SynopsisAsset reconstruction companies, jokingly referred to as scrap dealers in the financial market, were set up to free banks from the burden of stressed loans. Grappling with allegations of having cut sweetheart deals in the messy junk-loans market, these bad banks are trying to salvage their reputation amid the glare of regulators and investigative agencies.

Dealing with bad loans can be messy. It involves recovering money from difficult and often nasty borrowers that high street banks have washed their hands off. It can be a long, tortuous road replete with court feuds, hidden losses, and unpleasant surprises.

At the heart of this trade are asset reconstruction companies (ARCs), which trade on bad loans by buying sticky assets from banks to make money out of them. In other words, they are the financial market’s scrap dealers, and swirling around them are whispers of sham deals and arm-twisting.

Operating in this comparatively opaque and murky side of the financial market, ARCs are now battling a different kind of stress: salvaging their reputation.

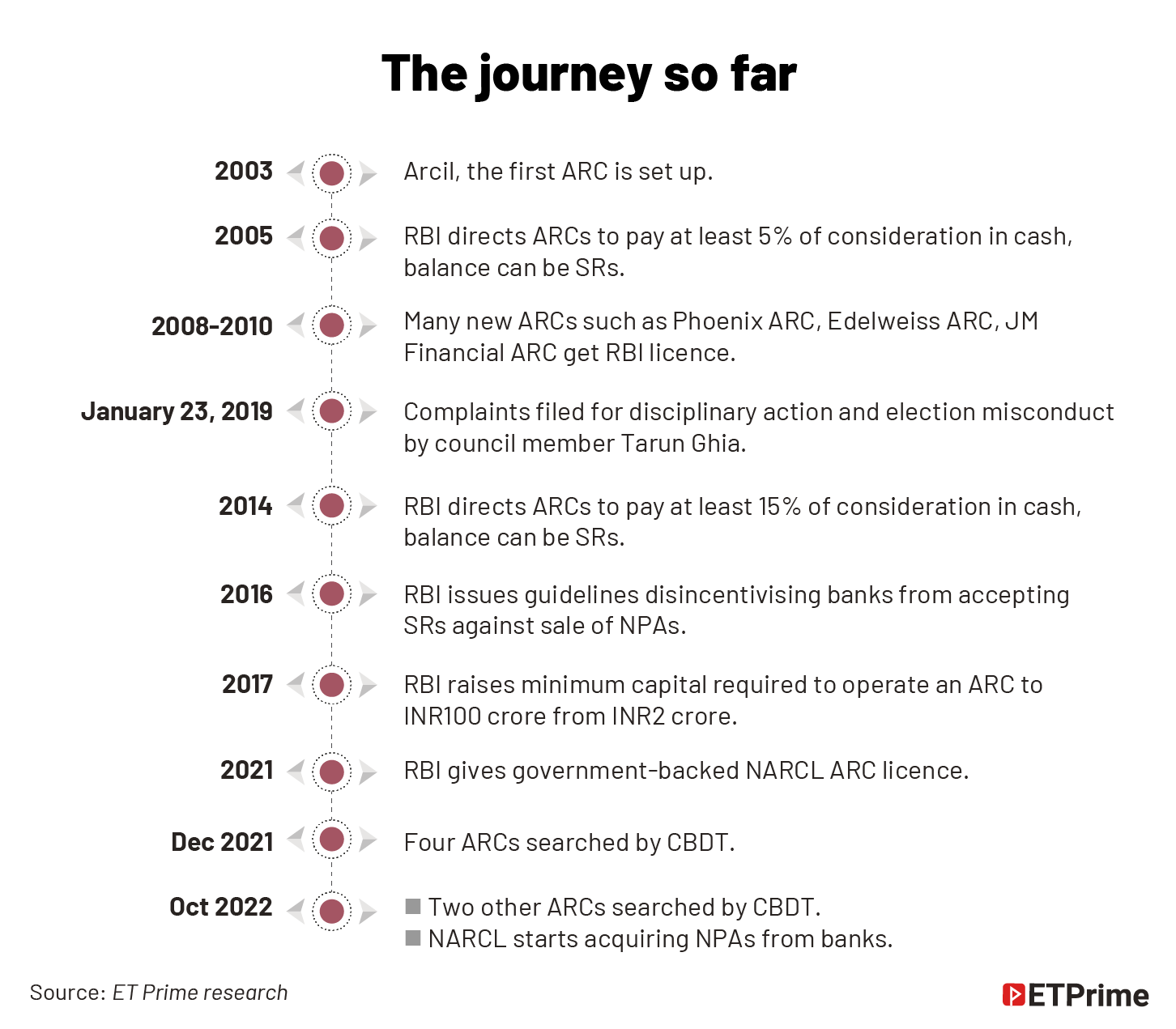

They first came under the shadow in December 2021 when income tax officials searched the offices of four ARCs on suspicion of an “unholy nexus between borrower groups and ARCs” which raises concerns that in the process“a maze of shell/dummy” companies were used.

The media picked up the cues from the Income Tax (IT) Department — known for its sweeping choice of words — but slowly lost interest as stressed loans and ARCs rarely make a readable story. But almost a year later, those allegations resurfaced when the IT department searched two other ARCs.

Soon, many sensed that a pattern was emerging. ARCs, often functioning below the radar, can be the centre of allegedly underhand deals involving loans worth thousands of crores. As banks get rid of these unrecoverable loans (better known as non-performing assets or NPAs) to clean up their books, another story unfolds.

First, let’s take a look at the facts.

In October, UV ARC and Alchemist ARC were searched by the IT department. In December 2021, it searched the premises of Invest ARC, Rare Asset Reconstruction, CFM Asset Reconstruction, and Omkara ARC.

According to the apex body of the IT department, the Central Board of Direct Taxes (CBDT), the ARCs have evaded taxes by concealing profits on the disposal of assets by diverting the actual profits to their related concerns under the garb of consultancy receipts or unsecured loans/investments.

