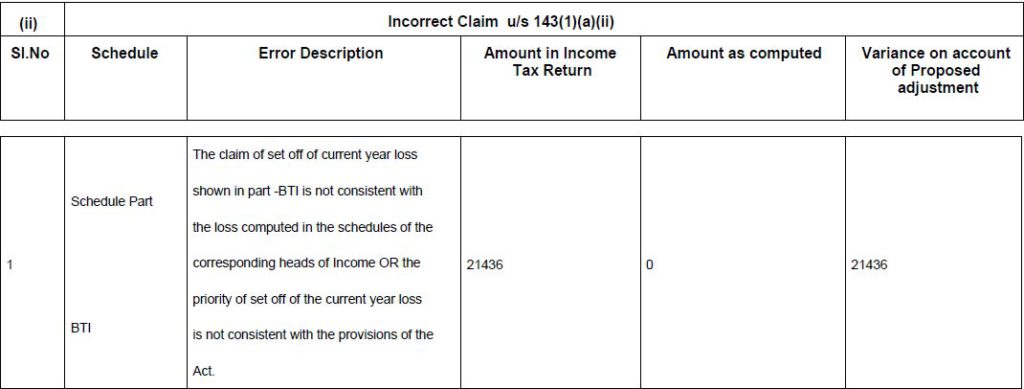

Notice u/s 143(1)(a)(ii)

Notice u/s 143(1)(a)(ii) is issued when there is an incorrect claim in the filed Income Tax Return. It is sent to the registered email of the assessee. The notice mentions income head, amount reported in ITR, amount as per computation, amount of variance and description of error. The assessee must submit a response to this notice within 30 days from the date of issue.

Incorrect claim means:

- An item in the ITR is not consistent with the same item or any other item in the ITR

- Information that needs to be reported in the ITR has not been reported

- Deduction claimed in the ITR exceeds the specified statutory limit as per the Act

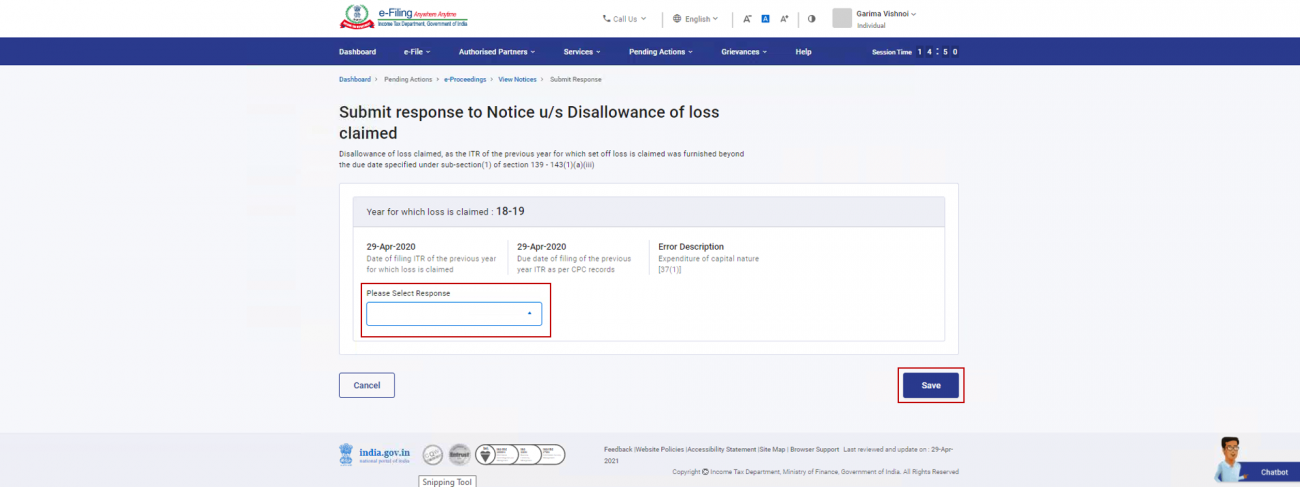

Notice u/s 143(1)(a)(iii)

Notice u/s 143(1)(a)(iii) is issued when the loss has been incorrectly claimed in the ITR filed. It is sent to the registered email of the assessee. The notice mentions income head, amount reported in ITR, amount as per computation, amount of variance and description of error. The assessee must submit a response to this notice within 30 days from the date of issue.

