The Indian diaspora, people of Indian origin living outside India, is approximately 35 million strong. This includes people who are non-resident Indians and people of India origin who are citizens of other countries.

Most of them have families and links in India. They send money back to India for their family maintenance expenses, to save and to invest.

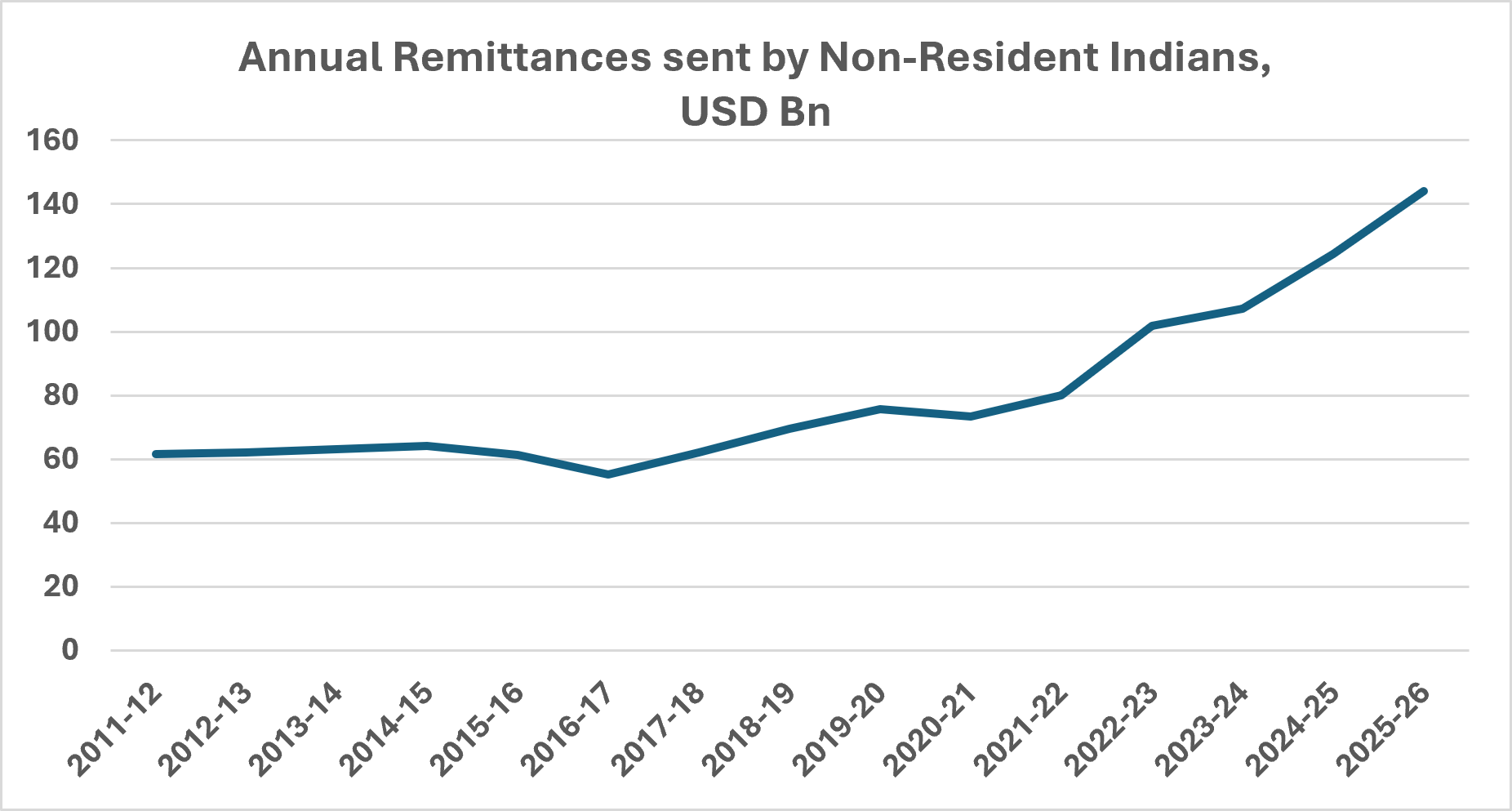

As the number of Indians migrating abroad has increased, so has the amount of money they send back every year. India is the world largest recipient of remittances sent by overseas Indians.

India received ~USD 140 billion in remittances in Fiscal Year 2026, a number which has gone up steadily over the years.

Over and above the remittances, the Indian diaspora sends money as deposits. India receives ~USD 15 billion in Non-Resident Indian Deposits (NRI) Deposit net flows annually. The outstanding balances on NRI Deposits was ~USD 165 billion.

The Indian Diaspora is seen as one of India’s soft power of people, talent, culture and the ability to influence India’s interests in the global arena.

STORIES YOU MAY LIKE

But as we have seen above, the same soft power also brings in crucial ‘hard’ currency back to India. Remittances and Deposits and Indian IT services exports is what keeps our current account deficit manageable.

When India faces a ‘currency crisis’ – sharp depreciation of the Indian Rupee against the US Dollar and a depletion in India’s foreign exchange reserves – the Indian government and the Reserve Bank of India opens up a facility to tap non-resident Indians for more inflows.