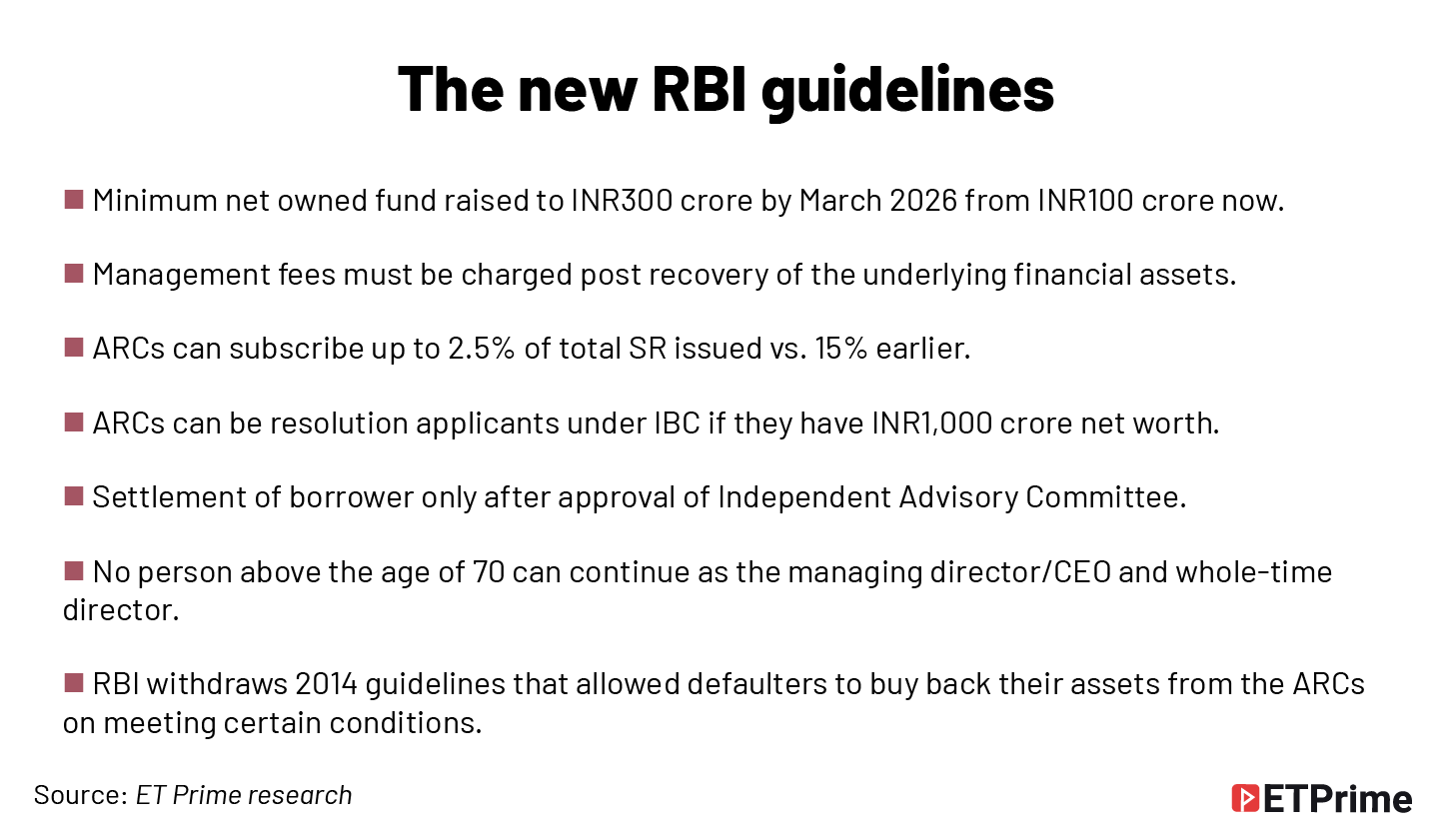

The IT department’s search comes within days of the Reserve Bank of India (RBI) tightening rules for ARCs to ensure that defaulters do not gain from their deals, to weed out the smaller players from the system, and restrict them from charging management fees.

Lenders jokingly refer to ARCs — 29 of them with assets under management (AUM) of about INR1.20 lakh crore — as scrap dealers. They buy loans where the borrowers have defaulted and help banks clean up their books for fresh lending.

So, why are these bad banks that have been around for two decades under the scanner now?

The fault lines lie in the 2016 insolvency regulations aimed at maximising recovery by punishing hard-core defaulters. It has opened an arbitrage opportunity for defaulters to cut sweetheart deals with ARCs which may secretly give the former a say in the corporate resolution process.

In October 2021, the promoter of GarhRajwada Hotel in Jaisalmer filed a police complaint alleging a nexus between State Bank of India (SBI) and Alchemist ARC, which bought the promoters loan at a throwaway price following a default. The complaint led to the arrest of former SBI chairman Pratip Chaudhuri who had joined the board of Alchemist after retirement. It caused an uproar and sparked a debate on the integrity of ARCs.

