Clipped from: https://taxguru.in/chartered-accountant/hc-grant-bail-ca-case-alleged-negligence-stock-audit-fraud.html

Sunil Bhatia Vs Serious Fraud Investigation Office (Delhi High Court)

Since the ex-promoters/directors and similarly situated chartered accountants have been granted bail, there is no reason why the Applicant should be treated any differently.

Facts-

M/s Bhushan Steel Limited (BSL) is a company under investigation on account of allegations of siphoning off by its promoters.

The allegation against the applicant is that he being a Chartered Accountant and one of the partners at ASRN & Associates [the firm appointed as stock auditors by the consortium of banks led by Punjab National Bank (PNB) for FY 2015-16 failed to perform his duty independently and diligently by not verifying the stock in transit, and he is accused to be in collusion with the office bearers of M/s Bhushan Steel Limited.

It is stated that he is involved in providing and using wrong information to calculate the Drawing Power figures wrongly based on the figures given by M/s Bhushan Steel Limited.

A complaint dated 01.07.2019 was filed under Section 439(2) read with Section 436(1)(a),(d) and (2) read with Section 212(15) of the Companies Act, 2013 read with Section 621(1) of the Companies Act, 2013, read with Section 193 of the Code of Criminal Procedure, 1973 by the respondent, Serious Fraud Investigation Office (SFIO). The respondent also relies upon Investigation Report dated 27.06.2019 filed with the Ministry of Corporate Affairs.

Based on the conclusions in the Investigation Report and allegations contained in the complaint, the learned Special Court was pleased to summon the applicant u/s. 36(c) read with Section 447 of the Companies Act, 2013 vide summoning orders dated 16.08.2019.

The applicant filed his bail application and sought to be supplied with the complete Charge Sheet in accordance with his rights u/s. 207/208 Cr.PC.

Conclusion-

A bare perusal of the above answer shows that the Punjab National Bank (PNB) did not lay much emphasis to the audit report given by the applicant. Even if I see the audit report, the audit report shows that the applicant had raised serious issues, and no loan should have been advanced based on the asset classification and Position of Accounts in the stock audit report.

I am of the view that since the ex-promoters/directors and similarly situated chartered accountants have been granted bail, there is no reason why the Applicant should be treated any differently.

FULL TEXT OF THE JUDGMENT/ORDER OF DELHI HIGH COURT

1. This is an application filed seeking grant of regular bail to the applicant (accused No. 200 in Complaint Case No. 770/2019 titled as “Serious Fraud Investigation Office vs. Bhushan Steel Limited and Others”.

2. The applicant is a senior citizen and Chartered Accountant (C.A.) by profession with private practice.

3. The facts in brief are:

3.1 M/s Bhushan Steel Limited (hereinafter “BSL”) is a company under investigation on account of allegations of siphoning off by its promoters.

3.2 In brief, the allegation against the applicant is that he being a Chartered Accountant and one of the partners at ASRN & Associates [the firm appointed as stock auditors by the consortium of banks led by Punjab National Bank (hereinafter “PNB”) for Financial Year 2015-16] failed to perform his duty independently and diligently by not verifying the stock in transit, and he is accused to be in collusion with the office bearers of M/s Bhushan Steel Limited.

3.3 It is stated that he is involved in providing and using wrong information to calculate the Drawing Power figures wrongly based on the figures given by M/s Bhushan Steel Limited.

3.4 A complaint dated 01.07.2019 was filed under Section 439(2) read with Section 436(1)(a),(d) and (2) read with Section 212(15) of the Companies Act, 2013 read with Section 621(1) of the Companies Act, 2013, read with Section 193 of the Code of Criminal Procedure, 1973 by the respondent, Serious Fraud Investigation Office (SFIO). The respondent also relies upon Investigation Report dated 27.06.2019 filed with the Ministry of Corporate Affairs.

