Currently, non-fossil or clean sources make up around 25 per cent of energy and 40 per cent of the installed power base in the country

The renewable energy (RE) sector has received tailwind from India’s renewed international commitments under its Nationally Determined Contribution (NDC) targets this year, which reflect the country’s determination to go clean and green, and source as much as 50 per cent of its power from non-fossil fuels by 2030.

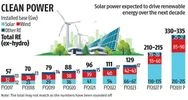

Currently, non-fossil or clean sources (hydropower, nuclear, solar, wind, and other renewables) make up around 25 per cent of energy and 40 per cent of the installed power base in the country, having grown rapidly from 19 per cent and 33 per cent, respectively, in FY17, supported by an addition of 51 gigawatt (Gw) of renewable capacity since, as of FY22 end.

Policy support has been a key driver for enabling growth and has constantly evolved and adapted to the changing requirements and dynamics of the power sector.

For perspective, the initial years from 2012 to 2017 were aimed at incentivising lower costs/pricing of the segment via feed-in tariffs, direct subsidies in the form of viability gap funding, and operational support through payment security mechanisms initiated by nodal agencies.

With tariffs successively breaching new lows in the solar segment in fiscal 2018, subsidy enablers were discontinued, and the government shifted its focus to removing resource bottlenecks. This has since led to the government focusing on solar park development (34 Gw approved as of December 2021), grid infrastructure planning for clean energy integration (Green Energy Corridor), and the rooftop segment, through renewed policies for adoption. This helped accelerate additions post 2017, with 75 per cent of the 51 Gw added between FY18 and FY22, despite the pandemic in 2021.

The focus currently is on ensuring holistic integration of renewables into the power system, by balancing the intermittency inherent in renewables with storage and adequate grid capacity, coupled with enabling relatively scalable clean sources such as hydro.

This is evident from the increased tendering of new operational structures such as mixed-resource renewable projects, round-the-clock offerings, and projects that guarantee supply during peak power demand.

CRISIL expects such tenders to form almost 10 per cent of the solar utility base by fiscal 2027, considering current pipelines. These models, coupled with standalone storage projects being developed by nodal agencies and private-sector developers, will help integrate renewables in large capacities into the power system.

The reserve margin indicator which indicates the power supply buffer over peak demand requirements shows that 15-20 GW storage would be necessary by fiscal 2027 to balance the current expected additions of 100-110 GW of renewables between fiscals 2023 and 2027. This is supported further by the government’s focus on reforms in state power distribution utilities, which, though a separate segment of power, is impactful in terms of revenue generation for power generators.

According to the data released for July 2022, dues to RE generators comprised almost 20 per cent of the total dues to all types of power generators [Source: PRAAPTI]. This has started to come down gradually, with the centre pushing discoms to pay off pending receivables under the dues-based instalment scheme, coupled with reform targets aligned to the Rs 3 trillion distribution reform package launched in 2022.

These policy enablers, coupled with sustained elimination of resource bottlenecks (ISTS connectivity targeted schemes, solar parks, expansion of the Green Energy Corridor scheme), provide comfort on renewable energy adoption over the next decade – till fiscal 2030.

CRISIL MI&A Research expects 220-230 GW of renewable (solar, wind, and other renewables) and around 240-250 GW of total non-fossil fuel capacity additions till 2030, supported by storage capacity of 55-60 GW. This would take the share of non-fossils to 45-50 per cent in energy and 58-60 per cent in capacity terms (including storage), nearing the NDC targets by the end of the decade.

Apart from policy, the sector will need to be supported by continued investor interest, low cost of capital, and supply chain efficiencies to ensure sustained momentum.

The credit outlook on the renewables sector is expected to remain ‘stable’ backed by conducive regulatory environment, expected release of receivables from state discoms and increased capacity base. Regulatory environment is expected to be reasonably supportive for the sector as seen from recent announcements around increased capacity targets and steps to further domestic green bond market.

Cash flows for renewable players are expected to ramp up driven by release of stuck receivables from state discoms following Liquidated Payment Scheme (LPS) adoption. This is expected to release over Rs 2,000 crore and Rs 3,500 crore for top 10 leading renewable developers in FY23 and FY24, respectively. Accrual generation is also expected to increase with higher operational portfolio base of these players.

Operational portfolio of the leading 10 developers in CRISIL Ratings study increased from 18 Gw as on March 2020 to 34 Gw as of September 2022.

These drivers are expected to lead to stable or moderately improving leverage for leading players. Total Debt/ Ebitda of the leading developers should trend below from levels of 8.1 times in fiscal 2021 to 7.9 times in fiscal 2023.

There are downside risks to the credit outlook as well, majorly from lower-than-expected operational performance. Operational performance, measured through generation, for projects has lagged expectations of P75 levels in past 2 years for both wind and solar segments. This has largely been on account of resource related variations and hence is expected to recover in line with its cyclicality.

Recovery in performance to expected standards of generation will be a key monitorable going forward.