Clipped from: https://www.thehindubusinessline.com/opinion/new-credit-loss-norm-could-hurt/article70925762.ece

The ECL rules risk exclusion of capable, asset-light borrowers — favouring weaker borrowers with collateral

For decades Indian banks managed bad loans under the Incurred Loss (IL) approach. Banks provisioned only after borrowers actually defaulted. The Reserve Bank of India is changing the Asset Classification, Provisioning, and Income Recognition norms. From April 1, 2027, banks must shift to the Expected Credit Loss (ECL) framework, from backward-looking IL model.

The RBI is asking lenders to anticipate crashes before they happen. Loans will be classified into three stages based on extent of credit deterioration. Stage 1 category (performing assets, no significant increase in credit risk) requires provisions for expected losses over the next 12 months. Stage 2 (performing assets with significant increase in credit risk but not credit impaired) and Stage 3 (non-performing or credit impaired) categories require lifetime loss coverage.

ECL uses three variables: Exposure at Default (EAD), Loss Given Default (LGD), and Probability of Default (PD). Together, they estimate not just current stress, but future vulnerability. This new rule retains the existing norms for classifying non-performing assets (i.e., 90-days overdue), complemented by the banks’ assessment of any forward looking credit risk requiring additional provision. For example, Stage 1 identification or the shift from Stage 1 to Stage 2 can occur irrespective of the current 90-day overdue norm. Therefore, credit risk could be triggered by 30+ days past due (rebuttable), rating downgrades, borrower stress, or portfolio-level signals.

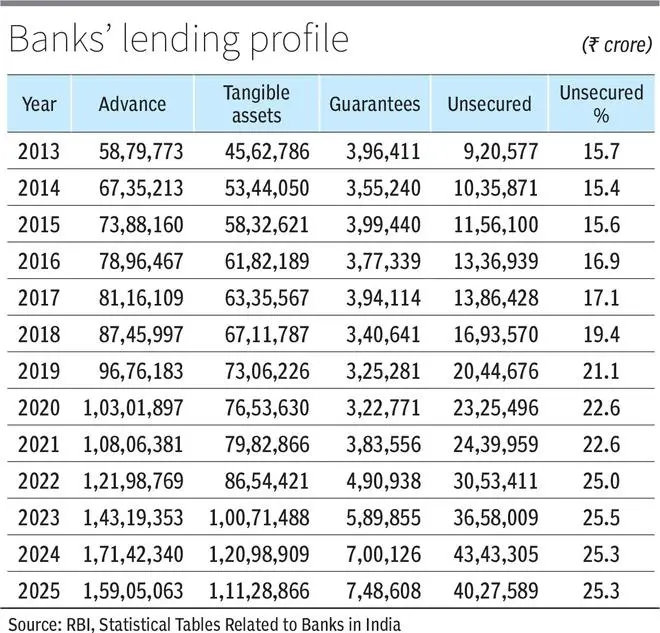

Prudent ECL creates a policy dilemma: does systemic resilience come at the cost of credit rationing? As of March 2025, Indian banks held net advances of ₹15,905,063 crore, of which, around 75 per cent are secured by collateral or guarantees, leaving 25 per cent unsecured (see Table). On paper, this appears comfortable. In reality, collateral values often collapse during systemic stress due to fire-sale effects, where assets cannot be liquidated near book value. This weakens recovery rates and raises Loss Given Default (LGD).

Once banks lose confidence in collateral recovery, they tighten lending, not because borrowers are weaker, but because security becomes unreliable. Unsecured advances rose from 15.7 per cent in 2013 to 25.3 per cent in 2025, lowering recovery rates and thereby increasing ECL provisioning pressure. Now the question remains: will this potential increase in provisioning trigger credit rationing?

When banks demand collateral to reduce unsecured exposure, borrower behaviour creates a natural self-selection. Safe borrowers, confident of repayment, are willing to pledge assets, while riskier borrowers avoid collateral because they expect a higher chance of default. Under ECL, this sorting becomes sharper. Since banks must account for LGD from day one, unsecured loans carry a much higher immediate provisioning burden. As a result, banks may simply avoid offering unsecured credit altogether.

In credit markets, when demand exceeds supply, interest increase fails to clear the market, due to the Stiglitz-Weiss Theory. Under this, if a bank tries to “price in the risk” of an unsecured loan by charging a 20 per cent interest rate, the “safe” borrowers who have low-margin, low-risk projects leave the market because the cost eats their entire profits. “Risky” borrowers remain because they only plan to pay if their high-stakes project succeeds. The bank knows that it is left with a Akerlof’s “lemon” pool of borrowers. To avoid this, the bank keeps interest rates lower than the market-clearing level and simply refuses to lend to everyone who wants money i.e., rationing. Banks stop lending to anyone who does not have “excessive” collateral. Raising interest rates worsens borrower quality, so banks manage risk by restricting access to credit rather than increasing prices — this is credit rationing.

Risky borrowers also affect the Probability of Default component of ECL. As Stiglitz and Weiss argued, beyond a point, higher interest rates attract mainly high-risk borrowers, making price a weak risk-control tool. Under ECL, loans to such borrowers trigger higher projected PD, especially during economic slowdowns. The resulting provisioning burden may exceed what banks can recover through higher interest income. This may push banks to tighten credit standards rather than simply raising interest rates as price increase hurts quality.

Probability of default

The real shift in ECL is moving from “what happened” to “what might happen.” Banks must incorporate macroeconomic variables into PD models. If PD estimates are highly sensitive to interest rates or sector stress, even a small shock can push loans from Stage 1, requiring only short-term provisioning, to Stage 2, where lifetime expected losses must be recognised. To avoid this jump, banks may stop lending to sectors showing early signs of weakness.

While ECL may push banks towards safer, collateral-backed lending, it also raises a deeper question: should access to credit depend on true repayment capacity or simply on asset ownership? ECL creates a forward-looking system that prices risk more transparently and reduces the chance of sudden systemic shocks. However, ECL risks exclusion of capable but asset-light borrowers, while favouring weaker borrowers with strong collateral.

A promising entrepreneur without property may be denied credit, while a mediocre borrower with real estate gets funded. The risk of credit rationing is real, but ECL is not a threat to growth by itself. Its success will depend on how well banks use data and how effectively RBI’s five-year transition period helps balance prudence with credit access.

Bhusan is Professor of Practice at TAPMI Bengaluru, Basu is Professor at IIM Bangalore, and Jeet is PhD Scholar at IIM Ranchi

Published on May 1, 2026