Clipped from: https://taxguru.in/income-tax/extra-0-massive-tax-demand-itat-pune-rescue-army-jawan.html?utm_source=follow.it

Naveen Nath Vs ITO (ITAT Pune)

The Pune ITAT granted relief to an Indian Army jawan whose income was wrongly assessed at ₹45.27 lakh merely because his tax consultant accidentally typed an extra “0” while filing the return. The assessee’s actual salary as per Form 16 and Form 26AS was only ₹4.67 lakh, but the return reflected salary income of ₹46.77 lakh due to a clear typographical error.

The Tribunal noted that even senior army officers were not drawing such salary during the relevant year and observed that the mistake was obvious from the records themselves. The Revenue also fairly accepted that it was a genuine error.

Interestingly, the CIT(A) had dismissed the appeal on a mere technical defect in Form 35, without addressing the glaring factual mistake. The ITAT criticised this approach and held that substantive justice cannot be denied over technicalities.

Accepting the assessee’s plea, the ITAT directed the AO to compute income at ₹4,67,790 instead of ₹46,77,900, thereby deleting the absurd tax demand raised merely because of a clerical mistak

FULL TEXT OF THE ORDER OF ITAT PUNE

This is an appeal filed by the Assessee against the order of ld.Commissioner of Income Tax(Appeal)[NFAC], passed under section 250 of the Income Tax Act, 1961 for the A.Y.2018-19dated 26.08.2025 emanating from the Assessment Order passed under section 143(1) of the Act, dated 23.10.2019. The Assessee has raised the following grounds of appeal :

“1. The Ld. Deputy Commissioner of Income Tax, CPC, Bangalore (AO) without going into the facts has assessed the income of the appellant at an income of 45,27,900.00.

2. The Ld. AO missed to note and failed to appreciate that the Consultant of the Appellant while filing return of income due to typographical error had inadvertently punched another “0” in the return of income.

3. The Ld. AO completed the assessment at an income of ₹ 45,27,900.00 without caring to cross check that the Appellant is a jawan in the armed forces and cannot have salary of this amount.

4. The Ld. AO missed to cross check the income returned without cross checking the same from the data available with the Income Tax Department.

5. That the impugned order is bad in law and not in consonance with facts, and against the principles of natural justice.

6. Besides the above grounds the appellant craves to leave, add, alter, amend, and/or to modify any Grounds of Appeal, in the circumstances of the matter.”

Submission of ld.AR :

2. Ld.AR for the Assessee appeared virtually. Ld.AR filed a paper book by post which was received by Office of the Assistant Registrar, ITAT Pune on 18.11.2025. The relevant written submission filed by the ld.AR is reproduced here as under :

“Background of the Case:

In pursuance to the order issued by the Deputy Commissioner of Income Tax, CPC, Bangluru under section 143(1) dated 23-10-2019, where due to an addition of 42,10,200.00 U/s 69A of the Act, a sum amounting to 14.94.820.00 by way of demand had come into existence. The details in respect of order is being enclosed for the kind reference of Your Honor

“Order Copy U/s 143(1) is enclosed.”

Being aggrieved the appellant filed appeal before the Ld Addit Commissioner of Income Tax Appeals-2, Hyderabad (CIT-A) where the appeal was heard and dismissed and the addition was sustained vide order dated 26-08-2025. The details in respect of order is being enclosed for the kind reference of Your Honor

“Order Copy U/s 250 is enclosed”

The facts of the case are as under, The appellant is an individual working in the Armed Forces of India as a Jawan being neither an officer of a JCO enjoying income primarily from salary. The appellant not being very qualified academically takes services of a tax practitioner to file his return of income as the appellant neither has a computer system nor has access to a computer system.

The appellant on receipt of Form 16 from his employers approached the tax practitioner to file his return of income, the copy of Form 16 is being placed in this paper book for the kind consideration of the Hon’ble Bench where salary income was 4,67,790.00. The Tax practitioner or Consultant filed his return of income by punching salary as 46,77,900.00 as another ‘0’ was punched while filing return of income and CPC Bangluru without any cross verification intimated assessment at an income of 45,27,900.00 after giving deduction under Chapter VI A of the Act as a result excess income of the appellant was assessed and thus aggrieved the appellant is before Your Honor in appeal.”

Submission of ld.DR :

3. Departmental Representative(ld.DR) for the Revenue fairly accepted ld.AR’s contention that there has been a typographical error by the Assessee while filing Return of Income.