As per the Income Tax Act, the assessee cannot carry forward the loss if he files his income tax return after the prescribed due date. When the return is filed after the due date u/s 139(1) and yet the loss has been claimed, notice u/s 143(1)(a)(iii) is issued to disallow such loss.

Notice u/s 143(1)(a)(iv)

Notice under section143(1)(a)(iv) is issued when an expense has been incorrectly claimed in the ITR filed. It is sent to the registered email of the assessee. The notice mentions income head, amount reported in ITR, amount as per computation, amount of variance and description of error. The assessee must submit a response to this notice within 30 days from the date of issue.

If an expense is disallowed under the audit report but the assessee claims it in the income tax return. Notice under section 143(1)(a)(iv) is issued to disallow such expense.

Notice u/s 143(1)(a)(v)

Notice u/s 143(1)(a)(v) is issued when a deduction has been incorrectly claimed in the ITR filed. It is sent to the registered email of the assessee. The notice mentions income head, the amount reported in ITR, amount as per computation, amount of variance, and description of the error. The assessee must submit a response to this notice within 30 days from the date of issue.

If the assessee files his Income Tax Return after the due date prescribed u/s 139(1). Thus in such case he cannot claim certain specified deductions (Sec10AA and Sec 80H to Sec 80RRB under chapter VI-A). However, if he has claimed such deductions, the tax department would issue a notice u/s 143(1)(a)(v).