India Development Bonds, 1991 – to manage the Balance of Payment crisis

Resurgent India Bonds, 1998 – to manage sanctions post Pokhran Nuclear test

India Millennium Deposits, 2000 – to manage the balance of payment deficit

FCNR Swap Window, 2013 – to shore up Forex Reserves and stem rupee depreciation.

The 1998 and 2000 series raised between USD 4-5 billion in a span of 2weeks to 2 months. A sizeable sum of foreign exchange during those times.

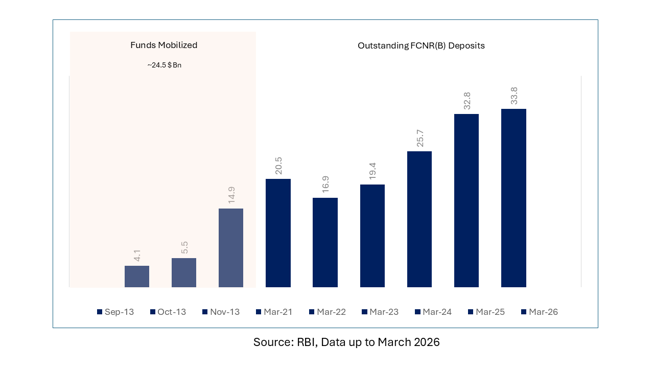

The 2013 Foreign Currency Non-Resident (FCNR) swap window raised ~USD 26 billion over 2 months between September and November 2013. A large amount driven by low global interest rates, a 3.5% swap subsidy, and a provision of a letter of credit by the Indian banks to foreign banks to provide leverage to non-resident Indian depositor.

The strength of India’s diaspora and the ability to tap it is why we do not think India suffers from a ‘currency crisis’.

However, we are in a situation where foreign capital flows have been negative, and the Indian currency has depreciated against global currencies. Please read.

The Reserve Bank of India and the Government have responded with three measures, with the major one being a redux of the 2013 FCNR Swap Window. Market economists estimate between USD 50 -70 billion in eventual inflows.

#1 FCNR Deposit Subsidy

The RBI will bear the cost of hedging (~3-3.5%) the USD/INR depreciation risk on this deposit. This would result in the India Bank offering a higher $ deposit rate to the NRI. FCNR $ deposits rates for above 3 years being quoted by Indian banks have risen from ~3-3.5% to ~6%-7%.

On its own, a 6% 3-year Deposit at a time when $ interest rates are >4%, doesn’t seem as attractive. This is tax free in India, but the NRI may have to pay tax in home country. Also, return expectations in todays day and age due to assets like bitcoins, AI, chip stocks, meme coins, prediction markets, are a lot higher than in 2013.

ALSO READ

For the ultra/high net worth NRI to make high single digit/low double digit post tax returns, assuming their borrowing cost for the leverage will cost ~5%, the leverage needs to be above 5-10 times for the facility to attract large inflows. If so, this scheme can garner, USD 20-40 billion as per estimates by end September 2026.

#2 PSU Overseas borrowing

The RBI is offering a subsidy on hedging cost to Public Sector Undertakings (PSUs) to borrow overseas. With this, PSUs may be able to offer >6%$ yields on their bond issuances which makes it a bit more attractive than current Investment grade Emerging market $ bond yields on offer. We estimate this could raise between USD 5-15 billion over time.

The impact of these two schemes would be seen in India’s corporate bond market. We have already seen near maturity corporate bond yields fall by 25-50 basis points since the announcement.

#3 Removal of Witholding taxes and capital gains on Indian bonds

The government announced this last week along with relaxation in ownership limits (something we have argued earlier) This seems to be done with a view to get Indian government bonds included in the Bloomberg Global Aggregate Bond Index.

This will indeed be a huge move as this index is the most widely used benchmark for both passive and active global fixed income funds. Even a 1% weightage can trigger substantial passive and active flows.

However, we would caution that index inclusion, if at all, happens over a staggered protracted period of time and eventual flows could take over a 12-24 month period. The index review is slated for June/July 2026.

ALSO READ

The current account deficit is expected to range between USD 40 – 80 billion given various estimates of oil prices. That is the extent of capital inflows required to fund the deficit and stabilize the currency.

In the next 3 months the major aspect to watch would be the FCNR Deposit flows and PSU bond offerings. If it is indeed more than USD 25 billion, it will have an impact on the currency, bond markets, and the balance of payment situation. It will also improve the sentiment on the Indian rupee.

We would also hope for foreign capital outflows to revive if the currency outlook improves due to these inflows and if the West Asia conflict sees a resolution.

Arvind Chari is a Chief Investment Strategist and has been with Quantum Advisors India group since 2004. Arvind has over 20 years of experience in long-term India investing across asset classes. Arvind is a thought leader and guides global investors on their India allocation.

This article is for educational and discussion purposes only and is not intended as an offer or solicitation for the purchase or sale of any investment in any jurisdiction. No advice is being offered nor recommendation given and any examples are purely for illustrative purposes. The views expressed contain information that has been derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness, or reliability of the information.

The views and opinions expressed in this article are my personal views and should not be construed of the Firm. There is no assurance or guarantee that the historical result is indicative of future results, and the future looking statements are inherently uncertain and cannot assure that the results or developments anticipated will be realized.