Synopsis

Spreading cash among consumers and collecting notes from businesses is a labor-intensive activity that doesn’t sit well with Japan’s shrinking workforce. In India, fewer notes will lead to pubic savings on $600 million in annual printing costs.

Five years ago, central bank digital currencies were a curiosity. Now, they’re a fad. More than 40 economies are running pilots or are in the pretrial development phase, in addition to the 11 already using them. With rising interest, previously unasked questions about these new-age payment tools are starting to emerge. Some sound deceptively easy, but getting the answers right could be crucial.

Start with one such simple query: physical representation. It was an issue that the Reserve Bank of India raised in October, ahead of a retail e-rupee trial that got under way this month. Simply put, there are two design choices. One is to specify a minimum value — say, 1/100th of a rupee — and allow tokens of any amount that can be composed without breaking the floor.

So if a consumer wants to pay someone 825.05 rupees ($10) by using the central bank digital currency, or CBDC, it will inform its bank, which will debit the person’s savings balance and request the RBI to issue a coin for the exact amount. The token will duly pop up in the user’s wallet after the RBI deducts 825.05 rupees from the requesting bank’s account with it.

None of this should take more than a few seconds. However, some friction is ingrained in public money and we probably don’t want to lose all of it. For instance, physical cash comes in fixed denominations. So it may make sense to require the consumer to request for one e-rupee coin of 1,000 rupees from the RBI. She can then spend a fraction of it and immediately see an unspent balance in her digital wallet. It can be simply left there for later use, or moved back into a regular savings account.

How’s this a better design? A fixed denomination is a wholly artificial construct in the digital world. But to the extent it anchors people into believing that what they’re using is just an online version of familiar sovereign money — safe even if their bank or wallet provider goes bust — it may actually be reassuring for users. (The functionality shoppers gain over bank notes is that they won’t have to go back home with unwanted candy that merchants in India pass on when they don’t have change.)

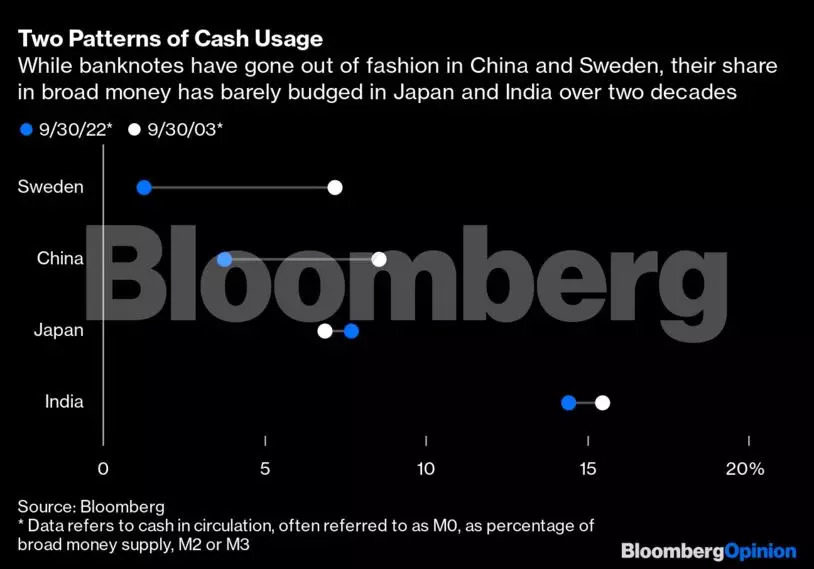

Trivial as they sound, decisions like these will shape our cashless future. Some of the early CBDC experimenters like China, Sweden and South Korea have already moved away from physical cash to a large extent. There, the authorities fear that unless they come up with an alternative, national money will be reduced to being just a unit of account — yuan, krona or won — without any physical presence. That could have unpredictable consequences. If the payment market is cornered by a few powerful private-sector platforms, they may impose hidden charges and fees. It will be hard for people to go on believing that their deposits and wallet balances are actually worth what the account statements say if they have no testable way to obtain a more trustworthy public-sector representation of the same value in exchange. You won’t know if water actually boils at 100 degrees C if all you have is a thermometer; you also need water.

Then there are countries at the other end of the spectrum. Japan will start CBDC trials in spring and spend two years on the results to decide whether to issue a virtual currency in 2026. But the problem with Japan — or India — isn’t that physical cash is going extinct. It’s the opposite: Japan’s cash habit is so deeply rooted that the government wants to nudge wage earners to receive a part of their pay in digital wallets. India, which shocked the world six years ago by canceling 86% of the then-existing cash in the economy, has nonetheless failed to break the affinity for banknotes. Yes, digital payments have surged 250% in four years, according to a central bank index. Yet, paper bills continue to grow.

Spreading cash among consumers and collecting notes from businesses is a labor-intensive activity that doesn’t sit well with Japan’s shrinking workforce. In India, fewer notes will lead to pubic savings on $600 million in annual printing costs. However, neither country suffers from a lack of private-sector digital payment options. Given the plethora of available choices, users are likely to ask a second question of CBDC: “How is this cash if you can see what I’m spending it on?”

Trails in digital payments are a feature, not a bug. One way to address privacy concerns is to place an anti-money-laundering authority in the picture as a kind of class monitor. Someone requesting cash from the central bank will also get a fixed number of “anonymity vouchers” free of charge from the monitor. These won’t circulate among people but will need to be spent to maintain the secrecy of transactions.

This European idea could work in situations where the guarantee from the central bank that it won’t lift the veil of anonymity around small payments carries weight. Where the relationship between citizens and the state has a trust deficit to begin with, technology may offer better solutions than institutions. One such idea comes from the world of polling. The election officer (read, the monetary authority) signs a sealed envelope that carries your secret ballot (the payment details); carbon paper (cryptography) carries the signature to the vote inside. So when the envelope is opened (the payee is credited), all that the receiver’s bank sees is the signature attached to the ballot, not where the vote (the funds) came from. You, however, will know what you did or didn’t intend to do. If a terror financier steals your wallet, you’d go to law enforcement to show them where your tokens are. You might even get them back.

Another question authorities need to consider is speed. It can be a showstopper. Recall that the impetus for CBDCs came from advancements in blockchain technology. But as the Korean pilot program has underscored, an Ethereum-based network may not be the best solution for crowds of office-goers trying to pay for their meal. If this problem remains unaddressed, most daily users would gladly stick to near-instantaneous private-sector digital payment options despite the bankruptcy risk.

After all, nobody wants to be kept waiting at lunchtime.