The turning point

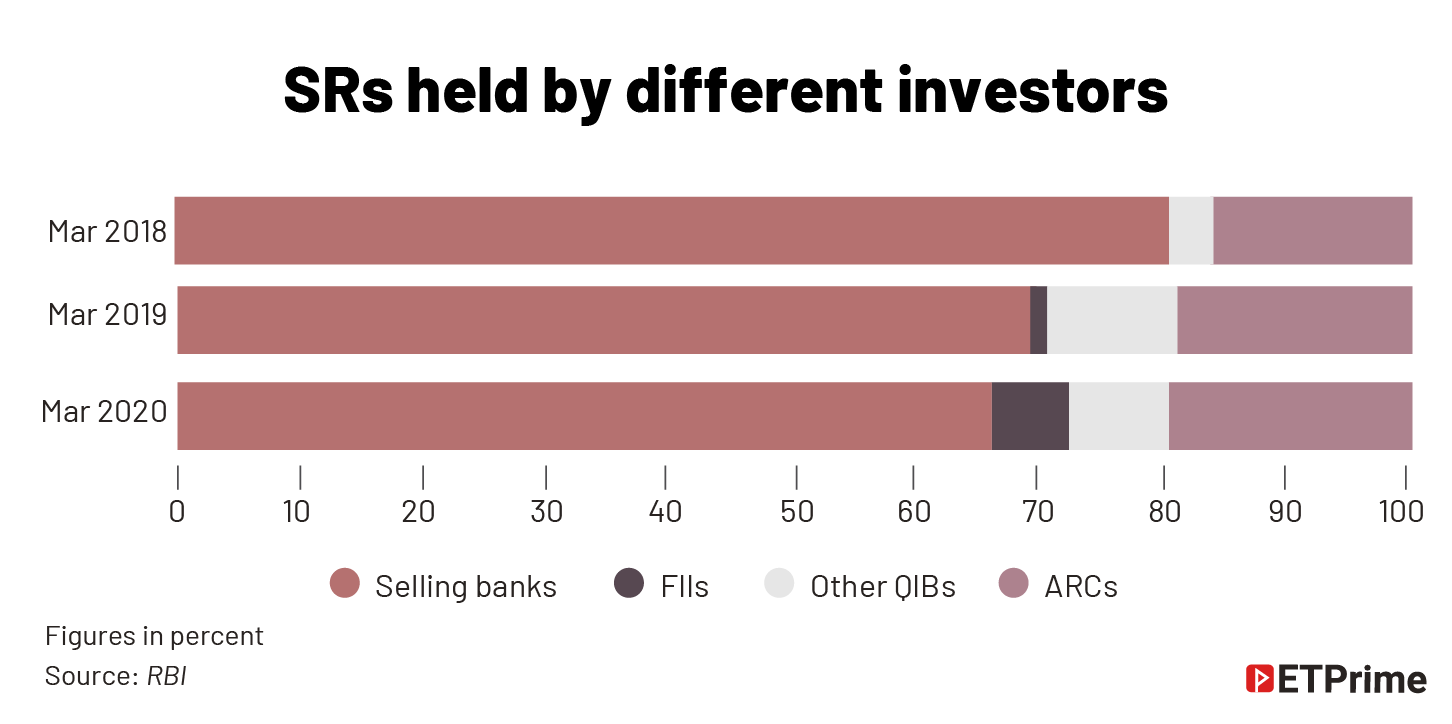

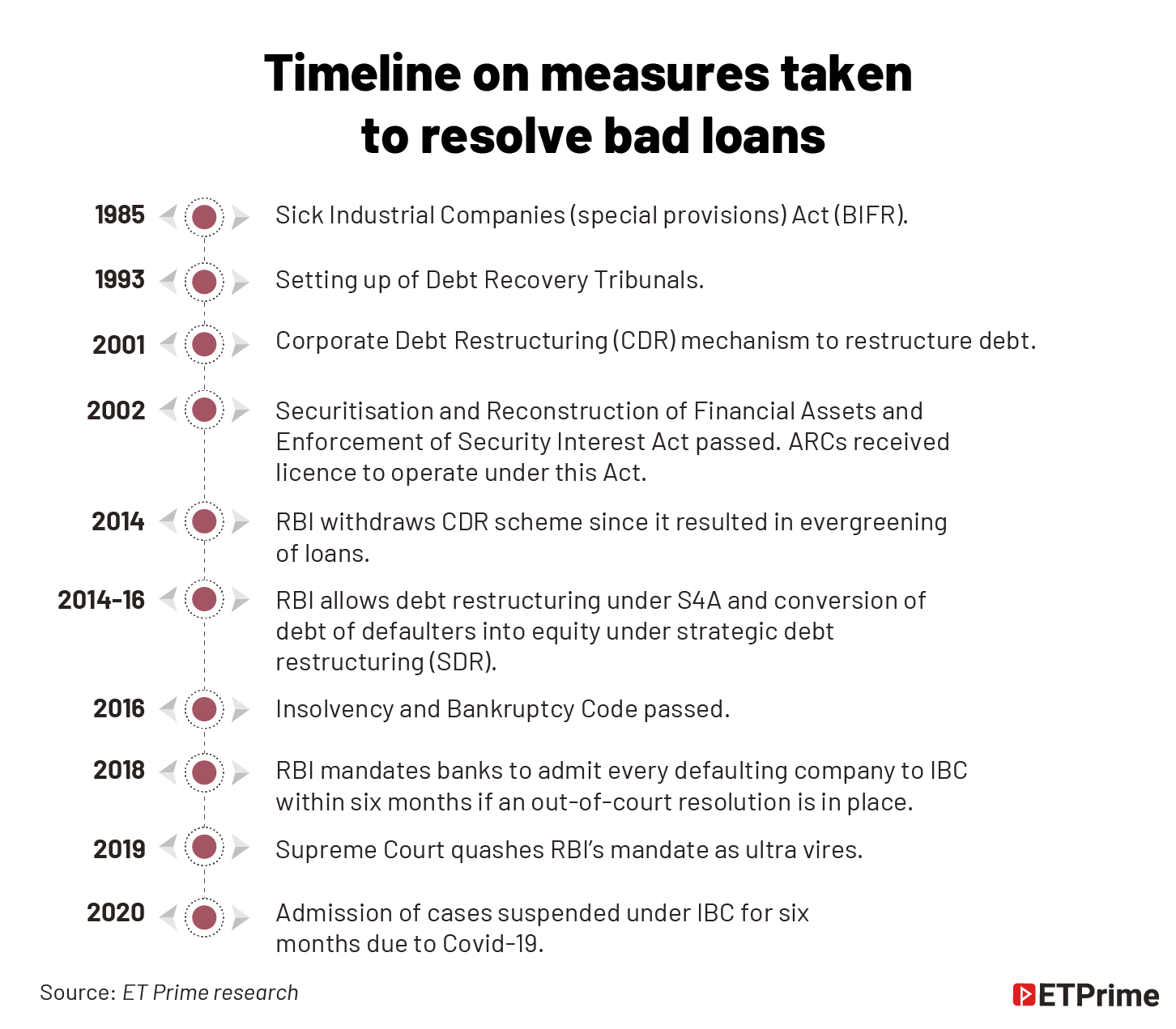

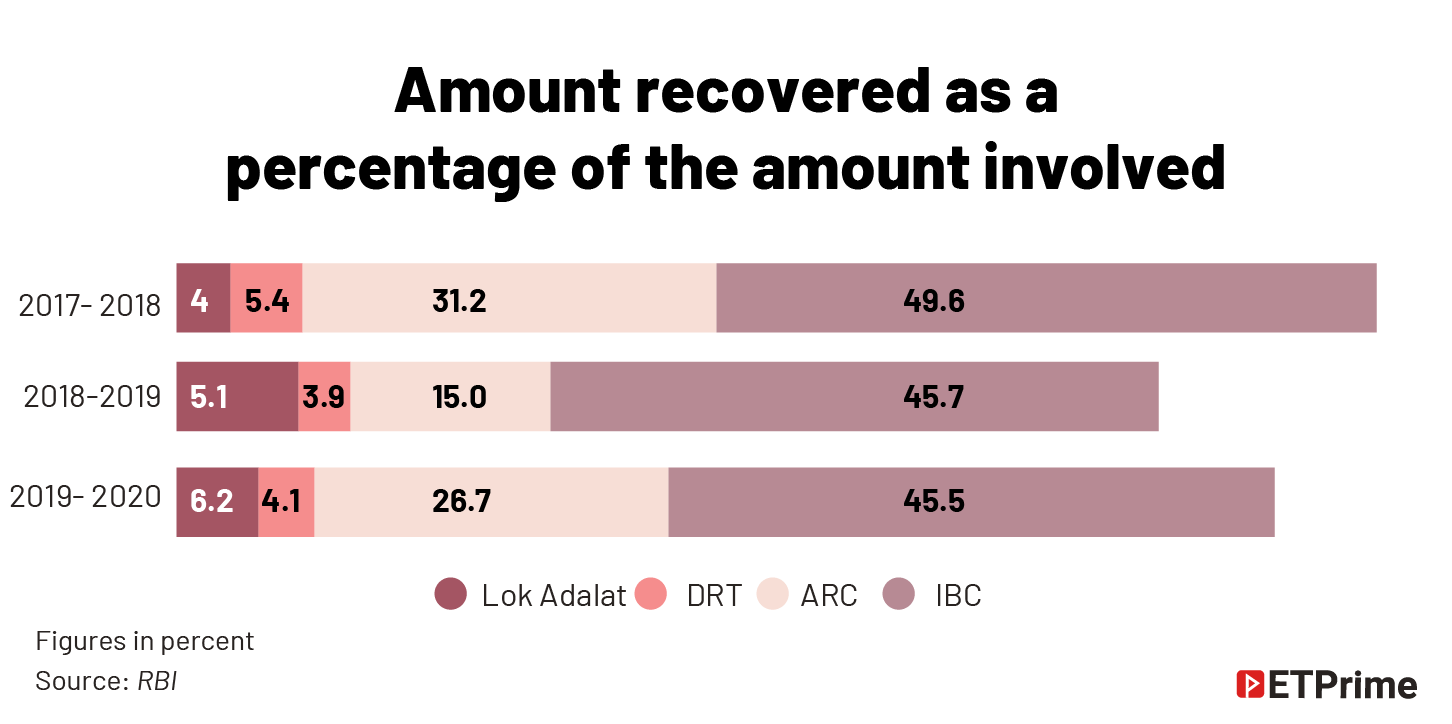

Banks never fully trusted ARCs. The lack of confidence stemmed from the conventional practice of buying bad loans in exchange for security receipts (SRs) for 95% of the loan value. Many of these receipts proved worthless. Over the years, several banks were saddled with it and they could neither sell them nor do anything to recover value from the underlying assets. To add to their woes, the RBI said that banks should write off the SRs if ARCs failed to recover it in eight years.

