SynopsisFrom Delhi-NCR to Mumbai to Bengaluru, cases of profile funding, where builders make use of people’s good credit profiles to get cheaper loans, with a promise to pay EMIs on their behalf, are popping up in large numbers. The ‘buyers’ here are left with little options after builders stop paying EMIs. Are we staring at another real-estate scam?

A penthouse and a flat in Mascot Manorath, another one in Himalaya Pride residential projects in Greater Noida, a three-bedroom spacious flat in Parkwood Glade, Mohali and then one more in Dwaarika Heights in Meerut.

This is the list of investments made by 35-year-old Manish Pandey from Delhi, all bought within a span of just three months between October to December, 2015, for a total consideration of approximately INR2.5 crore.

Looking at his investments, Pandey’s profile may seem to be of an entrepreneur running a flourishing business or a C-level executive earning at least a seven-figure salary a month. Right?

Alas, that is not how things are with Pandey.

Pandey is a mid-level IT professional, making around INR1.5 lakh a month. He neither has the financial capability to pay for the investments upfront or even to afford the bank EMIs for such massive investments.

More surprisingly, he bought these properties without spending a rupee out of his pocket, not even for the down payment.

Yet, he managed to get it financed by the banks.

As strange as it may seem, there are many like Pandey who own multiple properties without sufficient financial backing. Such a phenomenon is not restricted to any one residential project or a builder or a particular city.

That’s the story behind the real estate scam known as profile funding, a scam that targets the vulnerable lower middle-class people, who can barely afford to buy any property on their own but have a desire to make a quick buck.

Pandey, too, feels that he fell for that trap.

His property purchases were not genuine investments, but he was being used just as a dummy buyer by the builders. He just used his credit profile in order to get cheaper loans for the builders in lieu of a commission, that too without spending a penny.

The builder paid the down payment, promised to pay the subsequent EMIs on his behalf, buy back the property and close the loan once the flat is ready for possession.

Cut to 2022, four out of Pandey’s five loans have been declared as non-performing assets or NPAs by the bankers and he is fighting legal cases against him for loan defaults.

ET Prime has spoken to many other profile buyers like Pandey, who were offered the same pitch by the builders, and are now facing legal cases against them for non-payment of their dues to the banks.

The arrangement was going smoothly as the market was booming and the builders were paying the EMIs as promised.

But as soon as it stopped, the whole house of cards came tumbling down.

The pitch and the trap

A typical profile funding case starts like this: builders, through a set of brokers, start targeting people belonging to the middle-class mostly in the age profile of 30-40 years.

