SynopsisThe RBI on December 1 launched the pilot of e-rupee, the CBDC aimed to mimic and expand the usage functions of paper currency, in a closed user group. Its expected benefits include faster settlement, lower cost of cross-border transactions, and reduction in currency printing. However, with concerns around privacy and data integrity, a full-fledged implementation could be a challenge.

It was in 2016 that a government panel on digital payments, chaired by former bureaucrat Ratan Watal, first recommended studying the possibility of a central bank-issued and backed digital currency, and testing a proof of concept. However, it was only the popularity of private cryptocurrencies and stablecoins – until their recent crash – that forced the apex bank to speed up the launch of digital currencies.

In October 2021, the central bank proposed an amendment to the Reserve Bank of India Act, 1934, to enhance the scope of the definition of ‘bank note’ to include currency in digital form to the government.

In her Union Budget speech on February 1, 2022, Finance Minister Nirmala Sitharaman proposed to introduce digital rupee, using blockchain and other technologies, to be issued by the RBI starting 2022-23.

“The amendment in the RBI Act with regard to the CBDC (central bank digital currency), says that currency will also include digital currency. That is the amendment which has been brought. Therefore, in all respects, there is no difference in the eyes of law, and there is no difference in treatment between paper currency and digital currency,” said RBI governor Shaktikanta Das on December 7.

What is E-rupee?

From December 1, the RBI has launched a pilot of e-rupee retail in a closed user group with four participating banks — State Bank of India, ICICI Bank, IDFC First Bank and Yes Bank — and several merchants.

E-rupee is the CBDC issued and backed by the RBI that aims to mimic and expand on usage functions of paper currency or physical cash. It will be fundamentally different from the present UPI transactions — sans the direct involvement of banks as transactions will happen through e-wallet. The pilot for retail users follows a similar one launched for wholesale e-rupee transactions in November.

The expected benefits of e-rupee — faster settlement, lower cost of cross-border transactions, reduction in currency printing and distribution costs – are pitted against potential pitfalls including issues of privacy, data integrity, cyberattacks and disruption in deposit functions of the commercial banks.

Currently, it is only a trial restricted to a closed user group of merchants and customers in four cities of New Delhi, Mumbai, Bengaluru, and Bhubaneswar.

Several merchants like petrol pumps and organised retail stores are transacting with select customers that have been provided CBDC wallets in these cities. The scope of the pilot will be expanded gradually to cover more users in different cities.

In the initial days of the trial, users and merchants are doing a few hundreds of transactions every day, which will be increased to a few thousands. In due course, the plan is to launch a system wherein CBDC can also work in offline mode. This would help in expanding its scope and scale across the country. Direct benefit transfers by the government can also be done through e-rupee in future.

How is India placed against peers?