For instance, SBI, the country’s largest lender with 20% market share in loans and deposits, had to write off over INR10,000 crore of SRs after it failed to find buyers at an auction held in July 2021. The ARCs, however, made money as they charged a fee of 1.5% of the consideration amount each year for managing the bad loans.

In 2014, the RBI changed rules requiring ARCs to pay at least 15% of the consideration in cash. Since most lenders did not want to carry the SR baggage for eight years, they insisted on cash deals wherein the entire consideration is paid upfront.

They preferred cash deals for other reasons, too.

Banks feared that ARCs might sell the company back to the defaulter. This is a problem peculiar to public sector bankers which weigh every action against the possibility of being questioned by investigative agencies in future.

Moreover, a cash deal is akin to a true sale, thus insulating lenders from the allegation that the company was sold back to the defaulting promoter at a throwaway price. But if lenders invest in SRs, they could be linked to the ARC that strikes a deal with the defaulting borrower.

By early 2018, most lenders preferred recovery through the Insolvency and Bankruptcy Code (IBC) route rather than ARC since it promised resolution within 180 days with an outer limit of 270 days.

Also, to be fair to the ARCs, until last month, the RBI allowed buyers of bad loans to enter a settlement with defaulters. Lenders, too, are permitted to enter into a one-time settlement with defaulting borrowers.

Cash deals: an eyewash?

However, cash deals, too, have elements of suspicion, particularly when an ARC without institutional backing acquires big-ticket-stressed loans. For instance:

#Rare ARC’s INR183 crore binding bid for Life insurance Corporation’s debt in KSK Mahanadi Power raised many eyebrows.

#When CFM ARC paid INR825 crore in July 2021 to acquire JBF Industries, there was speculation that Reliance Industries was behind the deal. Reliance denied it.

#Similarly, Adani Ports and SEZ Ltd was rumoured to be backing Omkara ARC’s purchase of loans of Karaikal Port for INR1,500 crore in November 2021. According to media reports, Omkara appointed two Adani loyalists — VettathRaghunandan and Nilanjan Bhattacharya — on the board of Karaikal Port in February 2022. Two months later, it admitted the company for insolvency. Adani is one of the bidders for Karaikal Port, the other being Vedanta.

Neither of the three — Omkara, CFM, or Rare — has any institutional backing to raise this kind of money. CFM’s net worth stood at INR161.5 crore while the tangible net worth of Omkara was at INR210 crore for FY21, according to reports by local rating agency Infometrics Ratings released in January 2022. Rare has a tangible net worth of INR136 crore for FY20, according to the latest available rating report by Brickwork Ratings.

Bankers suspected that some ARCs were front-running for corporations.

A short cut

There is an arbitrage opportunity for ARCs because corporates cannot buy distressed debt from banks. The only way for them to acquire a distressed company was under the IBC or the June 2019 RBI guidelines that permit change of management while restructuring a loan.

To sidestep this, corporates began funding ARCs to acquire the entire debt of distressed companies from lenders. As a sole creditor, the ARC is in a position to control the resolution process making it easier for the corporate to acquire the company in IBC.

It worked well for ARCs, too. Banks and finance companies do not lend to bad banks, making it difficult for them to make cash offers.

This model of resolution gained traction. Banks realised this was the quickest way to recover their money rather than waiting over a year for bankruptcy courts to approve a plan.

The first such deal was struck in December 2018 when The Chatterjee Group (TCG) acquired Garden Silk Mills. Here, Invent ARC, financially supported by TCG, acquired INR1,680 crore in debt from lenders at a 60% discount in an all-cash deal. Later, the ARC sold the textile company to TCG under the IBC in six months. These days, it takes six months or more to get a company admitted under IBC.

