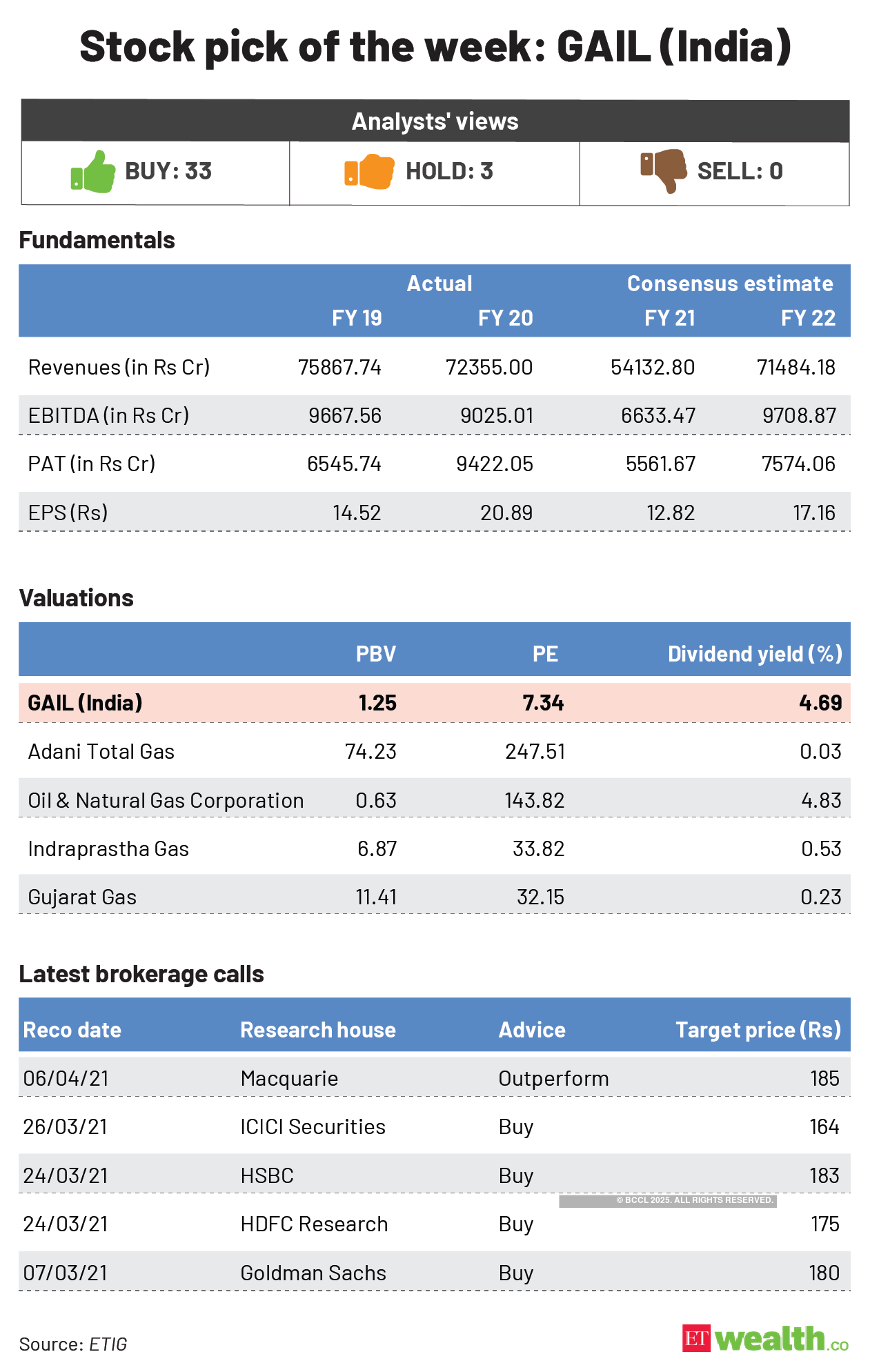

SynopsisGail is in the process of implementing several pipelines. Since 70% of its revenues come from three main pipelines, divestment of any of them through the InvIT route which government is planning to do, will result in company’s rerating. This has made the company a favourite of analysts.

Natural gas distribution company Gail reported only muted numbers for the first three quarters of 2020-21, mostly because of the Ebitda (earnings before interest, tax, depreciation and amortisation) loss by its gas trading division. However, things improved in the fourth quarter with increase in spot LNG prices. Year 2021-22 is expected to be brighter for Gail due to operational improvements across divisions. After remaining at very low levels, international crude oil prices have started stabilising around $ 60 per barrel. Going forward, petrochemical and LPG prices are also expected to remain stable at higher levels and this will help Gail to report high margins. In other words, higher crude price is a positive for its LPG as well as petrochemical divisions.

To satisfy the domestic natural gas demand jump, Gail is in the process of implementing several pipelines. Its Kochi-Mangalore pipeline was commissioned in November 2020 and has started supplying 0.8mmscmd of gas to Mangalore Chemicals and Fertilisers. Transmission volume from this pipeline will jump once the link to Bengaluru is completed. The commissioning of new pipelines along with increased availability of natural gas is helping Gail to increase its transmission volumes. Analysts expect the transmission volumes to increase by 7% CAGR between 2020-21 and 2023-24.

The proposal to include natural gas under GST is pending for some time and implementation of the same will be beneficial for the sector in the long run. Since users can claim input tax credit, this move will reduce their effective cost, thereby increasing the natural gas demand from industrial users.

The government has been taking bold steps to generate funds for infrastructure by monetising assets like highways, gas pipelines, etc through infrastructure investment trusts (InvITs). Since 70% of its revenues comes from the three main pipelines, divestment of any of them through the InvIT route will result in Gail getting re-rated. Additional fund inflow through this route will also help Gail take up other gas pipeline projects.

Last month’s underperformance in this counter was due to technical reasons– like exclusion of Gail from Nifty from 31 March 2021–and therefore, long term investors should use it as an opportunity to get in. In addition to its core value, investors should also consider Gail’s investments in companies like Petronet LNG (12.5%), Indraprastha Gas (22.5%) and ONGC (2.45%).

Selection methodology: We pick up the stock that has shown the maximum increase in “consensus analyst rating” during the last one month. Consensus rating is arrived at by averaging all analyst recommendations after attributing weights to each of them (i.e., 5 for strong buy, 4 for buy, 3 for hold, 2 for sell and 1 for strong sell) and any improvement in consensus analyst rating indicates that the analysts are getting more bullish on the stock. To make sure that we pick only companies with decent analyst coverage, this search will be restricted to stocks with at least 10 analysts covering it. You can see similar consensus analyst rating changes during the last one week in ETW 50 table.

Graphics by Sadhana Saxena/ET Prime