Clipped from: https://economictimes.indiatimes.com/wealth/plan/money-mistakes-4-parental-behaviours-that-can-impact-childs-decision-making-ability-as-an-adult/articleshow/87680485.cmsSynopsis

We have identified four main parental behaviours that can lead to financial aberrations among kids. Find out if you are guilty on any count and what you can do to rectify these.

Bengaluru-based software engineer Amit Bhaskaran (name changed) spends erratically on just about everything: clothes, shoes, phones, car accessories. Akshita, his homemaker wife, does not. As the budget goes for a toss every so often, their two kids, aged 10 and 7, are exposed to money arguments between their parents. “When I tell the kids we can’t buy expensive toys, they turn around and tell me that if their dad can buy, they should be allowed to as well,” says Akshita.

This confusion about spending and constant bickering over money may not bode well for the kids, leading to indecision or even wrong money decisions as adults. The inability to take financial decisions either due to confusion or fear of taking wrong decisions is referred to as financial paralysis. While the affliction can spring from a variety of reasons, the impact of parental financial behaviour plays a big role. Any kind of extreme money-related behaviour by parents, be it indulgence, apathy or personal conflict, can create turmoil among kids that manifests in adulthood.

Also read: Digital pocket money: 5 smart cards, app that can help children learn money management skills

“Parents do not give enough cognizance to the way they handle money in front of children, but how they portray it will define the child’s money confidence in future,” says Dr Samir Parikh, Psychiatrist, Director, Fortis National Mental Health Program, Fortis Healthcare.

Sushmita & Yogesh Malhotra, Delhi Saanvi, 13 & Riddhi, 11

“Good education is the only legacy we shall leave our kids, not a big house or other assets.”

Diagnosis: Kids are in good financial health.

Prognosis: They will turn out to be money confident adults.

“While parents assume that children do not understand finances fully, kids are quick to pick up subliminal messages by observing the spending patterns of their parents,” agrees Dr Prerna Kohli, Clinical Psychologist & Founder, MindTribe. “It is likely that the child will become an anxious spender in adulthood if he has seen his parents argue about money, or if he has received mixed messages from his parents, it can lead to overspending even during a financial crisis in adulthood,” she adds.

Gunjan & Jai Sogani, Delhi Pakhi, 13 & Harshana, 10

“We don’t encourage our kids to buy what they want instantly, but wait and look for other options.”

Diagnosis: Kids are being given good financial advice.

Prognosis: Unlikely to suffer from financial paralysis.

To ensure that your children grow into financially confident adults, it is not only important to educate them about finances from an early age, but more significantly, to set the right example though appropriate behaviour and interaction with them. We have identified four main parental behaviours that can lead to financial aberrations among kids. Find out if you are guilty on any count and what you can do to rectify these.

Also read: 3 out of 4 people still keep money idle in savings bank account: Survey

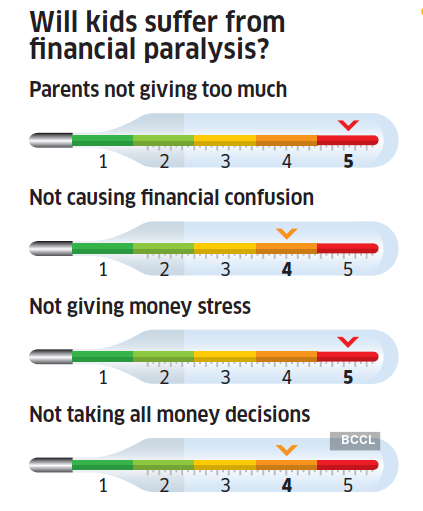

1. When you give your children too much…

It is natural for parents to indulge their progeny, giving them what they want, when they want, and planning an elaborate legacy with property and several assets to bequeath after they are gone. It may not be such a good idea. “Pampering kids and giving them too much affects their aspirations and hunger to grow,” says Parikh. They will not understand the value of money or appreciate how it is earned, and will end up spending it wrongly.