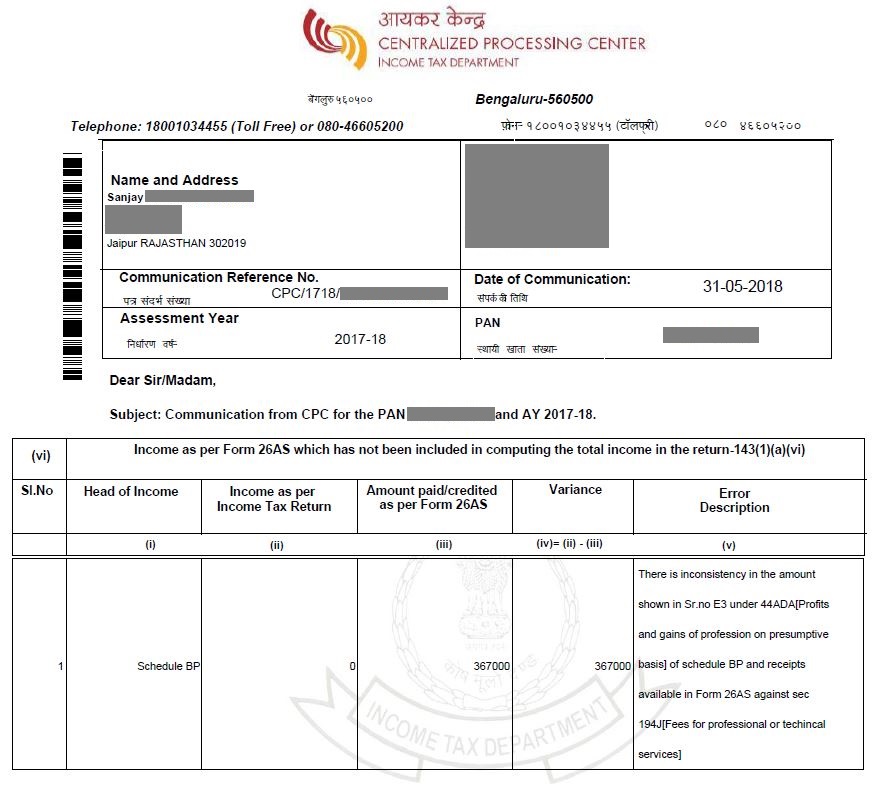

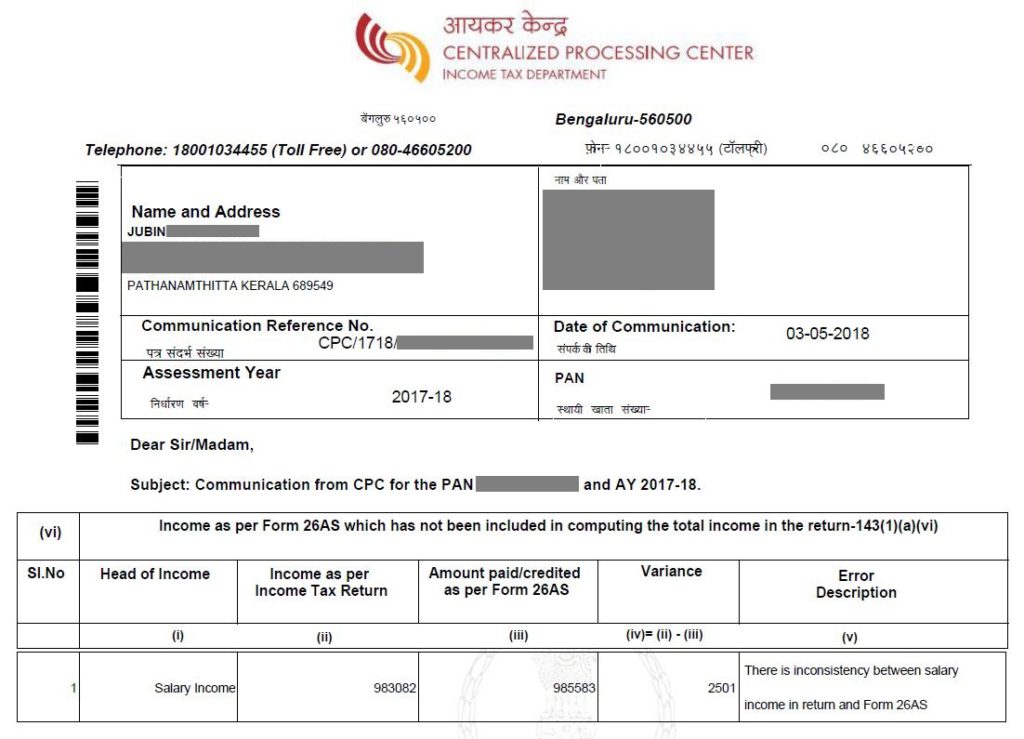

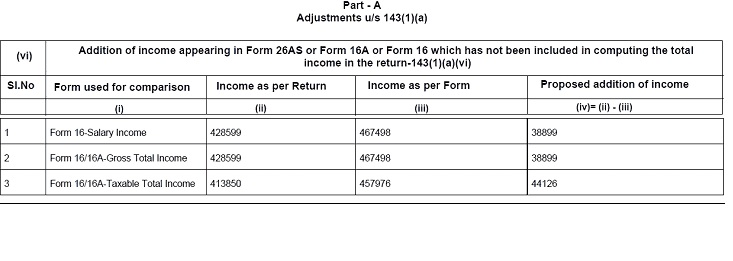

Notice u/s 143(1)(a)(vi)

Income Tax Notice u/s 143(1)(a)(vi) is received when there is a mismatch in details of TDS on salary as per Form 26AS or Form 16 or mismatch in TDS as per Form 16A and income details reported in the filed Income Tax Return. The notice communicates the head of income, the amount reported in ITR, amount as per Form 16/26AS/16A, amount of variance, and the description of the error. There can be following 3 possibilities:

- Business or Profession Income reported in Schedule BP of ITR does not match with the gross amount in Tax Credit Statement.

