lipped from: https://www.thehindubusinessline.com/opinion/rbis-low-dividend-payout-raises-concerns/article65655432.ece

It shows up poor risk management of forex reserves, such as relying on dollar sales in domestic forex market to book profit

The RBI’s dividend pay-out to the Centre for 2021-22 at ₹30,307 crore was less than a third of what was paid a year ago — ₹99,122 crore. This was at odds with a decent 20 per cent rise in its aggregate income in 2021-22 at ₹1,60,112 crore.

The central bank’s aggregate expenditure before provisions, which exhibits significant year-to-year volatility, rose 12.6 per cent during this period. So, what was amiss this time, given the government’s ever-increasing expectation and demand for higher surplus transfers from the RBI?

The answer lies in more than a five-fold increase in the provision made at ₹1,14,667 crore in 2021-22 to augment the contingency fund (CF), which received a hit of ₹94,250 crore on account of mark-to-market loss on revaluation of foreign securities held by the RBI.

In fact, the total mark-to-market loss in 2021-22 was even higher at ₹1,03,104 crore, representing 64.4 per cent of the aggregate income. If the similar loss made in 2020-21 is included, one gets a total of ₹1,48,134 crore or 50.15 per cent of the combined income for the last two years. The mark-to-market losses, expressed as a ratio of the respective incomes from deployment of forex reserves, are significantly higher.

Risk management

The very large mark-to-market losses, as above, surely portray an unedifying picture of the standard and professional quality of interest rate risk management of foreign currency assets (FCA) of the RBI. By all indications, the interest rate risk exposure of FCA has been modestly on the rise during the period prior to the outbreak of the Covid-19 pandemic in March 2020.

The sharp fall in interest rates in major markets shortly thereafter resulted in a significant mark-to-market gain of ₹53,884 crore for the securities segment of FCA as on end-June 2020.

In fact, the changes in mark-to-market valuation of the securities segment during the last three years, as revealed in the annual reports of the RBI, are mirrored, to a fair extent, by changes in the 10-year US Treasury yield at that time: it fell from a high of 1.92 per cent on December 31, 2019 to a low 0.64 per cent on June 30, 2020, but rose subsequently to 1.74 per cent on March 31, 2021 and further to 2.32 per cent a year later, on March 31, 2022.

However, both in 2020-21 and 2021-22, there was apparently no significant reduction in the interest rate risk of the securities segment either by way of selling securities in adequate quantities or through the use of derivatives like interest rate futures and interest rate swaps in the markets where the RBI invests.

Oddly, the realised profit on sale of foreign securities in 2020-21 was only ₹11,349 crore compared to a fall in mark-to-market valuation gain of ₹45,030 crore during this period. From end-2020, it had become increasingly clear that continuance of extra-loose monetary and fiscal policies for an extended period would eventually lead to higher inflation and higher interest rate in major markets, and, hence, there was a need to reduce risk in a gradual fashion.

World over, central banks with large FCA, like the RBI as also other types of major institutional investors flexibly manage their interest rate risk through the use of derivatives. But, quite obviously, the RBI does not yet make active use of these instruments for risk management.

In other words, the significant growth in the size of the forex reserves of the RBI over the last decade or so has not been matched by a corresponding enhancement in policy sophistication, systems and processes and in the overall professional standard for portfolio management and risk management. It is likely that the current HR policies and practices of the RBI do not support the transformation that is needed for this purpose.

Mark-to-market losses

In the face of the hefty mark-to-market losses, some quarters within and outside the RBI may be tempted to think that these are transitory phenomena arising out of market gyrations and, hence, are of no real long-term significance.

They would be wrong, not in the least because the mark-to-market losses also signify huge opportunity costs of not reducing risk exposure in time. Portfolio performances over any defined period do not conform to the law of averages. They are a direct consequence of the quality and efficacy of risk management.

The significant mark-to-market losses on the securities segment of FCA, seen against the need to transfer as large as possible surplus to the government would raise an important issue: Did the RBI follow any particular strategy with regard to its domestic forex market operations to cushion this loss?

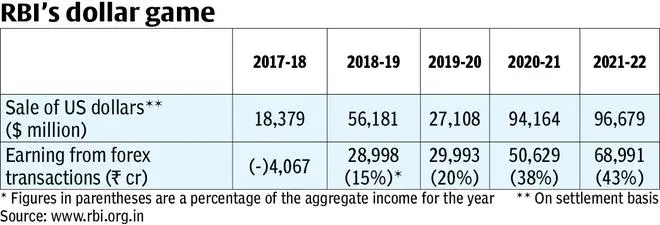

This question is relevant. Since the adoption of a new accounting rule in this regard in 2018-19, rapidly rising profits from forex transactions (which essentially means profit on sale of US dollars in the domestic forex market), on the back of higher US dollar sales volume, have emerged as a vital source of income for the RBI, both in absolute and relative terms.

To be sure, the amount US dollar sales recorded in any period is the outcome of current interventions in the forex market for settlement in that period itself plus maturity of outstanding forward sales, if any. The quantum of interventions in the spot and forward segments of the forex market on any given day depends on a host of complex factors.

Forex intervention

That said, in those two years there was a good bit of ambiguity, certainly not of the constructive variety, in the RBI’s communications, causing some confusion among market participants as regards the exact goals being pursued by the RBI through its forex interventions.

This was especially true of its interventions in the forward market by way of swaps, the volumes of which saw a quantum spurt in 2020-21 and 2021-22, leading to the US dollar-rupee forward premium getting significantly misaligned vis-à-vis interest rate differential and also causing uncertainties and distortions in the forward market.

There has been a legitimate point of view that the large-scale sell-buy swaps that were done during the last quarters of both 2020-21 and 2021-22, pushing up the forward US dollar purchase position of the RBI might have had an additional objective: to book profit on their first leg. This is not without substance, especially for 2020-21, the last quarter sales which were as high as 70 per cent of that of the entire year.

Financial institution, too

The RBI, like any other central bank, is also a financial institution which needs to have a strong capital base and the ability to generate reasonable surplus largely reflecting its seigniorage earning less operating cost. High dependence on profit from the sale of US dollars in the domestic forex market, which seems to be the case now, is not a good trend. This is so because the extent of this profit is determined by how much the Rupee falls against US dollar.

The current exchange rate regime for the Rupee is one involving a managed float and the RBI intervenes in all segments of the forex market using discretion. Hence, the RBI needs to eschew any major reliance on profit from the sale of US dollars, occasioned by depreciation of the Rupee, and none at all for paying decent dividends to the government.

By doing this, it will also avoid the kind of conflicting signals that excessive sell-buy swaps had provided: as alluded to before, such transactions in 2020-21 and thereafter led to a rise in the forward premia, signifying an increase in the implied Rupee interest rate. This was at odds with the extra loose stance of the monetary policy at that time. All in all, it would be much better to bolster the RBI’s portfolio management and risk management capabilities.

The writer is a former central banker and a consultant to the IMF. (Through The Billion Press)

Published on July 18, 2022

COMMENTS