Findings & Analysis :

4. We have heard both the parties and perused the records. In this case, Assessee had filed Return of Income for A.Y.2018-19 on 04.07.2018. Order under section 143(1) was passed on 23.10.2019 raising the substantial demand of Rs.14,94,820/-. Aggrieved by the order, Assessee filed appeal before ld.CIT(A). Ld.CIT(A) dismissed the appeal of the assessee stating that Assessee has referred incorrect date in the Form No.35, thus, ld.CIT(A) has dismissed the appeal of the Assessee on mere technicality.

4.1 Aggrieved by the order of the ld.CIT(A), Assessee has filed appeal before this Tribunal.

5. In this case, the Assessee is serving in Indian Army. At that point of time, he was at Artillery Centre, Nashik. It has been submitted by ld.AR that due to the nature of assessee’s service, Assessee was posted at different parts of the country at various times. Ld.AR further submitted that Assessee is not well-versed with Income Tax Rules and Procedures.

6. In this case, Assessee filed Return of Income for A.Y.2018-19 on 04.07.2018 under section 139(1) of the Act. Copy of the said return of income has been filed in the paper book.

7. It has been submitted by ld.AR for the assessee that Assessee’s Tax Consultant who filed assessee’s return of income erroneously typed “one zero extra” in the column “Income from Salary”. Ld.AR therefore, submitted that the Salary shown is Rs.46,77,900/-. Ld.AR further submitted that during F.Y.2017-18, even the highest ranked army officer was not drawing such high salary. Thus, it is a clear mistake on the part of the Assessee’s Tax Consultant.

8. We have perused the Return of Income filed by the Assessee, Copy of Form No.16 and 26AS of the Assessee with the help of ld.DR for the Revenue.

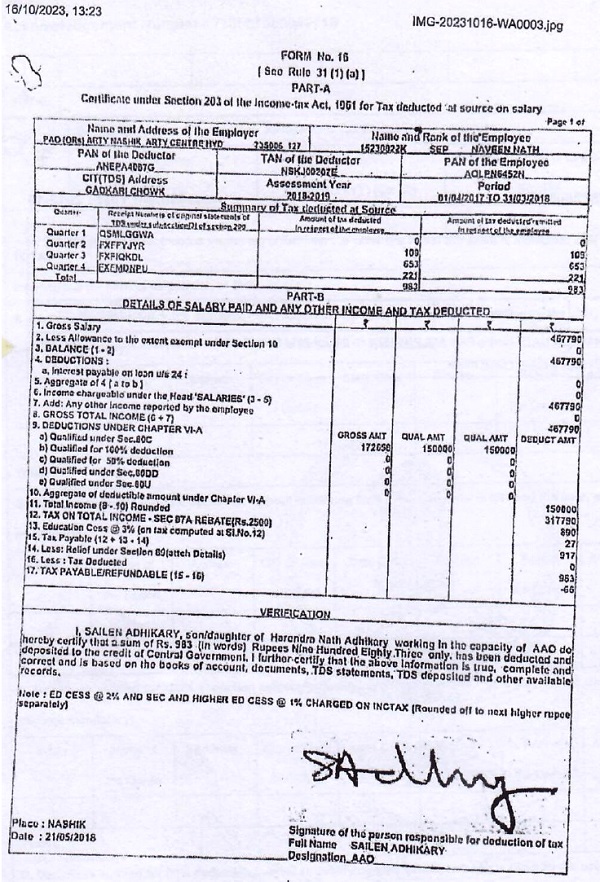

9. It is observed that Form No.16 which is issued as per Rule 31 of the Income Tax Rules has been issued by PAO Artillery Nashik. The Salary Income shown in the Form No.16 is only Rs.4,67,790/-, whereas Income from Salary in the Return of Income is Rs.46,77,900/-. The Form 16 is scanned and reproduced here as under :

10. We have verified Form 26AS issued by Income Tax Department and the Salary appearing in Form 26AS is Rs.4,67,790/-only. Thus, it is absolutely clear that Salary of the Assessee was Rs.4,67,790/- as per Form 16 issued by a Government of India’s Authority and Form 26AS issued by Income Tax Department. However, in the Return of Income under the Head Salary, the Salary shown is of Rs.46,77,900/-. Ld.DR also accepted that it’s a typographical mistake on the part of the assessee.

11. We are also convinced that it is a typographical error while filing the Return of Income. In these facts and circumstances of the case, we direct ld.Assessing Officer to consider the gross total income of the Assessee at Rs.4,67,790/- instead of Rs.46,77,900/-, calculated in the order u/s.143(1) of the Act. Accordingly, grounds of the appeal raised by the Assessee are allowed.

12. In the result, appeal filed by the Assessee is allowed.

Order pronounced in the open Court on 13 February, 2026.