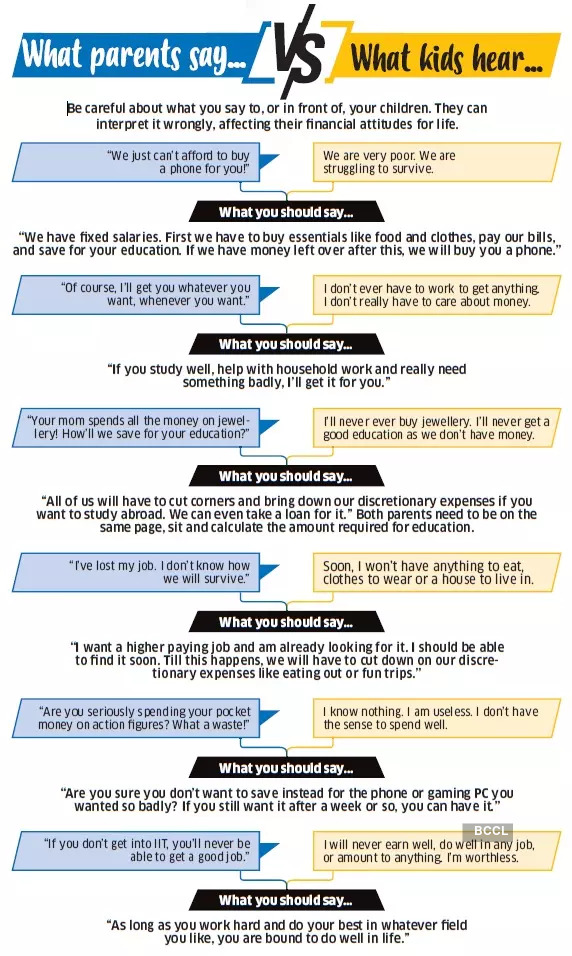

You give kids too much allowance: When you give a large amount as pocket money to the child and supplement it if the money finishes midmonth, you are telling the child that he never has to work hard to earn. When he is forced to do so as an adult, he may be paralysed into inaction or have a problem in career growth and adjustment.

Delhi-based Sushmita Malhotra, who is a resource mobilisation expert, and her banker husband, Yogesh, understand this well. They give Rs 200 a month to Saanvi, their 13-year-old daughter, and encourage her to spend it prudently. “She had saved all her allowance and gift money and wanted to buy sneakers worth Rs 3,000. So I asked her if she had other expenses to take care of, would she spend the entire amount on shoes,” says Sushmita. Saanvi scaled down her budget to Rs 2,000. While it is all right to guide the child, do not interfere too much. Give an age appropriate allowance and allow the kid freedom to make his own spending decisions and manage his money so that he can learn from his mistakes.

You fulfil their wants instantly without delay: If you do not prolong and give everything the moment a child asks for it, it can not only lead to frustration but also career problems as an adult. “The child will not want to work even for his needs in adulthood because he will assume it will somehow come to him. When it doesn’t, it can lead to depression and career problems because he will not be able to adapt in any work organisation,” says Parikh. This is the reason that Gunjan and Jai Sogani do not believe in instant gratification and encourage their two kids to wait for a few days, make a list, prioritise and explore all avenues, before buying what they want. “Pakhi, my 13-year-old daughter, wanted to buy books for Diwali from Amazon for `1,000. I asked her to wait and check other websites. She eventually found cheaper options on Flipkart,” says Gunjan.

You plan to leave behind too many assets: If you have a house and other assets, you cannot prevent their transmission to kids, but don’t go out of the way to acquire these. If there is too much on the kid’s platter, he will refuse to work for a living and fail to explore investing options on his own. Instead, provide the kids the best education and allow them to fend for themselves. “If you can’t avoid leaving assets, it’s important to teach the children how to manage these,” says Mrin Agarwal, Founder & Director, Finsafe India.

2. When you cause financial confusion

When there is a conflict in parenting parents regarding the child’s habits or goals, or parents do not practice what they preach, or even force the kid to accept their investing habits, the child can face a dilemma that lasts into adulthood. If a child is not sure what to do as an adult, he invariably ends up doing nothing, especially when it comes to saving or investing.

You force your financial beliefs on chidlren: “Most of the financial dilemmas children face as adults are due to the differing investing beliefs and earning capacities of their parents,” says Dinesh Rohira, Founder & CEO, 5nance.com. “This limits their wealth growth when they start earning. A child, who has been exposed by his parents to the fixed deposit culture, will find it difficult to invest in equity,” he adds. He may not want to buy a house or invest in crypto currency, but will hesitate in doing either. “Most of the youth today refuse to invest in liquid funds, letting the money idle in a bank account, because their parents have not had any exposure to mutual funds,” says Rohira.