3.5 As per the complaint, the allegations against the petitioner are as under:-

“32. On account of inter alia, the deprivation of finances to A-01Bhushan Steel Ltd., the financial position of Company deteriorated. However, despite this, the financial statements of A01 Bhushan Steel Ltd indicated increasing figures against Stock-in- Transit (“SIT”), both in absolute terms and as a percentage of turnover, especially in the financial years F.Y 2013 14, 2014-15 and 2015-16. The “SIT” is shown at Rs. 3823.48 Cr., Rs. 5093.46 Cr. and Rs. 6523.20 Cr. respectively. Investigation established that figures shown under “SIT” used to be inflated by making false entries in the books of accounts maintained in SAP and Foxpro Legacy. With these manipulated figures A-01 Bhushan Steel Ltd during the F.Y 2013-14 to 2015-16 was able to avail Drawing Power (“DP”) against cash credit facility. This conspiracy of availing “DP” by filing inflated figures was hatched by A-158 Brij Bhushan Singal, A- 159 Neeraj Singal, A160 Nittin Johari, A- 179 Pankaj Tewari. A- 161 Pankaj Kumar Agarwal, A- 190 Pankaj Mahajan and A-200 Sunil Bhatia, stock auditors and A- 186 R.K Mehra and A- 188 M.P. Mehrotra, statutory auditors. At all material time they were aware that the amount shown under SIT in inflated in the books of accounts.

71. Further, as detailed above, A-158 Brij Bhushan Singal A 159 Neeraj Singal, the ex-promoters of BSL, along with A-160 Nitin Johari, ex- Whole Time Director and Chief Financial officer (CFO) of BSL in active connivance with employees of A-1 BSL, namely, A-181 Vivek Mittal, A- 180 Saurabh Mittal, A-179 Pankaj Tewari, A-184 Rajat Jain, A-183 Sunil Agarwal and A185 Rajesh Sharma have filed various false, deceptive statements and misleading information to various banks, to avail/ continue to avail working capital limits from 2013-14 till 2015-16. All the aforesaid accused persons, at all material time, were well aware about the financial position of A-01, BSL and non-existent stocks but nevertheless, induced the banks to sanction total Drawing Power (DP) against Fund Bank Working Capital limits of Rs. 5389 crore, 5606 crore and 5527 crore against which it had cash credit outstanding of Rs. 5761 crore, Rs. 7094 crore and Rs. 9768 crore respectively. This was secured inter alia against the non-existent Raw Material (Stock in-Transit) which caused wrongful loss to lenders.

72. The Stock Auditors A-199 Pankaj Mahajan, CA and A-200 Sunil Bhatia, CA appointed by the Banks also colluded with the above-mentioned accused and did not discharge their duties diligently.

73. A-158 Brij Bhushan Singal, A-159 Neeraj Singal, A-160 Nitin Johri, A-161 Pankaj Kumar Aggarwal, A-179 Pankaj Tewari, A-183 Sunil Agarwal, A-184 Rajat Jain, A-185 Rajesh Sharma, A-181 Vivek Mittal, A-180 Saurabh Mittal of BSL, alongwith A-186 R.K. Mehra, CA of Mehra Goel & Co., connived in making false, misleading statements relating to Stock-in-Transit for the credit facilities availed from bankers during the period covering F.Y. 2013-14 to 2015-16.

74. Thus A-1 BSL, A-158 Brij Bhushan Singal, A-159 Neeraj Singal, A-160 Nittin Johari, A-181 Vivek Mittal, A-180 Saruabh Mittal, A-179 Pankaj Tewari, A-183 Sunil Aggarwal, A-184 Rajat Jain, A-185 Rajesh Sharma, A-190 Pankaj Mahajan, A-200 Sunil Bhatia, A-186 R.K. Mehra, A-161 Pankaj Kumar Aggarwal are liable for fraudulent inducement of creditors as laid down in Section 36 (c) of Companies Act 2013 and are liable to be punished u/s 447 of the Companies Act, 2013.”

3.6 The Investigation Report records as under:-

“OBSERVATION ON THE STOCK AUDIT REPORT OF M/S ASRN & ASSOCIATES, CHARTERED ACCOUNTANTS

4.12 Based on the statement and the Stock Audit report, the following observations are made on the report submitted by M/S ASRN & Associates, Chartered Accountants:

> The movement of stocks for intervening period was not taken by the auditor.

> The auditor confirmed that due to pressure from the Bank to conclude the Stock Audit, certain norms for verifying the stock positions was not taken care by them.

> The Stocks at Jawaharlal Nehru Port, Mumbai could not be verified due to strike. The company could not provide the full details of supporting documents regarding ownership of the stock i.e., like invoices and bill of entry. M/s ASRN & Associates verified the stock on test check basis and hence they had relied upon the stock position given by the management.

> The stock in transit was also verified as per the information/ data provided by the Management of BSL. However, certain bills/invoices were verified as the auditors were not provided with supporting documents to the extent of stocks lying in transit i.e. Rs 5389.58 Crore. The stock auditors were told by the management and the bank to cover the DP therefore, the stock positions shown in the stock in transit is actually not correct.

