Synopsis

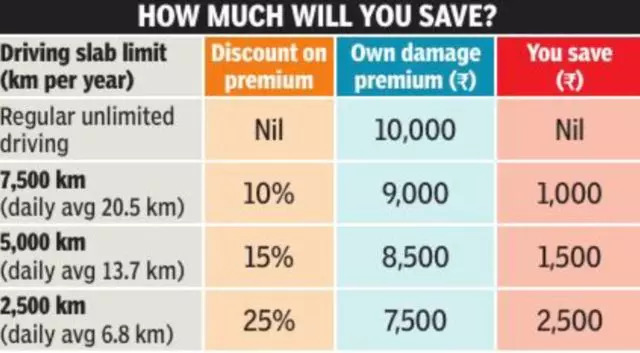

Pay-as-you-drive policies allow buyers to set a mileage limit for their car and offer them discounts over the normal premium. The lower the limit, the bigger the discount over the normal premium. The insurance is valid only up to the limit chosen by the buyer. One insurance company offers three slabs of 7,500 km, 5,000 km and 2,500 km.

(This story originally appeared inon Jul 13, 2022)

NEW DELHI: Your car insurance premium could soon be decided by how much and how well you drive. The Insurance Regulatory and Development Authority of India (Irdai) has permitted insurers to launch pay-as-you-drive motor insurance policies with premiums linked to mileage and quality of driving.

Pay-as-you-drive policies allow buyers to set a mileage limit for their car and offer them discounts over the normal premium. The lower the limit, the bigger the discount over the normal premium. The insurance is valid only up to the limit chosen by the buyer. One insurance company offers three slabs of 7,500 km, 5,000 km and 2,500 km.

Insurance companies can also offer discounts based on the quality of driving. A telematics device is fitted in the car to monitor the condition of the vehicle and the driving habits of the user. This data is then interpreted to give discounts to careful drivers. It can also penalise rash and negligent drivers.

These developments seem good news for those who own multiple vehicles or have not been driving too much due to Covid restrictions. They won’t have to shell out the full premium if their vehicles are not being used too much. “The introduction of these options will aid in giving the much-needed fi llip to motor Own Damage cover in the country and increase its penetration,” Irdai said in a statement.

However, the discounts offered on the premium are not too exciting (see table). If you choose the 7,500 km slab, you get only a small 10% off on the regular premium. Mind you, the discount only applies to the ‘own damage’ premium, and the mandatory third-party premium and other add-on covers are not affected.

The discount is a little more attractive for a lower limit of 2,500 km, but that works out to an average drive of less than 7 km in a day. Consider that before you opt for a policy with a low slab.

The good news is that buyers can switch to a higher slab or even to a regular unlimited policy if they end up driving more than the slab limit. But this upgrade should be done well before time. It is not possible to upgrade after a mishap or claim incident.

The installation of telematics devices also raises privacy concerns for the car owner. No doubt it will reduce the insurance premium, but this discount comes at a cost. Go for it only if you are comfortable with the thought that the insurer will have 24x7 data on your car’s movement.