- Taxable Salary reported in Schedule S of ITR does not match with the gross amount in Tax Credit Statement

Taxable Salary in ITR does not match with the Taxable Salary as per Form 16. This means that an extra deduction has been claimed in the ITR which is not reflected in Form 16

Communication of proposed adjustment u/s 143(1)(a)

How will I receive Communication u/s 143(1)(a)?

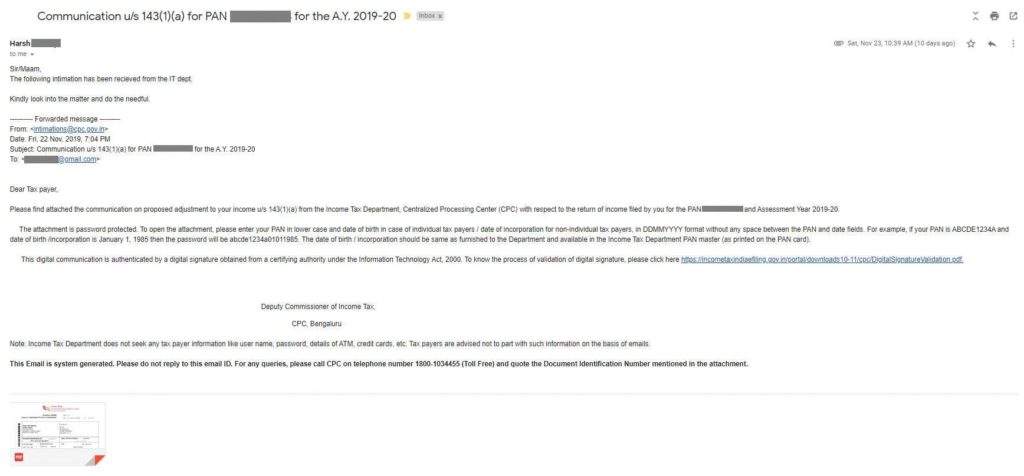

Communication on Email

- The system auto-generates the communication u/s 143(1)(a) and sends it to the assessee on the email entered while filing the income tax return

- The sender of these email is CPC i.e. Central Processing Centre and the sender’s email is intimations@cpc.gov.in

- The subject of the email is ‘Communication u/s 143(1)(a) for PAN CDAxxxxx8P for the A.Y. 2019-20‘. The PAN and AY (Assessment Year) would be different in each case

- The notice is attached to the email in a pdf format. It is password protected. The password to open is PAN in lower case and the date of birth in DDMMYYYY format. Eg: aagpr1212a02101980 for PAN: AAGPR1212A and DOB: 02/10/1980

Communication on SMS

- The system auto-generates the communication u/s 143(1)(a) and communicates to the assessee on the mobile entered while filing the income tax return

- The sender of the message is CPC i.e. Central Processing Centre and the sender’s name is VM-ITDCPC

Time Limit for issue of Communication for Proposed adjustment u/s 143(1)(a)

The income tax department can send intimation u/s 143(1)(a) within one year from the end of the financial year in which the return is filed.

Example

Taxpayer files ITR for FY 2018-19 in July 2019 or October 2019

End of financial year in which return is filed – 31st March 2020

One year from end of financial year – 31st March 2021

Therefore, the tax department can send intimation for ITR of FY 2018-19 up to 31st March 2021

If a taxpayer does not receive any intimation within such period, it means that there are no adjustments and changes to the ITR filed. There is no change in tax liability or refund. Thus, the Income Tax Return filed is deemed to be intimation u/s Section 143(1).

Due Date to submit response to notice u/s 143(1)(a)

If you have received a notice under section 143(1)(a), you must file a response within 30 days from the date of issue of notice.

