SynopsisPayments bank is a major growth driver for One97 Communications. While an RBI curb on onboarding new customers may not have a huge financial impact, it puts a big question mark on the possibility of Paytm getting a small finance bank licence. The ban adds more pain points to the Paytm stock, already trading at one-third of its issue price.

Is Paytm turning into a value buy?

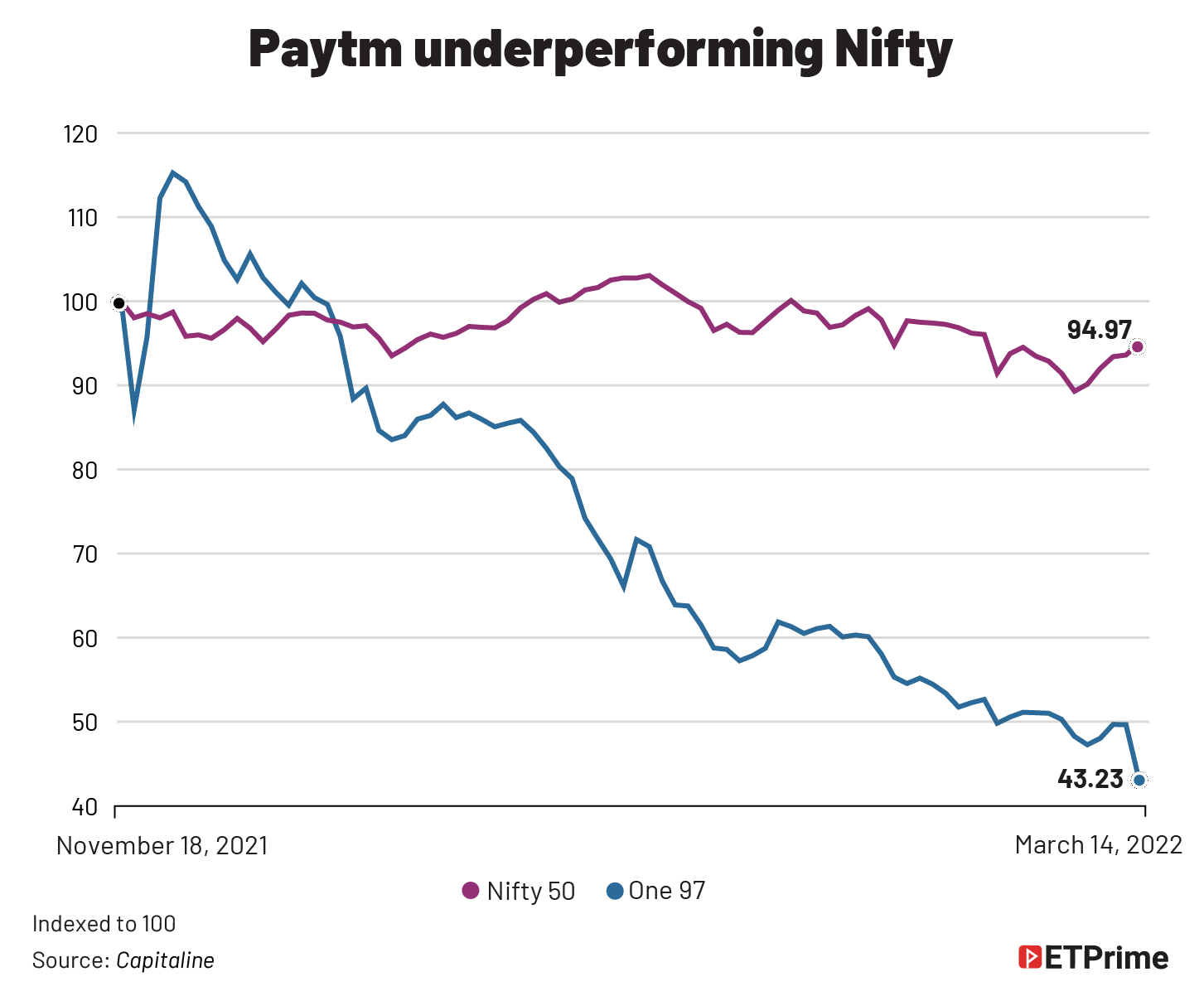

Last week, Paytm investors and market experts saw a flicker of hope amid a steep price erosion in the stock since its listing on November 18 last year. It was aided by the buzz that the fintech major would ask the Reserve Bank of India (RBI) for a small finance bank (SFB) licence in June this year.