> The physical stock in transit could not be verified as the company could not provide supporting documents such as invoices and bill of entries etc. for claiming the same.

> The goods received under LC were devolved to the extent of Rs. 3,676.61 and the amount was paid by the bank, hence, it is not paid stock and it should have been excluded for the purpose of arriving DP. The banks and the management had expressed their concern if this devolved liability excluded for the purpose of DP, the DP should have gone down to the extent above. Hence, the same was taken for DP purpose.

> In view of the above facts the Stock Auditors M/s ASRN & Associates have failed to discharge their legitimate duties to prepare the audit report impartially and against norms of Audit Principles and ignore the serious irregularities in the stock audit report. Hence, he is responsible for the lapses.

5.1.14. Investigation revealed that the Stock Auditors, Sunil Bhatia, a partner of firm of M/s ASRN & Associates conducted the stock audit on behalf of PNB for the period of “BSL” as on 30.09.2016. The auditors failed to verify the supporting documents of “SIT” which “BSL” had shown at Rs.5389.58 crore (refer para 4.4 (Table No. 4.7) of factual matrix) specifically keeping in view the nature of account of “BSL” which was classified as “Non-Performing Asset since 1.10.2014/Doubtful”.

5.1.15. Thus, both the Stock Auditors, failed to perform their duties independently and diligently by not verifying the stock in transit, and thereby colluded with the officers of “BSL” in providing and using the wrong information to calculate the DP figures wrongly based on the figures given by “BSL” management. The Stock Auditors also got influenced and did not perform their assigned duty diligently and professionally.”

3.7 Based on the conclusions in the Investigation Report and allegations contained in the complaint, the learned Special Court was pleased to summon the applicant under Section 36(c) read with Section 447 of the Companies Act, 2013vide summoning orders dated 16.08.2019.

3.8 The applicant filed his bail application and sought to be supplied with the complete Charge Sheet in accordance with his rights under Section 207/208 Cr.PC.

3.9 It is submitted that the Charge Sheet is approximately of 60,000 pages, and in February 2022, the learned Special Court directed the applicant to conduct physical inspection of the voluminous record every Thursday from 12 Noon to 4 PM till 31.05.2022.

3.10 The inspection was conducted by applicant’s counsel on numerous dates, and on numerous occasions, the inspection could not be conducted as officers of SFIO were not present.

3.11 On 08.04.2022, the learned Special Court directed as under:-

“I am fixing two dates of hearing i.e. 01.06.2022 and 04.07.2022 for arguments on the bail applications. I note that on 01.06.2022 first arguments shall be advanced on the applications under Section 207 Cr.PC pending qua any of these accused persons and thereafter arguments on the bail application shall be heard.

I further note that if arguments on the bail application are not concluded on the said, the remaining accused persons shall argue their bail applications on 04.07.2022.

Now list this matter on 01.06.2022 for arguments on the pending applications qua A-190 to A-203.”

3.12 On 01.06.2022, the applicant went to attend the Court proceedings, but the learned Special Judge was pleased to hear the arguments on bail application and dismissed the same and took the applicant in judicial custody.

4. This Court on 06.06.2022 was pleased to direct issuance of notice, and on 13.06.2022, this Court directed the matter to be listed on 24.06.2022.

5. The Hon’ble Supreme Court on 17.06.2022 directed this Court to hear and decide the bail application filed by the petitioner on 24.06.2022.

6. Accordingly, and as per the directions of the Hon’ble Supreme Court, I have heard Mr. P.V. Kapur, learned senior counsel for the applicant and Mr. Ripu Daman Bhardwaj, learned CGSC appearing for the respondent.

7. Mr. Kapur, learned senior counsel for the applicant submits that at the outset, the complaint against the petitioner is not maintainable.

7.1 He submits that as per the complaint, the main allegation is that the promoters of BSL, along with some other accused persons, filed various false deceptive statements and misleading information to various banks to avail and continue to avail working capital limits from 2013-14 till 2015-16.It is further alleged that the applicant‟s firm was appointed by the bank, Punjab National Bank, and they colluded with the BSL and did not discharge their duties diligently. The issue under investigation in the case of M/s Bhushan Steel Limited was1.9 xv – “Role of Stock auditor who conduct audit of BSL in the F.Y. 2014-15 & 2015-16.”.