- If you Agree to the mismatch in notice – File a Revised Return u/s 139(5)

- If you Disagree to the mismatch in notice – Submit a response

- When you Partially Agree to the mismatch in notice – File a Revised Return u/s 139(5) and submit a response

How to File Response to Notice u/s 143(1)(a)

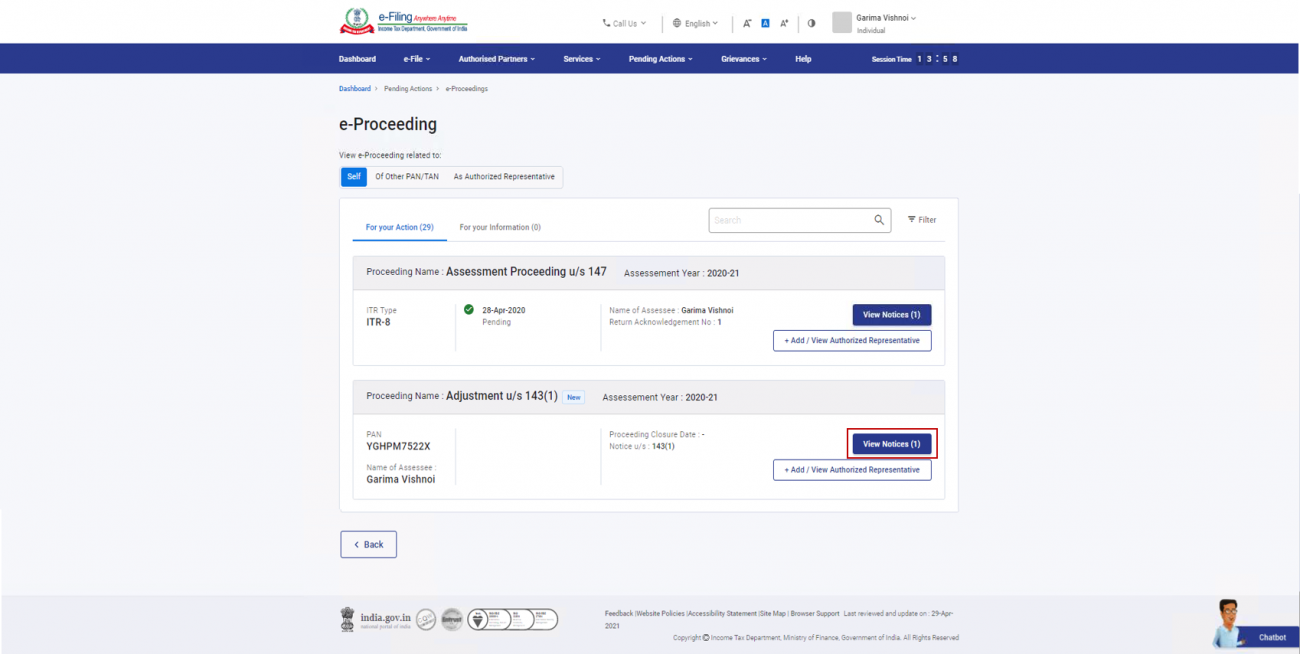

- Visit the e-Filing portalLogin using valid credentials on the e-Filing portal.