But a bucket of cold water followed as the RBI barred Paytm Payments Bank (PPB) from onboarding new customers due to likely gaps in its technology systems, sending the shares down by 13% on Monday morning trade. At Monday’s close, the stock was down 69% from its IPO issue price of INR2,150. The central bank has also ordered a comprehensive system audit of its IT system by a third-party audit firm to address “material supervisory concern”.

So, from the issue price of INR2,150 to INR675 now, what really is the bottom for the Paytm stock?

“Earlier, I thought value would emerge at around INR700, but with this development, I think we may see value at around INR400,” says independent analyst Ambareesh Baliga.

Many, however, believe it is difficult to gauge the bottom, given all the developments since listing and as there is no clarity on profitability.

“It is difficult to predict a bottom in companies, where there is no clarity as to when the company will turn profitable,” says Sandip Sabharwal, founder of asksandipsabharwal.com.

The RBI crackdown on PPB has brought more bad news for Paytm and its listed parent One97 Communications. It has put to rest any hopes of Paytm procuring an SFB licence any time soon, equity brokerage Macquarie said in a report.

PPB is owned by One97 (49%) and its founder Vijay Shekhar Sharma (51%) and plays a huge role in the growth of the company and its future prospects. PPB has a revenue-sharing agreement with Paytm, contours of which are not public. However, according to a draft red herring prospectus (DRHP) filed last year, around INR900 crore or 33% of Paytm’s revenues for FY21 came directly from PPB. Also, Paytm paid around INR980 crore in the form of payment-processing charges to PPB.

Before we tell you more about the implications of the ban and why getting an SFB licence is important for Paytm, let us dig deeper to understand how long the ban could stay and why the RBI is miffed with PPB.

A hard knock

Previous instances of bans on customer onboarding show these are not short-term restrictions.

RBI’s ban on Mastercard from issuing new credit cards early last year has not yet been revoked. The regulator had banned the country’s largest private-sector bank, HDFC Bank, from issuing new credit cards and digital products for around nine months. The central bank has been extremely strict about tech audits, as we have told you here.

“It was 15 months until RBI lifted the full ban on HDFC Bank. When it took so long for a bank of that stature, we don’t know when will RBI revoke the ban on PPB,” says Baliga.

“It raises questions on their process and internal controls. The ban may be temporary, but definitely hits the top line,” he adds.

On Monday, Bloomberg reported that RBI’s ban was on account of data sharing with China-based entities that have a considerable shareholding in the company. This goes against RBI’s mandate on financial data localisation. Paytm in a statement called the report false stating that all the Indian customer data resides within India.

While the RBI doesn’t publicly share the specifics about banning an entity, the other possible reasons for putting a curb on PPB could be the following: not closing dormant accounts, not doing full KYC (know your customer) of accounts older than one year, keeping more money than allowed in a payments bank account or even not responding to requisite details requested by the regulator.

The biggest problem could be RBI asking PPB to close the bank accounts for which it did not do full KYC. in the past, many fintech players have been found to be not doing full KYC.

“If this is not a grave mistake according to the RBI, the ban could be lifted in as early as a month. RBI would not likely ask them to close the existing accounts for not doing full KYC because it could inconvenience the customers,” says the digital head of a large private-sector bank. However, doing full KYC in the next couple of months could put an enormous cost and pressure on Paytm.

“PPB houses all the key products offered by Paytm including wallets, UPI, and deposit accounts. All of Paytm’s 330 million-plus wallet accounts, as well as over 150 million UPI handles, are housed in PPB. Hence, a ban on onboarding customers is effectively a ban on onboarding customers for Paytm,” says the Macquarie report.

The price of a ban

Over the last three years, PPB has become a crucial element in the payments firm’s growth or even survival. It may well be rejuvenating the Paytm brand.

Paytm’s initial resistance to adopting UPI meant that consumers shifted en masse to UPI apps such as Google Pay and PhonePe, which together hold more than 80% of the market. Meanwhile, merchants, who adopted mobile payments since the demonetisation days, stuck to Paytm and its interoperable QR code platform that helps them receive payments either through the Paytm wallet or UPI. And most of these merchants had linked their receivables to PPB accounts.

PPB has been adding close to 0.4 million customers every month and has over 100 million KYC customers. More than half of around 25 million merchants on the Paytm platform use PPB as their settlement bank.

While the bigger payment gateway and point of sale (PoS) companies targeted large merchants, Paytm onboarded a lot of small businesses like restaurants, shops, and petrol pumps across the country. And most of them used PPB as their bank account for receiving digital payments. The soundbox, which announces the successful payments, made the system foolproof for merchants. From 0.9 million PoS devices in June 2021, the company’s merchant-payment installations grew to 2.3 million till date.