Both parents are not on the same page: Even if there are differences in financial habits or attitudes among parents, make sure you put up a united front, instead of expressing opposing views, while dealing with kids. If one of the parents refuses to buy an expensive toy or gadget for the child, but the other parent goes ahead and buys it instantly, the child will learn to be manipulative. More importantly, he may end up being financially indecisive, or an extreme spender or saver as an adult, because he will not know which is the better option. “Any extreme opposing behaviour by parents confuses the child and he doesn’t understand which way to go. The growth of child in terms of mental make-up and confidence about money goes down,” says Parikh.

You teach them one thing, but do another: “Sometimes kids overhear their parents talking to accountants about evading GST or income tax. They are either passing on negative behaviour or sending mixed signals to the child because a kid cannot tell the difference between right and wrong,” says Rohira. Similarly if you are refusing to buy your teen a phone because it is expensive, but buy a costly one for yourself, you are passing on the message that either saving is not as important as you make it out to be, or that as a parent you can do whatever you want and spend at will. Be sure to practice what you preach because children learn more by observing you than through your sermons.

3. When you give them money stress

Financial anxiety that is passed on by parents to their kids, knowingly or unknowingly, is another cause of paralysis in adulthood.

You argue about money in front of kids: If parents have opposing money personalities—spender versus saver or risk taker versus conservative investor— there is bound to be conflict. Remember, however, not to expose your child to bitter arguments and preferably do it when kids are not around. Fights over finances can make the child resent money and avoid all financial decisions as an adult. “Besides arguing about money in front of your child may make him insecure about himself and he may learn not to vocalise his needs to maintain harmony. If the argument has taken place, ensure that you explain to the child that couples can disagree sometimes and comfort your child,” says Kohli.

You take on too much debt and can’t repay: These days many parents prefer living off loans, buying everything on EMIs and maxing out their credit cards, while others may have to take loans for their businesses or homes. If you are unable to repay the debt and are hounded by creditors, it can cause anxiety and behavioural problems among kids. As adults they may either rebel and swear off loans even if it is needed or simply may follow in their parents’ footsteps and ruin their finances. So either keep your debt to the minimum so as not to expose kids to unnecessary anxiety, or explain it to them about how you are taking steps to repay.

You don’t explain or talk about financial crisis: Lack of communication about financial problems with kids can translate into latent anxiety and confusion which can result in financial paralysis in later life. Whether it is job loss, salary cut or any other crisis, most people don’t talk to their kids thinking it best to keep them out of their problems, or perceiving them to be too young to understand or deal with it. However, kids are quick to pick their own ways. They could feel guilt at not being able to help or see money as a problem that needs to be avoided as an adult. The best option is to sit with them and explain the situation and how you are planning to deal with it. Make it clear that you do not expect them to solve the problem, only to help the best they can by cutting down expenses like eating out or forgoing holidays. This will cut down their stress and make them feel involved.

4. When you take all the decisions

“When parents take all the financial decisions, they create a superficial sense of responsibility which will later lead to lack of financial accountability,” says Kohli. So it is important to support your child’s financial decisions without rescuing them.

You don’t allow them to use pocket money as they want: When you give your child pocket money, by all means lay down some guidelines on spending, but after that make sure you allow them the freedom to make their purchase choices. If you constantly criticise or override the child’s decisions, it will take away his confidence and self-esteem, which might reflect as financial paralysis in later life.

You choose their career for them: If you force your child to select a career for its earning potential, not the one he has a flair or interest in, he will either lose the confidence to take decisions as an adult, or rebel and refuse to take any decisions altogether. He may even resent the money he makes from a lucrative profession he has no interest in, and give it up.

You don’t tell them about various investing options: Since most children don’t have any knowledge about investing, they blindly depend on their parents to save and invest their money. “Since parents have taken these decisions as per the choices available decades ago, these may not be valid in the current scenario,” says Rohira. Consequently, these may not help them achieve their goals or meet their requirements and cause resentment. If parents do not have requisite knowledge, they should hire financial advisers to know about the latest investing options. When the child observes his parents taking help and looking for information, he is more likely to do the same as an adult to avoid confusion.