7.2 He submits that a bare perusal of the appointment letter dated 29.10.2016 shows that the applicant was appointed as a Stock Auditor for conducting stock audit for the year 2016-17. The terms of appointment were as under:-

“(Appointment Letter dt. 29.10.2016)

| PUNJAB NATIONAL BANK Large Corporate Branch, Tolstoy House, New Delhi-110001 | Email:bo2164@pnb.co.in Ph:91-11-23752604, 23311654 Fax:91-11-23323480/41522135 |

LCB/Stock Audit

M/s ASRN & Associates

Chartered Accountants

608, Padma Towers – I

Rajindra Place New Delhi

Dear Sir,

Reg. Stock Audit as at 31.10.2016

We have pleasure to appoint you as Stock Auditor of M/s Bhushan Steels Ltd. (Shri Pankaj Tiwan) Phone No. 8588870836) for conducting stock audit for the year 2016-17.

The Proforma of Stock Audit Report along with Checklist/ Scope of Stock Audit and Terms of Reference is enclosed. The audit may be completed within 2 weeks and report be submitted immediately after completion of audit but in no case later than two weeks of completion of audit Irregularities observed during the stock audit may be discussed with the Relationship Manager at our branch. In case of major deficiencies, if any, in the stock/ receivables, the same be informed to our office by fax. The Stock audit should be conducted was reference to the stock as at 31.10.2016.

The fees including travelling boarding, lodging and other miscellaneous expenses will be payable as per bank guidelines with the consent of the barrower.

If you are willing to accept this offer, kindly submit your acceptance letter immediately i.e. within 5 days of the receipt of this letter by fax/courier. If no acceptance is received within 10 days from the date of this letter, it will be presumed that you are not interested in the offer and the arrangement will, therefore, be automatically cancelled.

It may please be noted that this offer is one time offer and no further work should be undertaken by you without our express permission.

Please call on the concerned RMs/ SRMs before starting the stock audit to discuss details.

We solicit your cooperation in conducting the stock audit in an effective manner.

Thanking you,

Yours sincerely,

Sd/-

Asstt. General Manager

Copy to M/s Bhushan Steels Ltd., Bhushan Centre, Ground Floor, Hyatt Regency Complex, Bhikaiji Cama Place, New Delhi) for information please. Kindly provide full cooperation to the stock auditors in their task.

Asstt. General Manager”

7.3 The appointment letter clearly shows that the applicant was not an Auditor of M/s Bhushan Steel Limited during the period under investigation i.e. Financial Year 2013-14 to 2015-16. The counsel has relied on the judgment of the High Court of Delhi, Gaurav Kumar v. Serious Fraud Investigation Office [MANU/DE/4412/2019] to show that the applicant cannot be held liable for acts done during a period which did not concern them.

7.4 The Stock Audit Report dated 15.02.2017 by ASRN & Associates was for the period dated 1st April 2016 to 31st October 2016 and had no relevance whatsoever to the FY 2013-14 to FY 2015-16 which is the period under investigation in the complaint.

7.5 As regards to the allegation that no physical verification of the stock has been done by the Auditor, the Ld. Senior counsel submits that as per the “Implementation Guide to Standard on Audit (SA) 530 Audit Sampling” issued by the Institute of Chartered Accountants of India, the auditor is not expected or required to carry out physical verification of each and every transaction having regard to the fact that the volume and spread of transactions in modern businesses are incredibly enormous. In such cases, it is recommended by the Institute that only “test check” be carried out.

7.6 Additionally, the Stock Audit Report by the applicant‟s firm, discloses the Asset Classification of BSL as “Non Performing Asset since 01.10.2014/Doubtful”.

8. In opposition to the grant of bail, Mr. Ripu Daman Bhardwaj, the Ld. CGSC has submitted the following arguments.

8.1 The period of stock audit of BSL was as on 30.09.2016. The visits of the stock auditor to company plants commenced from Dec. 2016 onwards and the last visit was on 15.02.2017 and report was submitted on 15.02.2017. Hence, there is a gap of more than 3 months from the date of his commencement, and he has not taken stock statement of December 2016 and reconciled the stocks backward. The movement of stocks for intervening period was not taken into account.

8.2 The applicant did not do any physical stock verification and relied upon the stock position given by BSL.

8.3 The stock auditor did not check the records to substantiate claim of consumption of such huge quantity of coal, and they also failed to check the bills of stock in transit of Rs. 5,389.58 Crore during stock audit assigned. Further, it is odd that the company would have huge quantities of coal and other stocks appearing in stock in transit amounting to Rs. 5389.58 Crore during the month of September 2016 alone, specifically when company was in financial crunch.