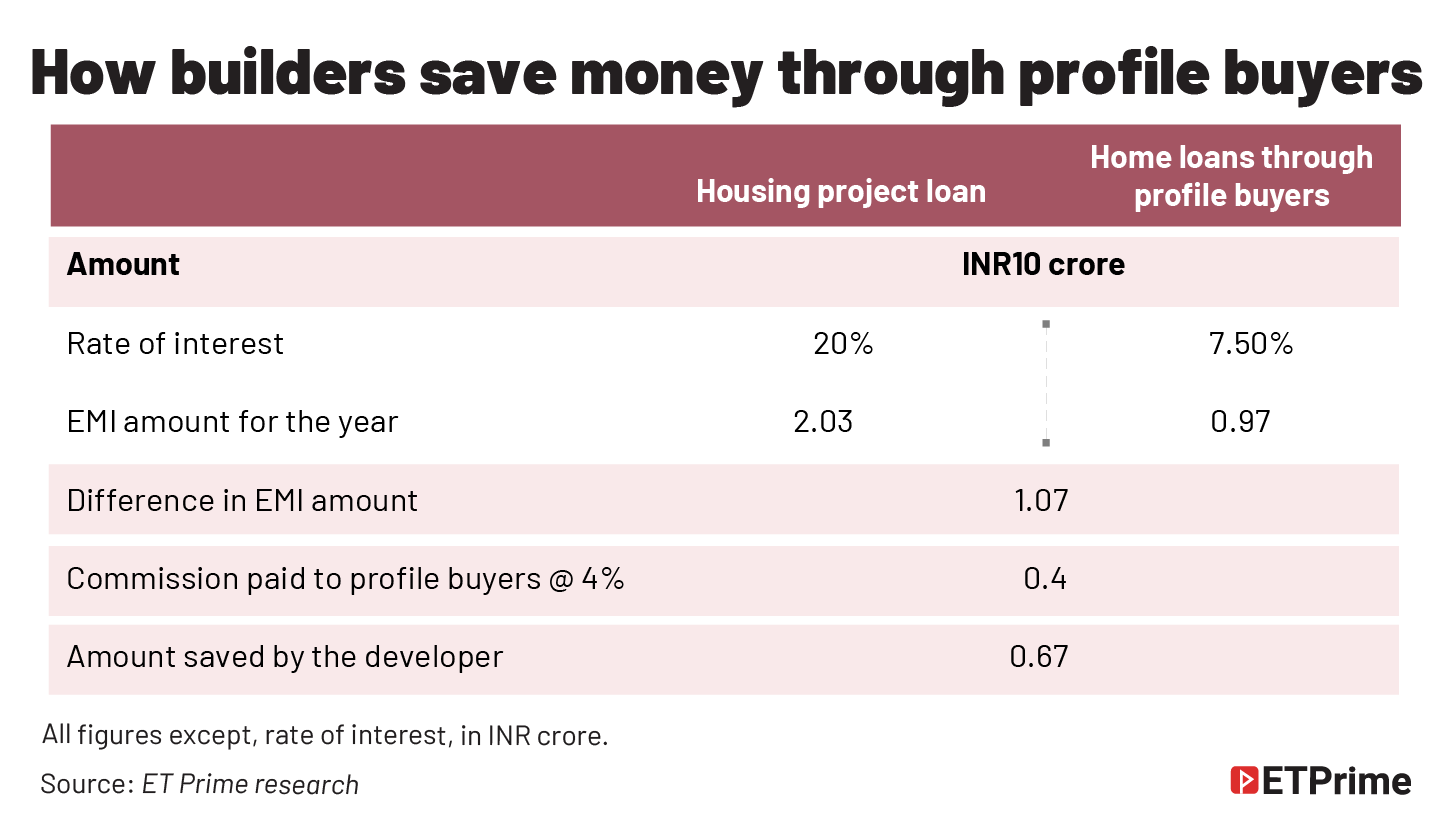

The pitch is simple, the builder says that a project loan has a higher interest rate, say 15%-20% and a home loan is available at 7%-10%. The buyer is then convinced by the brokers to use his loan eligibility or credit profile to fund the builder.

Once the home loan is sanctioned, the builder will get money for his unsold property at a lower rate of interest and can use this money to complete the project.

Once the flat is ready, the builder will find a genuine buyer for the flat, and will close the loan of the profile buyer. In return, the profile buyer gets a commission, ranging between 4%-6% of the loan amount in lieu of blocking his profile and benefits enjoyed by the builder due to the interest rate differential.

As you can see, the pitch is good enough to convince vulnerable people like Pandey who fall prey to such schemes.

But it is not as easy as it may seem.

Firstly, all these agreements between the builder and the profile buyers are simply verbal agreements.

Secondly, the down payment, which is the mandatory requirement to get a loan sanctioned by any financial institution, is not coming out of the pocket of the buyer. The builder is either paying the buyer in cash or through bank transfer routed through dummy accounts. This is a clear violation of banking rules and can attract money laundering charges.

And most importantly, if the builder stops paying those EMIs, the banks will be after the profile buyer to recover their dues as the loan has been sanctioned on his name and not the builder’s, that’s where things become ugly.

Peculiar cases

A Noida-based profile buyer shared a very strange case.

He currently has four profile-funding loans running on his name. All of them have been declared as NPAs. One of such projects, Himalaya Pride in Greater Noida, was in advanced stages of construction. He then decided that he will continue that particular loan as a genuine buyer and sell it off to clear his dues.

“The above incidents demonstrate the sorry state of affairs in the real estate industry. Where builders and bankers are working in collusion. The Delhi High Court in various batches of writ petitions have noted that protection needs to be given to the homebuyers who are stuck in such schemes.”