Subsequently, JSW Steel acquired BMM Ispat, outside the IBC framework, wherein Edelweiss ARC and Indostar acquired bank loans and sold the company to JSW Steel. Jindal Saw is set to acquire SathavahanaIspat using the JC Flowers ARC platform, while JSW Steel will soon buy National Steel and Agro via JM Financial ARC. Industry experts say the cash-rich corporates acquired distressed companies using the ARC route mainly to save time.

The thumb rule is that if an ARC offers to buy the entire debt of lenders, invariably, the bad bank’s offer will be backed by a strategic partner who is funding the deal.

The banking regulator has good reasons for restricting corporations from directly acquiring debt from banks. Purchasing stressed loans can give corporates a bigger say in the insolvency process as they indirectly become creditors, thus paving the way for selling the company back to the promoter at a throwaway price. A court-endorsed revival plan against cutting a deal with a corporate (who buys the debt) also lends a degree of immunity to banks. Since the RBI cannot regulate corporates, acquiring debt is restricted to banks, finance companies, and ARCs.

There are also instances where ARCs have taken the entire debt and successfully restructured it without pushing out the promoters but with the support of financial investors. While the RBI directed lenders to refer Jayaswal Neco to the National Company Law Tribunal (NCLT), all banks (in separate transactions) sold their debt to Assets Care and Reconstruction Enterprise (ACRE), which restructured the loans while ringfencing its cash flows. ACRE’s offer to lenders was backed by a financial investor — Bank of America.

Similarly, in the case of NSSL Ltd, an unlisted subsidiary of Jayaswal Neco, Avenue Capital-backed Asset Reconstruction Company of India (ARCIL) acquired its entire loans from lenders and subsequently restructured them.

The unholy nexus

There may be many such cases that may have escaped media attention. And that brings us back to the question raised by the IT department about the unholy nexus.

Industry experts suspect that many defaulters who siphoned off money from the company by issuing inflated or fake invoices are buying back their companies using ARCs as a conduit.

The CBDT, too, has similar suspicions. It alleged that the ARCs follow non-transparent methods in disposing of assets acquired from the banks. Often, these assets had been re-acquired by the same borrower group at a fraction of their real value, it said in a statement on December 15, 2021.

It is quite likely that dubious promoters are funding smaller ARCs to acquire 66% of debt at a deep discount. ARCs, as the sole creditor, can control the resolution process and may sell the company to persons linked to the promoters.

Similarly, promoters may fund ARCs to acquire up to 90% debt of a company amid corporate insolvency. Once an ARC holds 90% debt, it can pass the resolution to withdraw the company from the IBC under Section 12A. Here, the promoter regains control while lenders take a steep haircut.

What makes a defaulter comfortable striking a deal with an ARC but not a bank?

Lenders have stayed away from such deals due to the perpetual fear of investigative agencies. But ARCs have had no such worries until recently.

On the one hand, the government wants to send out a message that corrupt, unscrupulous promoters would be punished. Rules such as Section 29A of the IBC are designed to prevent defaulting promoters from gaining control over their companies. Regulators have also made it clear that defaulters will not have a “divine right” (as former RBI governor Raghuram Rajan famously said in 2016) to control companies that were ill-managed under their leadership.

But at the same time, the IBC framework has a provision under Section 12A for promoters to settle loans which encouraged promoters such as Gautam Thapar of Crompton Greaves, Kapil Wadhawan of DHFL and Anil Ambani of ADAG (Anil Dhirubhai Ambani Group) to give settlement offers. Lenders explain such offers only delay the process.

Meanwhile, the RBI guidelines also need to give a clear direction. It says that while resolving a loan, ARCs should be mindful of Section 29A of the IBC, but it permits settlement with the promoter when all other options are exhausted.

But there is one aspect on which the RBI and IBC are very clear — a complete restriction on the settlement with promoters classified as fraud and wilful defaulters. This should be the guiding principle for settlement rather than having multiple and conflicting rules around it.

The bottom line

The IT department’s challenge would be to establish the links among the connected parties that are often lost in the maze of companies floated by defaulters. For now, everyone can see the smoke but no one can spot the fire.

Forensic audits and tracking money trails to eventually lift the veils and nab the real perpetrators is a job which is still in its infancy in India.

Thus, many cases often reach a dead end. And the price is paid by taxpayers and shareholders.

(Graphics by Sadhana Saxena)

The latest from ET Prime is now on Telegram. To subscribe to our Telegram newsletter click here.