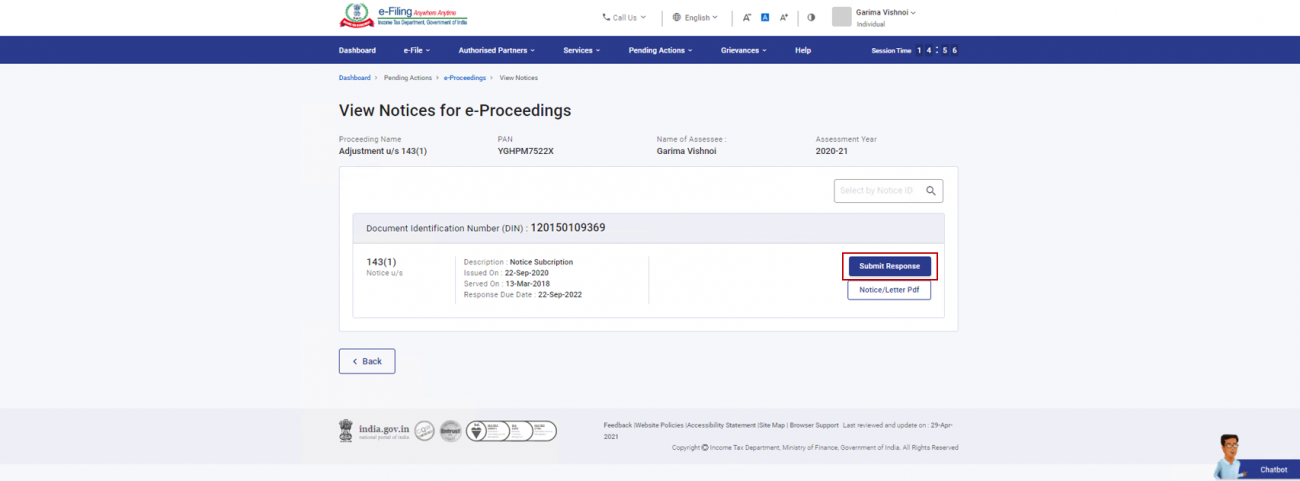

- Pending ActionsClick on Pending Actions > e-Proceedings from the dashboard

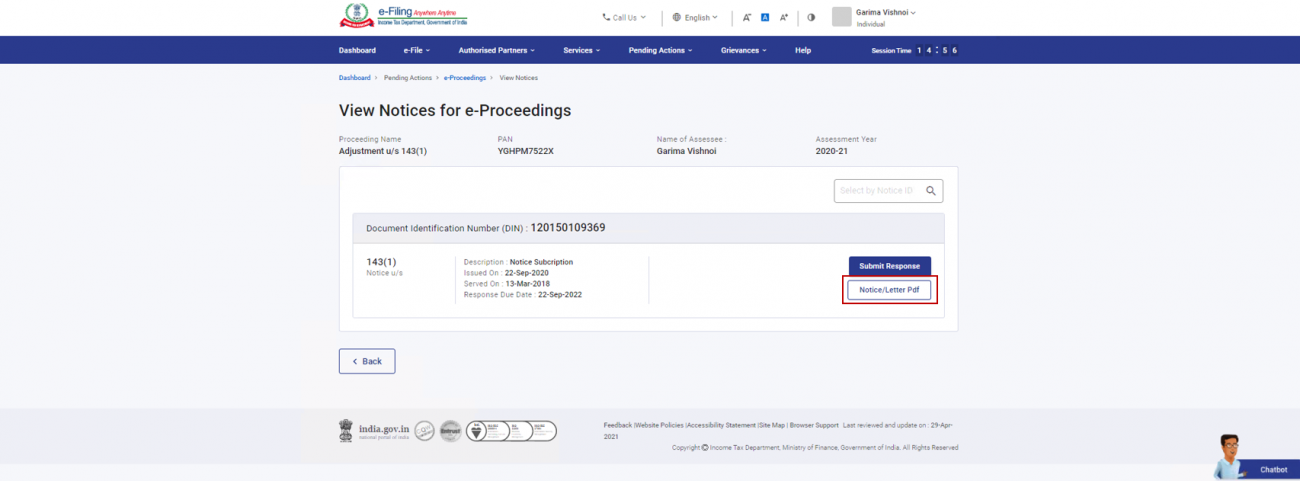

- View NoticesClick on the option to View Notice for adjustment u/s 143(1)