— Anshul Gupta, managing partner, ANG PartnersHe decided to go and check the status of his flat and was shocked to see that the flat is complete and somebody is already residing in the flat, while the bankers are chasing him for loan recovery.

The builder not only got funds through the bank loan in his name, but he further sold the property to another buyer at a higher rate.

Another case, incidentally in the same project, is of a ghost flat. A profile buyer has a loan running on his name for a particular flat number but in reality the flat number doesn’t even exist.

For instance, there are four flats on a floor, say, 101, 102, 103, 104 and there are 15 floors in a tower, the fourth flat on a floor, namely, 104, 204 and so on can be found until the seventh floor. But after the seventh floor the builder clubbed two flats into one and changed the flat number. Hence, flats 804, 904 and so on, are clubbed with 803 and 903 respectively.

The Himalaya Pride project is being developed by Himalaya Group under the flagship company named, Himalaya Residency Private Limited.

Queries sent by ET Prime to the directors of the company on the e-mails provided by them to the registrar of companies remained unanswered till the time of publishing.

In both the cases, loans were given by Canara Bank. E-mail queries sent to the bank didn’t elicit any response.

The scam’s tentacles

The scam started as a nexus between builders, property brokers and some of the bank officials. It was at its peak between the years 2013 and 2016, when the real estate market was booming.

One way of pitching the scheme was through the property brokers. They used to pitch it to middle-class individuals who used to come to them enquiring about available properties but then they could not proceed due to lack of funds for making the down payment and afford expensive EMIs.

“Me and my wife had just thought about buying ourselves a home. We just started visiting brokers to get a feel of the market, to check the properties available and see if we can afford it or not. And in that chase we ended up visiting a property broker in Sector 62, Noida. He showed us a few property brochures but none of them were fitting our budget so we dropped our plan for a while. The broker then pitched us this plan,” a Noida-based profile buyer tells ET Prime on the condition of anonymity.

“We were amazed to know that we can earn a few lakhs without even putting in any capital from our side. He told us that after this, you will have sufficient money to make the downpayment for a new flat of your own. Without much hesitation I agreed to it. The flat was costing around INR65 lakh and with my salary I was not eligible for a loan of that high amount but the brokers assured that it will be managed and he did. Within a week or two my papers were signed and the loan was sanctioned,” he adds.

The builder paid them some amount in cash and some of it came through a bank transfer from the broker. This amount was then sent back to the builder and shown as the downpayment for the flat.

As and when the loan got sanctioned, the builder started paying the EMIs on his behalf as committed. The profile buyer also received INR1.5 lakh as a commission and was promised the balance INR1.5 lakh after the flat was complete and was sold to a genuine buyer.

But after a year, the EMIs stopped coming from the builder and his account became an NPA. He started getting harassment calls from the bank’s recovery team almost everyday, and builders stopped taking his calls too. He is currently fighting a case in the Debts Recovery Tribunal (DRT) for his loan default.

In separate cases, a Bangalore resident was looking for a personal loan of INR2 lakh for his son’s school admission but was lured into this scheme by the executive of a private bank.

One Yudhvir Singh from Ghaziabad was lured into this by his friend who also happens to be director of a real-estate company.

That’s how the scam started to gain scale and started spreading further through word-of-mouth.

The thought of making easy money and making ends meet lured Pandey as well.

“I was facing some job uncertainty at my workplace and was worried about my financial stability. I knew a few people who had been part of such schemes and in many cases, the loans were successfully closed by the builders. It seemed a safe and lucrative option to me and I too, got into it,” Pandey tells ET Prime.

Same was the case with most of the other profile buyers ET Prime spoke with. They were either lured into this scam by office colleagues, friends or relatives.

Some lucky ones

It’s not that every profile buyer got stuck in the scam.

There are a few lucky ones who got into this scheme of arrangement initially and made a quick buck.

“The builders succumbed to the credit crunch and low demand in the market post-demonetisation and defaulted. Had they been using the money appropriately, the current situation would never have occurred. But the builders diverted the money to buy more land or for other purposes and as a result the projects are nowhere near completion and neither us nor the banks can recover anything out of it,” Pandey adds.

