If heir provides guarantees, lender may ease repayment schedule

Since a home loan is a long-term liability that can last from 15 to 30 years, the possibility of the borrower dying during the tenure of the loan cannot be ruled out. This has serious implications for the co-borrower and legal heirs.

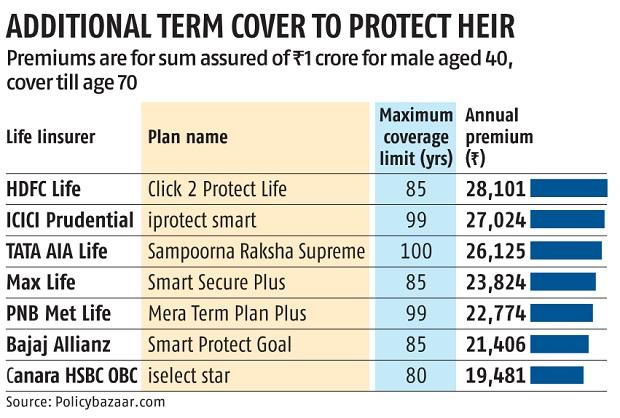

Buy insurance protection

To minimise hardship for legal heirs, home loan borrowers must purchase additional insurance cover while taking a home loan.

“Some lenders require mortgage insurance to approve a loan application. You can either buy home loan insurance (also called home loan protection plan) or a life insurance cover, such as a term cover,” says Atul Monga, chief executive officer (CEO) and co-founder, Basic Home Loan.

The nominee can use the payout from the policy to close the outstanding home loan dues. “Many home loan insurance plans also cover the policyholder in case of a critical illness or disability,” says Adhil Shetty, CEO, BankBazaar.com.

Who is liable to repay?

In case a borrower passes away, her death should be reported to the home loan company and a copy of her death certificate should be submitted.

The primary responsibility for repaying the home loan after the borrower’s death falls on the co-borrower, if there is one.

Says Monga: “The surviving co-borrower is required to provide information about her monthly income along with other details. The lender will then evaluate if her income is sufficient to repay the outstanding loan fully.”

If the co-borrower is not looking to repay the loan, she can contact the lender and request to be released from the liability. A written notice is required from the home loan company that states that she no longer has any responsibility to repay the loan.

After the co-borrower, the liability falls on the legal heir/s. “If there is no co-borrower or the co-borrower is also dead, the lender will try to identify the borrower’s legal heir and transfer the loan account to her after evaluating her repayment capacity and other facets of her credit profile,” says Ratan Chaudhary, head of home loans, Paisabazaar.com.

A spouse or a civil partner can also apply for a loan transfer deed. This is an agreement between both the parties that transfers responsibility for the home loan to them.

Heirs can renegotiate terms

A co-borrower or an heir who is struggling to repay but does not want the property to be auctioned should try to renegotiate the terms of the loan.

“The heir or co-borrower can negotiate easier repayment terms with the lender. She can offer some guarantees, like some property or other assets that she holds, to the lender. She may also be able to offer an acceptable level of guarantee from a third party willing to support her financially,” says Monga.

Shetty points out that while the lender bank cannot force the co-applicant or legal heir to shoulder the burden of the loan, it will try to find a mutually acceptable solution. “This could be in the form of deferred payments, a smaller EMI, or even a settlement if the outstanding amount is very small,” he says.

Only if these solutions don’t work out will the lender repossess the property and auction it.

Auctioning is the last resort

If the legal heirs are unable to service the loan, the lender can eventually resort to selling the property to recover its dues.

“The lender can take possession of the house under the Sarfaesi Act. It can then auction the property to recover its dues,” says Shetty. He adds that repossession, however, is the final measure and lenders attempt to reach a solution before resorting to it.

Adds Monga: “The proceeds from the sale are first used to recover the outstanding debt. Any excess money left is handed over to the heir,” says Monga.