Clipped from: https://economictimes.indiatimes.com/opinion/et-commentary/impossible-trinity-returns-to-test-rbi/articleshow/92722234.cms

Synopsis

Law mandates the RBI to keep inflation at 4% which it forecasts to be 6.7% this fiscal. To get to target, it has to raise interest rates sharply which it is reluctant to as it aims for a durable economic recovery. For the currency to be stable it has to attract overseas funds with higher interest rates.

MC Govardhana Rangan

The author is a post-graduate in Economics and has been a financial markets journalist for more than 25 years.

Is it Déjà vu 2013, 2008, 1997? That’s what has begun to swirl in the minds of those that have witnessed those years in the financial markets after the Reserve Bank of India (RBI) revealed its mind on Wednesday.

When the central bank is open about its intentions to welcome more foreign exchange when Taper Tantrum 2.0 might well be playing out in markets as far apart as Jakarta and Johannesburg, some view the latest suite of measures from the RBI as indicative of its ability to see the future. But then there are others that believe that the measures point to brewing trouble.

To be sure, the Indian Rupee, down about 6 percent this year, is relatively stable when the Dollar Index DXY is up 11.4 percent. The equities market has so far withstood the sell-off by overseas investors. Bond yields spiked to 7.60 percent, but the increase is mild given the inflation rate. Above all, foreign exchange reserves are at $593.3 billion as on June 24. It was less than half when Ben Bernanke spoke about unwinding the Quantitative Easing in 2013.

Given this set up, why did the RBI lift the cap on interest rates on deposits from overseas Indians? What is the need for doubling limits under the External Commercial Borrowing programme for companies? What would widening of bonds securities pool for foreign investment do when already there’s room?

The consensus is that the RBI may be uncomfortable to see the rupee breach the 80 mark to the US dollar. It doesn’t want to deplete reserves defending a currency level. And act in advance to nip a potential crisis in the bud.

“While the Rupee has outperformed other currencies recently, we speculate that India’s political economy likely prefers some stability in USD-INR,” said Ananth Narayan, Finance Professor at SPJIMR, a management institute. “We see these steps as further reiteration of this priority.”

While the move to raise the foreign exchange buffer is a well-intentioned one, during times of heightened volatility, financial markets could begin to drive in the opposite direction. Central bank actions have to succeed for them to have the desired impact on markets. If they don’t, the outcomes could be worse than what it would have been otherwise.

Will the banks raise interest rates on deposits by overseas Indians to attract US dollars? When the financial markets are swinging wildly, will the banks expose themselves to adverse currency movements? That was the contentious issue in all previous crises.

The RBI has added the 7-year and 14-year government bonds that would be available for foreign investors under the automatic route. When the asset swap arbitrage is narrow it is doubtful how much would flow through this route. Overseas investors own Rs. 51,640 crores of bonds in this segment, data from CCIL shows.

Furthermore, when Indian interest rates are held relatively benign for a stable economic recovery, companies’ External Commercial Borrowing limit has been doubled to $1.5 billion which may not be an incentive given hedging costs.

“Foreign portfolio inflows have been lukewarm to debt, with net outflows for the past six months and existing debt limits still to be exhausted,’’ says Radhika Rao, economist at DBS Bank.

When risk-off is the dominant theme in the market for now, the impact of these measures would be critical.

The RBI’s shot across the bow may have been warranted more due to flashes of red in the real economy than in financial markets. Trade deficit is at a record monthly high. Fiscal deficit target could be tested given unbudgeted ballooning subsidies. Historically, these twin deficits were key to breaking the currency.

Central bank ammunitions are to be used sparingly for them to be effective. And timing is a key component.

One lingering question in this episode would be why the RBI revealed its hand a day after Crude oil, the biggest factor in the CAD, tumbled 9% on fears of a global recession. Couldn’t it have waited even if the plan was ready? Many of the commodities are down more than a third from their peaks. Bets on Fed turning next year to counter a recession are growing.

Assuming the move to raise USD inflows has the desired effect, what could be in store? The RBI has to suck out the USD that would increase liquidity in the domestic market, weakening its fight against inflation.

If there’s not much inflows despite these moves, the markets could be emboldened to test the RBI beyond Rs. 80 to the Dollar as it has signalled its intention to not throw away existing reserves to defend the Rupee in the short term.

Law mandates the RBI to keep inflation at 4% which it forecasts to be 6.7% this fiscal. To get to target, it has to raise interest rates sharply which it is reluctant to as it aims for a durable economic recovery. For the currency to be stable it has to attract overseas funds with higher interest rates.

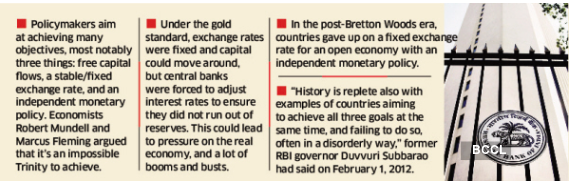

Is it the classic case of Robert Mundell’s Impossible

at play?

(Views are personal)