In fact, even in January this year, PPB has been the biggest beneficiary bank in the UPI ecosystem, a position it has held since January 2020, the month since when data is available on the National Payments Corporation of India (NPCI) website. It had around 212 million transactions then, which has grown to 957 million in January 2022. Even the country’s largest bank SBI is a distant second with 648 million transactions in January this year.

Despite the ban, Paytm can add new customers with the interoperability of wallets with bank accounts and UPI from next month onwards. Although this is possible logistically, it will be expensive for it to run and maintain. While a payments bank can hold up to INR2 lakh at the end of the day, wallet balance cannot cross INR99,999 at any given point of time. When the balance in a payments bank crosses INR2 lakh, it can be transferred to Paytm’s partner commercial bank as fixed deposit.

So, the immediate financial impact of the ban may not be huge, but the company’s brand and reputation do take a big hit and add to the woes of the investors as the stock price may take a further beating.

ICICI Securities, which had estimated Paytm’s consumer base to grow 10% in FY23 and monthly transacting users to rise at a run rate of more than 25%, believes the company will have to increase its efforts to enhance engagement with the existing user base to offset the adverse impact of an embargo on new users.

The brokerage maintained its rating on the stock but cut its target price to INR1,285 from INR1,352 earlier. Morgan Stanley has slashed its price target for the stock to INR935 from INR1,425 following the ban. Even when domestic brokerages and funds brought down the target price of Paytm, most international firms had previously stuck with higher share prices, which seems to be changing now, indicating more bad news for the company.

“We do not expect the impact on business for Paytm from this ban to be substantial, since Paytm has already onboarded a very large customer base onto the payments bank. However, we would expect a significant impact on Paytm’s brand and customer loyalty going forward,” Macquarie analysts Suresh Ganapathy and Param Subramanian said in the note. They maintained their underperform rating on the stock with a target price of INR700.

“Paytm has been showing high growth simply because of the growth in the lending business. The core business is becoming very competitive. They (Paytm) have still not turned profitable on the whole. PPB is one vertical which has logged profits.”

— Sandip Sabharwal, founder, asksandipsabharwal.com

The importance of an SFB licence

To be sure, a payments bank cannot lend to customers, issue credit cards, or accept time deposits. While PPB is handcuffed by this rule, an SFB licence would have made Paytm a more rounded financial institution with the muscle of receiving deposits, lend, apart from a captive customer base of more than 25 million merchants who use its platform for hundreds of transactions daily.

“Nobody makes big money in payments and all the payment companies are looking at lending as the holy grail. Not having an SFB licence and not being able to lend directly to customers mean achieving profitability will also be difficult,” says the banker quoted earlier.

In fact, lending has been one of Paytm’s key focus areas. The company disbursed 4.4 million loans with a value close to INR2,200 crore during the third quarter of the current fiscal, representing a growth of around 400%. While the RBI ban does not impact its current loan platform as it only connects lenders with customers, an SFB licence would prove to be a cherry on the cake and allow it to lend directly.

Indeed, the future profitability and growth potential of Paytm revolves around the company getting an SFB licence. For, the overall consumer market is close to being saturated with most smartphone users adopting UPI apps such as PhonePe and Google Pay.

Most of the last few statements issued by Paytm to the stock exchanges have been around the growth of lending that the company has seen in the last few quarters. It is as if that is the only silver lining for the company amidst the intensifying competition.

The company’s “jack of all trades” approach has not impressed the markets. Most revenue streams it promised have not come to fruition apart from lending, which seemed to have gained reasonable traction. But as long as it remains a platform that connects lenders with consumers, its potential to grow big becomes limited.

The way forward

Paytm, which was the biggest IPO in the country’s history, has seen its share price tumble to almost one-third of its issue price of INR2,150. The stock may continue to remain under pressure.

“It is (the ban) a significant negative for Paytm, as it brings to fore corporate-governance issues. After recent issues with BharatPe, Dhani Services, the regulators are likely to look at such fintech companies closer than ever,” says Sabharwal.

“Paytm has been showing high growth simply because of the growth in the lending business. The core business is becoming very competitive. They (Paytm) have still not turned profitable on the whole. PPB is one vertical which has logged profits,” he adds.

Some believe the existing investors may push Paytm to separate its ties with PPB, given the issues surrounding the latter, and of course the discomfort of Sharma holding a 51% stake. But then, it could also lead to another set of problems.

“While existing investors may pitch for a separation of the payments bank from Paytm, but in doing so, the value proposition goes down substantially. Separation might be a short-term fix, but it doesn’t resolve what minority shareholders should be getting out of it,” says Sabharwal.

(Data support by Varsha Santosh; graphic by Manali Ghosh)

The latest from ET Prime is now on Telegram. To subscribe to our Telegram newsletter click here.