Mayank Gupta, founding partner, MNG Law office, a Delhi-based law firm, has represented many such profile buyers in court. He feels that the scale of this scam is huge and it is not restricted to Delhi-NCR but one can find such cases in Mumbai, and Bengaluru among others.

According to him, Chandigarh is developing as a new hub for such scams.

“On an average, each profile buyer has at least two to three properties on his name. We haven’t come across any case with a single property,” Gupta adds.

The profile buyers are the victim of harassment from the banks for recovering their dues, even though they are not the only ones at fault. The builders and the bank officials are equally responsible for executing such a scam. But these buyers are no saints either.

These buyers struck such deals with multiple builders for multiple properties.

“The builders intentionally got into it and they are the ones who have got bankers’ money. The bank officials either were involved in it or didn’t do their proper due diligence to catch hold of such buyers. But in the end we are the ones who are being harassed and fighting legal cases. Why are we suffering alone,” asks Pandey.

Once the builder stops paying EMIs the profile buyers start getting calls from bank officials and the harassment level in these calls increases as the time passes. Ultimately, banks are left with no other option but to take legal action against these buyers.

Mostly the legal cases are being filed at the DRTs, the adjudicating authority for the recovery of debts due to banks and financial institutions.

Another recourse that these banks take is presenting the security cheques of these profile buyers. The bankers present these cheques by filing the entire outstanding loan amount or an amount equivalent to a few months’ EMIs. As these buyers do not have the financial capability to get those cheques cleared, they bounce.

The banks then file cases in civil courts for dishonouring the cheques.

No way out?

Anshul Gupta, managing partner at ANG Partners, a Delhi-based law firm says, “The above incidents demonstrate the sorry state of affairs in the real estate industry. Where builders and bankers are working in collusion. The Delhi High Court in various batches of writ petitions have noted that protection needs to be given to the homebuyers who are stuck in such schemes.”

He adds, “Even the Supreme Court has made a comment in the Bikram Chatterjee vs Union of India case, that it is shocking and surprising that such large stage cheating has taken place, the bankers have failed to ensure and oversee that the money invested in the projects have been diverted elsewhere. The builders have created assets with that money worth thousands of crores.”

Gupta from MNG Law Offices says that these buyers have mainly two legal options, either go to RERA or the consumer court. Which legal option to follow depends on case to case basis. In some cases where there is a clear case of cheating on the builder’s side then a consumer court suits better.

“We have had successes in the past with such cases where such buyers managed to get a favourable judgement from the court,” he adds.

However, a Noida-based profile buyer quoted above feels that the legal route is not that easy. “I have a favourable order from RERA in one of my cases but it is not yet executed. Moreover, I am fighting multiple court cases for one property. The same bank has filed a case in DRT and one in a civil court for dishonouring a cheque. Not only is it an added expense but one has to take a lot of pain in attending those hearings and pursuing them,” he adds.

While Pandey believes that these buyers are the ones being harassed by the banks and they get into legal trouble, the builders who have actually taken the bank’s monies walk free.

Not only have they taken the funds but also not delivered the projects.

“There is either lack of proper due-diligence from the banker’s side while passing these loan cases or they are part of the nexus. The banks also need to take some onus on themselves and also a proper internal investigation is required by the banks into such cases,” Pandey adds.

He also highlighted that in the case of Dwaarika Heights, where he owns a flat as a profile buyer, there was a housing project loan running on the project by IDBI Bank. For every housing loan, the financing bank was supposed to take an NOC from the IDBI Bank. And the disbursed amount should have gone to their escrow account. But the builder and the banks disbursing housing loans for that project didn’t do that.

The project is being developed by EMM VEE Infrastructure Private Limited. E-mail queries sent to the builder remained unanswered.

The scale of this scam is huge: the projects are stuck and buyers have either become insolvent or gone underground — the buyers are not genuine and incapable of servicing their loans. Banks have no way to recover the loans either from the buyer or by selling the property.

(Graphic by Manali Ghosh)

The latest from ET Prime is now on Telegram. To subscribe to our Telegram newsletter click here.