Clipped from: https://www.thehindubusinessline.com/opinion/was-rbis-latest-rate-hike-driven-by-external-factors/article66294014.ece

More than controlling inflation, the rate hike was meant to arrest capital outflow and prevent the rupee from depreciating further against the dollar

The RBI raised its ‘repo rate’ under Liquidity Adjustment Facility (LAF) from 5.90 to 6.25 per cent on December 7. It is the 5th consecutive hike in the RBI’s main policy rate.

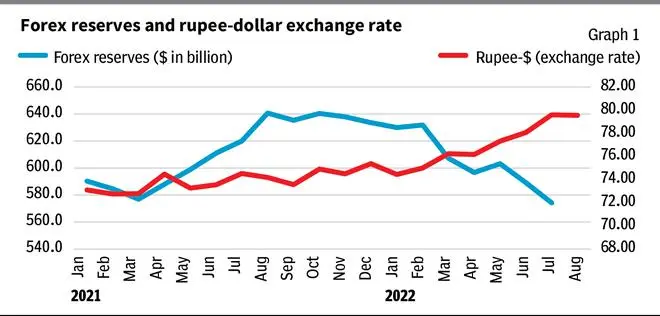

A pertinent question that comes to mind concerns the actual reason for the current rate hike, if we take into account developments in the external sector. Data obtained from the RBI reveal that net foreign investment to India has turned negative of $1.4 billion (net outflow) in the fourth quarter of 2021-22, from $12.6 billion (net inflow) in the second quarter of 2021-22. This is also reflected in the gradual running down of RBI’s forex reserves from $640.7 billion in August 2021 to $574.3 billion in July 2022 (Graph 1).

This is a drop of around $66.5 billion in forex reserves within a year — a 10.3 per cent decline. One possibility could be that the RBI has used its forex kit to keep the Indian currency from depreciating fast in the face of decline in net capital inflows. Notwithstanding the tacit efforts of the RBI, the rupee-dollar exchange rate has depreciated from ₹73.10 to a dollar in January 2021 to ₹79.60/ dollar in July 2022 (Graph 1).

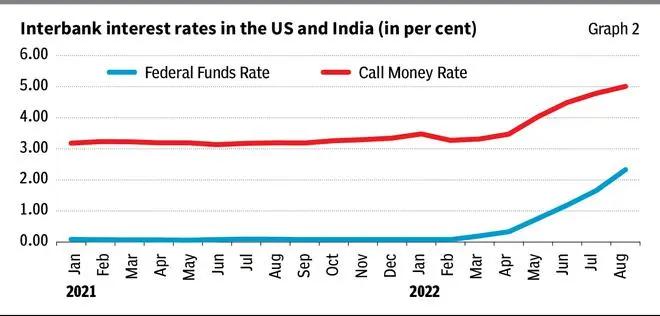

A related issue is the withdrawal of monetary accommodation by the US Fed. It has raised its target for the ‘federal funds rate’ in the recent times. Plotting the ‘call money rate’ in India along with the US ‘federal funds rate’ reveals their close movement in Graph 2.

The possibility of future hike in federal fund rate target by the Fed having implication for the RBI’s current repo rate hike cannot be completed ruled out.

This is because, the rise in federal funds rate makes investment in US securities more attractive than India, thus tempting further capital outflow. This consequently may cause the rupee to depreciate further. In fact, as expected, the Fed had raised its targeted policy rate by 50 basis points on December 15.

Economists talk about ‘impossible trinity’, which implies an economy cannot enjoy monetary policy autonomy under fixed exchange rate regime, while allowing for free cross-border capital flows. The RBI’s stated policy is that it does not target any particular level or band of rupee-dollar exchange rate, so as to retain the monetary policy autonomy.

Perhaps the current situation suits the RBI to suggest that the current policy hike is driven by monetary policy considerations to control inflation. But in reality, the rate hike could be meant to arrest excessive capital outflow and protect the rupee against the dollar.

The writer is Professor, Department of Economics, School of Management, Pondicherry University