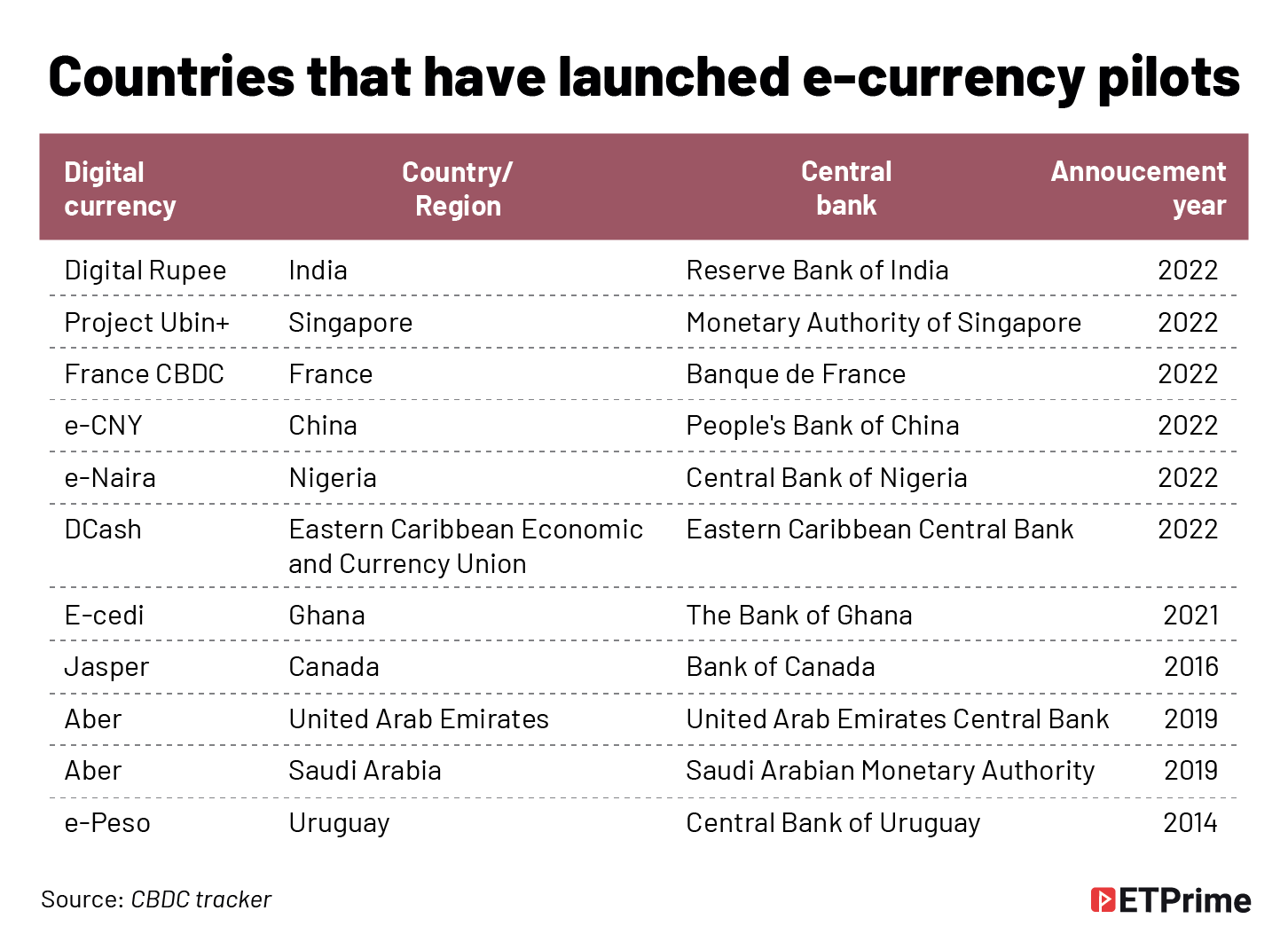

Globally, the eNaira in Nigeria, unveiled in October 2021, and the Bahamian sand dollar, debuted in October 2020, are two fully launched CBDCs. China, Singapore, France, Canada, Saudi Arabia, and the United Arab Emirates are among the countries conducting CBDC pilots. There were more than 100 CBDCs in research or development stages.

In the Indian context, the central idea is that in terms of look and feel, usage and features the e-rupee should exactly mirror the functionality that cash offers. That brings into focus a key issue — can e-rupee offer anonymity at par with the cash? Critics have raised doubts.

But discussions with the government and senior RBI officials indicate that the level of anonymity prevalent for cash transactions has to be integral for a full-scale launch of e-rupee. How to achieve that? The jury’s still out.

How will RBI ensure anonymity?

There are two possible ways. One is the technology route, where the RBI systems deploy auto-deletion tools that erase transaction records up to a certain extent, let’s say INR50,000. Another way could be the government enacting a legislation or providing it through rules that e-rupee transactions up to a limit cannot be stored or probed into. However, the execution manner can be gauged after the experience of the pilot projects, learnings from other countries and technological options being developed.

“One of the reasons cash is still being used in many developed countries to a large extent is that people love privacy, and people love their anonymity. So, for anonymity purposes, currency can be used. How anonymity is to be ensured in the case of a digital currency? The normal understanding is that anything digital leaves a footprint, can have various solutions,” RBI deputy governor T Rabi Sankar said on December 7, 2022.

“We are looking at the largely first technological solution. We understand there are technologies possible to do that. So, we can use any one of those. It is also possible to get a legal provision to ensure anonymity. So, what exactly will happen will depend on how things evolve, but anonymity is a basic feature of currency, and we will have to do that…,” he added.