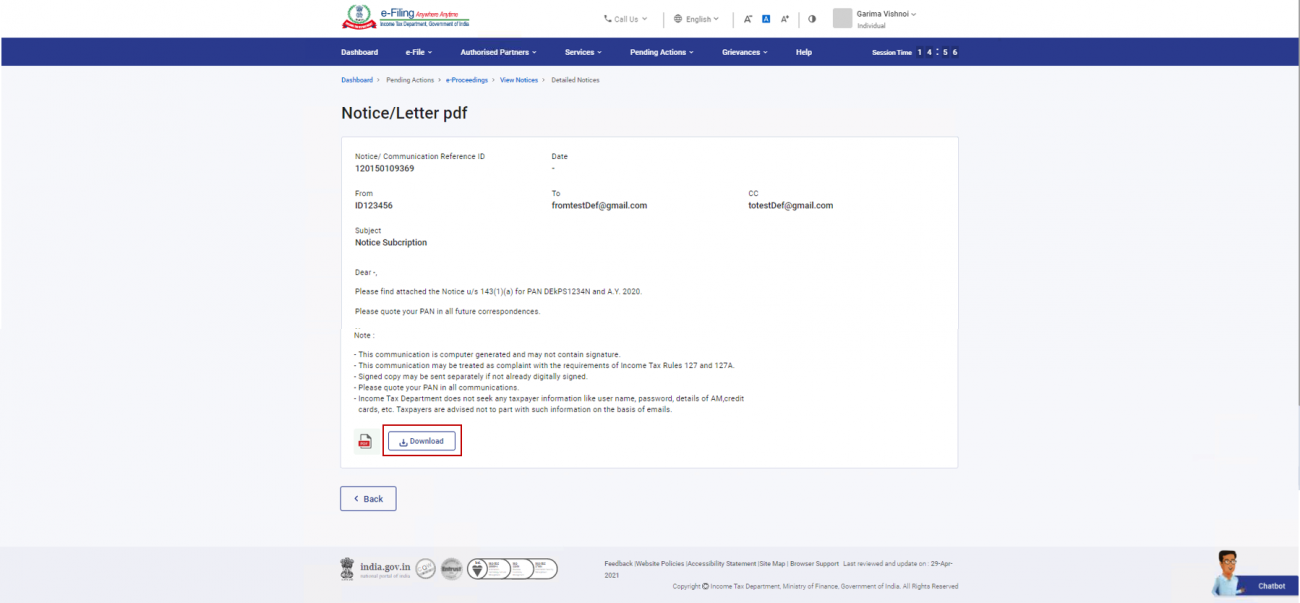

- Notice pdfClick on the Notice/Letter pdf.

- Download the noticeYou will be able to view the notice issued to you. If you wish to download the notice, click Download.

- Respond to NoticeClick on the option to submit response.

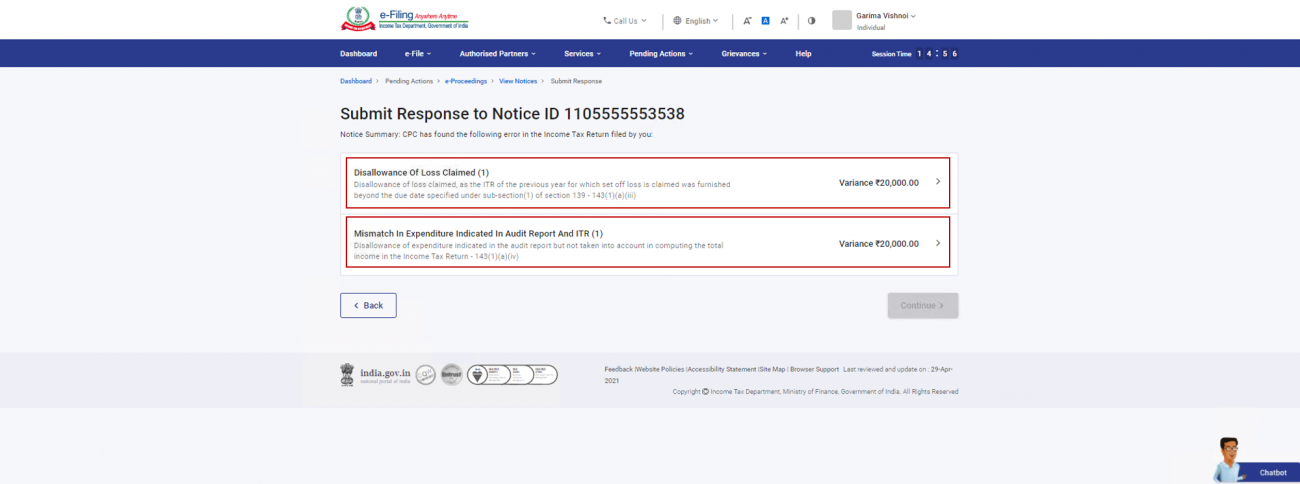

- Details of the Prima Facie AdjustmentsYou will be able to view the details of the Prima Facie Adjustments found by CPC in your filed ITR. Click on each variance to provide responses.

