Credit growth in the system has touched a decade high, a level seen last in 2011

The decadal high credit growth amid slow deposit accretion and tight liquidity conditions have meant that banks are drawing down their high-quality liquid assets (HQLAs) to fund the demand for credit in the economy, the Reserve Bank of India’s (RBI) Financial Stability Report said.

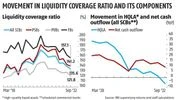

This is evident from the fact that the liquidity coverage ratio (LCR) has come down from a high of 173 per cent as of September 2020 to 135.6 per cent as of September 2022. It, however, still remains comfortably above the minimum regulatory requirement of 100 per cent.

Incidentally, the LCR of private banks have fallen more than public sector banks and foreign banks. Private banks saw their LCR drop to 121.8 per cent as of September 2022, while for public sector banks, it dropped to 141.2 per cent. Foreign banks have relatively high LCR at 157.1 per cent as of September 2022.

In banking parlance, LCR refers to the proportion of HQLAs held by banks, to ensure their ability to meet short-term obligations. HQLA is essentially cash or assets that can be converted into cash quickly through sales (or by being pledged as collateral) with no significant loss of value.

According to the RBI data, bank credit has grown at 17.4 per cent year-on-year (YoY) as on December 16, 2022 while deposits growth moderated to 9.4 per cent during the same period.

The credit growth in the economy has been broad-based across geography, economic sectors, population groups, organisations, types of accounts and bank groups, RBI said. Also, private banks have logged better credit growth figures than their public sector counterparts.

Credit growth in the system has touched a decade high, a level seen last in 2011. However, the lagging deposit growth is increasingly becoming a concern for the banks as they scramble to garner liabilities to meet the credit demand in the economy.

Analysts in the past have indicated that the slower pace of deposit growth may become a constraint in loan growth, going forward.

However, the current growth has to be seen in the context of base effect also. For the last two years of the pandemic, credit growth in the economy averaged at 6 per cent YoY while deposits grew at 11 per cent YoY.

Going forward, analysts expect a combination of factors, including the RBI’s rate hikes, slowing GDP growth, and the normalisation of the base effect to blunt the sharp growth in credit. Meanwhile, with banks scrambling to garner deposits, thereby raising deposit rates, will ensure that deposit growth will pick up pace, and the gap between credit and deposit growth will narrow.