Currently, for cash transactions above INR50,000 or more, quoting PAN card details is mandatory, while the tax laws do not allow usage of cash for a single transaction above INR2 lakh. While the INR2 lakh limit may not be applicable for e-rupee, transactions up to INR50,000 per user in e-rupee will be kept anonymous.

How will e-rupee be different from UPI, cryptocurrencies?

To understand this difference, let’s first know how e-rupee will work.

E-rupee will be issued in the same denomination as the paper currency. A user with say an account with the ICICI Bank, a participating bank in the pilot, will download the wallet of the same bank and transfer funds into the wallet. Instead of a cash withdrawal, funds have now been loaded onto the wallet as e-rupee. Transactions can be both person to person (P2P) and person to merchant (P2M). So, it will be a wallet-to-wallet transfer between these parties without the bank coming in between. This functionality is also critical to offering anonymity in CBDC transfers.

In UPI transactions, banks act as intermediaries, whereas in e-rupee its direct money transfer from one wallet to another.

“When I use a UPI app, the message goes to my bank, my bank account gets debited, money gets transferred to the recipient, to the receiver’s bank, his account gets credited, and he gets a message in his mobile phone. So, there is an intermediation of the bank in that process. In CBDC, just as paper currency, you go to a bank, let us say, you are drawing some INR1,000 currency notes, you keep it in your purse, you go to a shop, you have to pay INR500, you take out INR500 and pay,” the RBI governor said.

“Here also, you will draw the digital currency and keep it in your wallet, which will be basically your mobile phone. And when you go and make a payment in a shop or to another individual, it will move from your wallet to his wallet. There is no routing or no intermediation of the bank,” he said.

As regards to private cryptocurrencies that are created with decentralisation at their core, the e-rupee will be issued, backed, and controlled by the central bank like any other legal tender. It is a liability of the RBI like other currencies.

What are the key challenges?

The fact that several countries such as Uruguay, Canada, Saudi Arabia and United Arab Emirates have been running CBDC pilots for several years means a full-fledged launch of digital currencies may be easier said than done.

“While a CBDC may have many potential benefits on paper, central banks will first need to determine if there is a compelling case to adopt them, including if there will be sufficient demand. Some have decided there is not, at least for now, and many are still grappling with this question,” Andrew Stanley, staff of finance and development at the IMF, wrote in a note on The Ascent of CBDCs in September 2022.

“Additionally, issuing CBDCs comes with risks that central banks need to consider. Users might withdraw too much money from banks all at once to purchase CBDCs, which could trigger a crisis. Central banks will also need to weigh their capacity to manage risks posed by cyberattacks, while also ensuring data privacy and financial integrity,” he wrote.

Another risk is that it may not be possible to keep digital rupee transactions completely anonymous, as a trail can always be established for each transaction. The wallet-to-wallet transactions could certainly be anonymous. But when a user transfers money into the wallet or withdraws money from the wallet to his/her bank account, these transactions will reflect in the user’s bank statement.

Effect on deposit functions of the commercial banks is another key pitfall, especially if there is wider adoption of CBDCs and consequent withdrawal of funds from the banks into the wallets. This could partially be neutralised by banks offering a sweep-in facility that transfers digital rupees from users’ wallets back into their bank accounts by the end of the day.

What is the global experience on CBDCs?

In an encouraging development, the Bank for International Settlements (BIS) and four central banks recently completed a successful pilot of the use of CBDCs by commercial banks for real-value transactions across borders, as part of Project mBridge. Twenty banks in Hong Kong SAR, Thailand, mainland China and the United Arab Emirates used the mBridge platform to conduct 164 payment and foreign-exchange transactions totalling over USD22 million, the BIS said on October 26, 2022.

Project mBridge is aimed at creating a low-cost, regulatory-compliant, and scalable cross-border payment solution with CBDC at its core. It is being designed to operate across different jurisdictions and currencies, to explore the capabilities of distributed ledger technology and the application of CBDC in cross-border payments between commercial banks. Such a system could help two countries, let’s say India and Russia – both having their own digital currencies – transact seamlessly without going through SWIFT or other financial networks.

(Graphic by Mohammad Arshad)(Originally published on Dec 15, 2022, 04:45 AM IST)

The latest from ET Prime is now on Telegram. To subscribe to our Telegram newsletter click here.