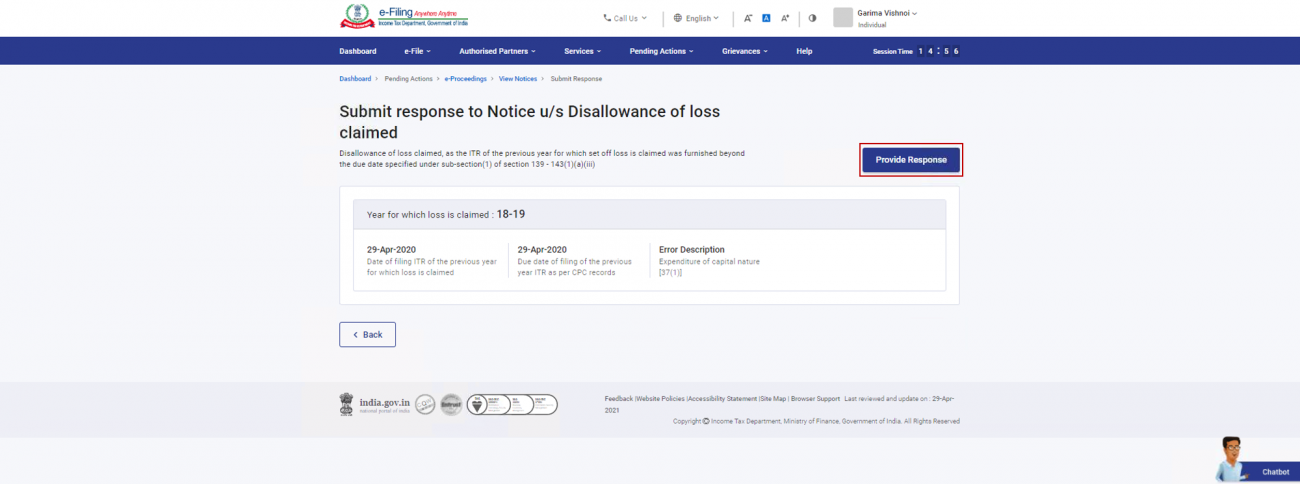

- Provide ResponseOn clicking the variance, details of the variance will be displayed. To provide response for the particular variance, click Provide Response.

- Response from dropdownSelect the relevant response from the dropdown and click Save after responding to each Prima Facie Adjustment.

- Proceed to e-Verify your responseOnce all the responses have been provided, click Back. On clicking Back, you will be taken back to the details of Prima Facie Adjustment found by CPC in your filed ITR. After responding to each variance, the responses will be saved. Click Continue. Select the Declaration checkbox and click Proceed to e-Verify.

- Successful VerificationOn successful e-Verification, a success message is displayed along with a Transaction ID. You will also receive a confirmation message on your email ID registered on the e-Filing portal.

FAQs

Is income tax notice u/s 143(1) different from notice u/s 143(1)(a)?

Communication u/s 143(1) is just an intimation and not a notice. Under this intimation, there is a preliminary check whether the calculations as per ITR match with the calculations as per tax department.

If there is any mismatch in the data, the department issues a notice for adjustment u/s 143(1)(a) The taxpayer needs to respond to this notice within 30 days.

How do I check my 143(1) online?

Generally IT Department sends intimation u/s 143(1) on the registered mail. However, if you have not received you can still request for 143(1) by logging into your Income tax account, then my account and request for 143(1) intimation under service request.

What does pending for response to proposal of adjustment u/s 143(1)( a) ?

A communication for such an adjustment under Section 143(1)(a) is sent to taxpayers wherein there is a mismatch of the income/deductions/exemptions reported in the Income Tax Return and in the income/deductions/exemptions as shown in the Form 16.