8.4 The counsel has relied upon the judgment of Satender Kumar Antil v. Central Bureau of Investigation & Anr. [(2021) 10 SCC 773] and Serious Fraud Investigation Office v. Nittin Johari &Anr. [(2019) 9 SCC 165]to state that the rigours of 212(6) of the Company Act, 2013have to be met and economic offences are a crime of grave and serious nature which should also be considered.

ANALYSIS:-

9. I have heard the learned senior counsel, Mr. P.V. Kapur for the Petitioner and the Ld. CGSC, Mr. Ripu Daman Bhardwaj for the Respondent and gone through their submissions and documents.

10. At the outset, for grant of bail, the twin conditions under section 212(6) of the Companies Act, 2013 have to be met:-

“Section 212. INVESTIGATION INTO AFFAIRS OF COMPANY BY SERIOUS FRAUD INVESTIGATION OFFICE

(6) Notwithstanding anything contained in the Code of Criminal Procedure, 1973 (2 of 1974), [offence covered under section 447] of this Act shall be cognizable and no person accused of any offense under those sections shall be released on bail or on his own bond unless-

i. the Public Prosecutor has been given an opportunity to oppose the application for such release; and

ii. where the Public Prosecutor opposed the application, the court is satisfied that there are reasonable grounds for believing that he is not guilty of such offense and that he is not likely to commit any offence while on bail:…”

11. I think this a case where the applicant needs to be enlarged on bail for the following reasons:

11.1 The Applicant was appointed as a stock auditor vide appointment letter dated 29.10.2016 for conducting stock audit of BSL for the year 2016 – 2017. As per the Stock Audit Report dated 15.02.2017 by the applicant firm it pertained to the period 01.04.2016 to 31.10.2016. Hence, the stock audit report did not pertain to the period under investigation. The observations of Gaurav Kumar (supra) are relevant and read as under:

“48. The contention raised on behalf of the petitioner that the assignment was received by the applicant in February-March, 2016 and that the applicant could thus not be liable for the statutory record which was filed in the year 2008-09 to 2014-15 available on the MCA website cannot be overlooked in as much as the role attributed against the applicant by the SFIO commenced only from February-March, 2016….”

11.2 This was the first appointment of the applicant and he was not an auditor of BSL prior to the said date. Mr. Rajan Malhotra, who was the relationship manager at PNB, states:

“Q. no. 11 In reference to your answer to question no. 10, please state since you was relationship manager, why you had accepted the stock audit report. Whether you consider the verification of stock auditor from other entity.

Ans: It is correct that company was under financial stress and no further exposure was extended, so not much emphasis was given to this audit report. Further, I would like to submit stock audit report was shared with all the lenders and the same has not been closed.”

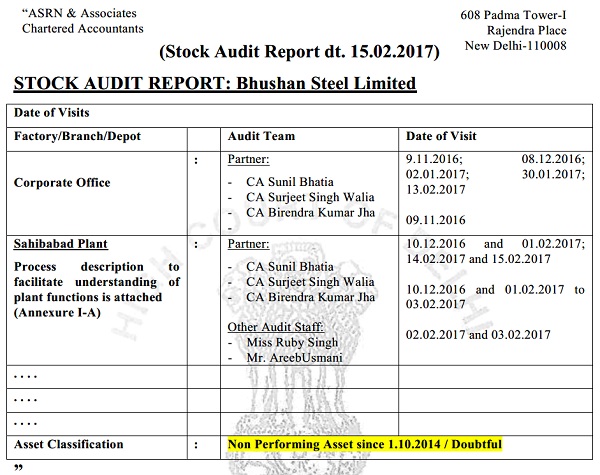

A bare perusal of the above answer shows that the Punjab National Bank (PNB) did not lay much emphasis to the audit report given by the applicant. Even if I see the audit report, the audit report shows that the applicant had raised serious issues, and no loan should have been advanced based on the asset classification and Position of Accounts in the stock audit report. The asset classification of the report reads as under:-

“ASRN & Associates

Chartered Accountants

608 Padma Tower-I

Rajendra Place

New Delhi-110008

(Stock Audit Report dt. 15.02.2017)

STOCK AUDIT REPORT: Bhushan Steel Limited

ASRN & Associates have also shown the irregularities in the Position of Account:

