Synopsis

To incentivise foreign currency inflows, the Reserve Bank of India will swap fresh dollar term deposits raised until end-September at par. In effect, the RBI will bear the entire hedging cost on deposits mobilised under the Foreign Currency Non-Resident (Bank), or FCNR(B), scheme. In line with the RBI’s expectations, banks are passing on almost the entire benefit to depositors, making these deposits more attractive.

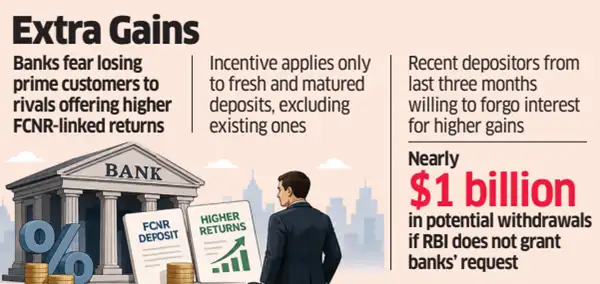

MUMBAI: Commercial banks have sought approval from the banking regulator to allow existing non-resident Indian customers to prematurely withdraw and rebook deposits to take advantage of the time-bound FCNR deposit scheme, which in some cases offers almost double the returns of regular term deposits.

Some large depositors are instructing their banks to prematurely close term deposits and redeploying the funds in other banks, bankers said.

Banks are offering between 6% and 7.1% for three- to five-year deposits under the special scheme, compared with 3.35% to 4% previously.

“Some of our prime depositors are moving to other banks…In the long run, we may lose our relationship with these customers,” said a banker cited above.

To incentivise foreign currency inflows, the Reserve Bank of India will swap fresh dollar term deposits raised until end-September at par. In effect, the RBI will bear the entire hedging cost on deposits mobilised under the Foreign Currency Non-Resident (Bank), or FCNR(B), scheme. In line with the RBI’s expectations, banks are passing on almost the entire benefit to depositors, making these deposits more attractive.

Banks seek RBI nod on Guarantee Rule to boost NRI deposit inflows

However, the RBI has said that its incentive is applicable only to fresh and matured deposits. That means existing deposits will continue to earn lower rates.

“Those who have created deposits in the last two to three months are the most aggrieved, as they are missing out on better returns,” said a banker. “We are buying time from them, hoping the RBI will agree,” he added.

The RBI did not respond to ET’s request for comment.

Under RBI rules, FCNR(B) deposits have a lock-in period of one year, and interest is forfeited if they are withdrawn before that. If deposits are prematurely withdrawn after one year, banks deduct one percentage point from the contracted rate.

HDFC Bank extends Keki Mistry’s interim chairman tenure by three months

Depositors who placed funds in the last three months are willing to forgo interest income, as the benefits outweigh the costs.

Bankers said they do not have the authority to prevent depositors from prematurely withdrawing funds if they are willing to forgo interest. They expect nearly $1 billion of withdrawals if the RBI does not approve premature withdrawal of deposits placed over the last three years.

Under the RBI scheme, the FCNR deposits should be in multiples of $1 million and will have a lock-in period of one year. While banks are permitted to take deposits in any foreign currency, the RBI will swap them with banks only in US dollars.

(Join our ETNRI WhatsApp channel for all the latest updates)

…more