11.3 Additionally, the main stakeholders of both the companyi.e. BSL and the Bank i.e. PNB have been enlarged on bail/interim bail:

a. Interim relief granted till pendency of proceedings to ex-promoter/director of the company, Neeraj Singal by the Hon‟ble Supreme Court on 04.09.2018 in SLP (Crl.) No. 7241 of 2018.

b. On grounds of parity, co-accused, Nittin Johari, ex-promoter of BSLin the same case was granted bail in the matter, Vijay Madanlal Chaudhary &Ors. v. Union of India &Ors. dated 18.08.2021[MANU/SCOR/25854/2021].

c. Additionally, the same summoning order dated 16.08.2019 has been quashed by a coordinate bench of this court against Dr. Rajesh Kumar Yaduvanshi, who was a Nominee Director appointed PNB on the board of BSL.[ Rajesh Kumar Yaduvanshi v. SFIO, CRL. REV.P. No. 1308 of 2019 vide order dated 21.09.2020].

d. Co-accused, Mr. Pankaj Mahajan who is also a practicing Chartered Accountant at the firm, M/s. A.C. Gupta & Associates is also admitted on bail by a coordinate bench of this court in BAIL APPLN No. 1813 of 2022 titled Pankaj Mahajan v. SFIO dated 29.06.2022.

e. A coordinate bench of this court also enlarged Rupesh Purwar, co-accused no. 203 on bail. He was signatory to the Financial Statements of the company for the FY 2013-14 and 2014-15 in his capacity as the Company Secretary, which he had signed for the purpose of regulatory filing of the Company. [Rupesh Purwar v. SFIO, CRL. M.C. No. 2878 of 2022 dated 29.06.2022]

11.4 I am of the view that since the ex-promoters/directors and similarly situated chartered accountants have been granted bail, there is no reason why the Applicant should be treated any differently.

12. The judgment relied upon by Mr. Kapur, learned senior counsel for the applicant on Jainam Rathod vs. State of Haryana and Ors. [SLP (Crl No. 1554/2022, Order dated 18.04.2022) ]also helps the petitioner as it has been held:-

„8 In this backdrop, in the absence of a fair likelihood of the trial being completed within a reasonable period, this Court must be mindful of the need to protect the personal liberty of the accused in the face of a delay in the conclusion of the trial. We are inclined to grant bail on the above ground having regard to the fact that the appellant has been in custody since 28 August 2019. In Nittin Johari (supra), this Court has held:

“24. At this juncture, it must be noted that even as per Section 212(7) of the Companies Act, the limitation under Section 212(6) with respect to grant of bail is in addition to those already provided in CrPC. Thus, it is necessary to advert to the principles governing the grant of bail under Section 439 of CrPC. Specifically, heed must be paid to the stringent view taken by this Court towards grant of bail with respect of economic offences.”

While the provisions of Section 212(6) of the Companies Act 2013 must be borne in mind, equally, it is necessary to protect the constitutional right to an expeditious trial in a situation where a large number of accused implicated in a criminal trial would necessarily result in a delay in its conclusion. The role of the appellant must be distinguished from the role of the main accused.‟

13. The summoning order was issued on 16.08.2019 and the Applicant had not been arrested till 01.06.2022 without there being any protection in favour of the Applicant. There is also no reason shown for seeking judicial custody of the Applicant.

14. As regards the legal embargo of Section 212(6), I am of the view that Sub-section-(i) has duly been complied with, as the Public Prosecutor (Ld. CGSC) has been given a chance to oppose the bail application. I am prima facie of the view that the Applicant is not guilty of the offence of which he is charged with, and therefore, I am also of the opinion, that he is not likely to commit any further offence while on bail. Hence, sub-section (ii) of Section 212(6) is also complied with, notwithstanding the observations of Jainam Rathod(supra).

15. In view of my analysis above, I do not find merit in the contentions and submissions of the learned CGSC.

16. The application is allowed. The Applicant, Mr. Sunil Bhatia (accused no. 200) in complaint case no. 770/2019 is enlarged on bail subject to the following conditions:

i. The applicant shall furnish a personal bond with two local sureties in the sum of Rs. 25,000/- each, to the satisfaction of the Trial Court;

ii. He shall appear before the Court as and when directed;

iii. In case he changes his address, he will inform the IO concerned and this Court also;

17. The application stands disposed of in the aforesaid terms.

18. Since regular bail has been granted, the application for interim bail in CRL. M. (BAIL) – 737/2022 is now infructuous.