SynopsisThe new tax regime has two main differentiating aspects. First, it offers more tax slabs. Second, it takes away all the exemptions and deductions available under Section 80, which is popular among taxpayers. So, if the cash in hand after adopting the new tax regime turns out to be higher than the benefit of tax deductions and exemptions available in the old tax regime, the taxpayer might choose the new tax regime.

The Finance Act of 2020 included a new section, 115BAC, that created a new tax regime. The primary characteristic of this new system is reduced tax rates when compared with the existing slab rates. However, assesses adopting the new tax regime must sacrifice around 70 exemptions and deductions under Section 80. The new tax regime was introduced at the beginning of assessment year 2021-22. It applied to individuals and HUFs irrespective of their residential status. However, the scheme is optional; a taxpayer can continue to use the traditional tax regime. The transition from one system to another is permitted under certain conditions.

The new tax regime has two main differentiating aspects. First, it offers more tax slabs. Second, it takes away all the exemptions and deductions available under Section 80, which is popular among taxpayers. So, if the cash in hand after adopting the new tax regime turns out to be higher than the benefit of tax deductions and exemptions available in the old tax regime, the taxpayer might choose the new tax regime.

Equity linked savings scheme (ELSS) is one avenue that enjoys tax benefits under Section 80C. The section provides a deduction for tax-paying individuals/HUFs who invest up to Rs 1.5 lakh in ELSS each year. It also looks like a more relevant tax exemption for the younger population, who may not yet be in a phase of life where exemptions such as home loan principal repayment, children’s tuition fees can be availed.

ELSS benefits both the government as well as the taxpayers. The government promotes savings through this section, and individuals have to pay tax on a lower income. The only catch with ELSS investments is its minimum lock-in period.

As the name suggests, ELSS funds invest in equity markets. The returns are linked to the performance of a fund’s underlying stocks. The fund is managed by fund managers assigned by the respective asset management companies (AMCs).

ELSS has a mandatory lock-in period of 3 years. In the case of a systematic investment plan (SIP) in ELSS, only the tranches that are more than three years old can be redeemed. Ideally, the investment horizon in ELSS should be longer than the lock-in period based on the type of fund chosen. ELSS funds can be large-cap oriented or flexi-cap oriented. However, some investors who prefer liquidity in their portfolios would not want to invest in ELSS funds if these give no tax incentives.

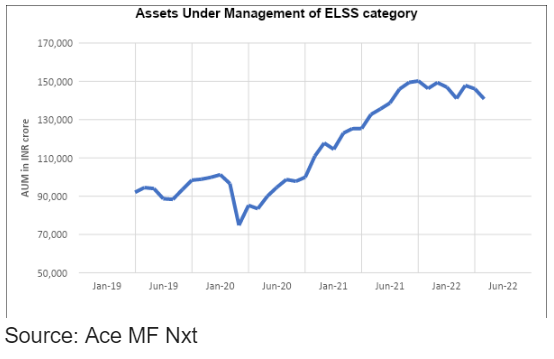

To understand the quantum of the funds being managed in this fifth most significant category of mutual funds, take a look at this chart showing the AUM trend over years:

ET CONTRIBUTORS

The tax incentive provided by the government has attracted more investments into this category of mutual funds over the years. The AUMs in this category as on May 31, 2022, were a whopping Rs 1,408 lakh crore. Most of the inflows are seen during the March quarter, which is when many people do tax planning. A sizable chunk also flows through the year in the form of SIPs.

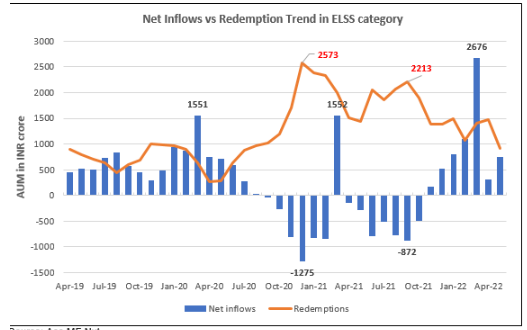

Below is the chart showing the net inflows in the category in the past three years:

ET CONTRIBUTORS

As can be seen clearly in the above chart, the inflows during the March quarter are usually higher. However, this trend also suggests that if the tax incentives are absent, there is a high probability that these inflows might not be as healthy as they are now. Additionally, redemptions might also start increasing as there might be mobilisation of funds to a different asset with a better risk-reward ratio.

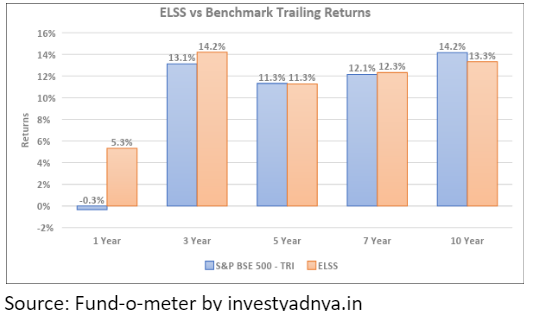

The intent of every investment is to generate decent returns while considering the risk-reward ratio. When we look at the returns generated by the direct funds in the ELSS category, we notice a CAGR of around 14.2% in the last 3 years, as on June 14, 2022, which looks decent enough. But let us compare these returns with its benchmark – S&P BSE 500 TRI. A few things to note before we compare:

- While analysing the ELSS category, one can notice ELSS funds majorly invest in large and midcaps, with an average allocation of 65% and 20%, respectively.

- On the other hand, the benchmark S&P BSE 500 TRI consists of around 250 smallcap companies. And so the short-term benchmark returns seem low due to the sharp fall in smallcap companies in the recent market fall. Due to this, ELSS funds currently look better placed when we see recent trailing returns.

Below are the comparative trailing returns of the benchmark vs the ELSS category as in June 14, 2022:

ET CONTRIBUTORS

ELSS looks good when compared with the benchmark in 1-year and 3-year trailing returns. In the 7-year period, the difference is insignificant. It is also essential to look at the calendar returns to understand the performance in a better way.

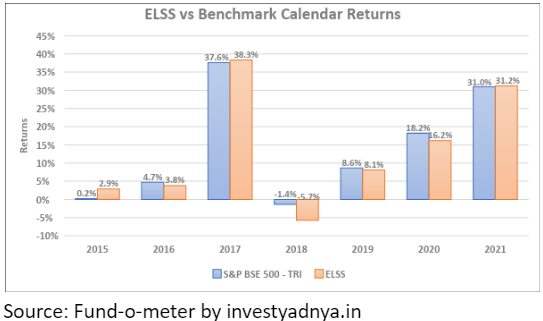

Below is the chart showing the calendar returns of both the ELSS category and the benchmark:

ET CONTRIBUTORS

As can be seen, in calendar returns, the ELSS category has not been able to beat the benchmark in more than 2 years and has at par return year of 2021. From another angle, the ELSS category has locked-in funds, which help the fund manager to take long-term bets with lower redemption pressures during volatile markets. The lock-in also helps manage expected returns and risks are taken in a better way when compared with other categories. But this is not translating into better returns, as can be seen from both the returns’ graphs.

The significance of this category is not limited to tax incentives, but it also forms a platform for many first-time investors. The scheme works as a gateway for new investors who would have otherwise refrained from entering volatile equity markets. The government benefits when people develop saving and investing habits; the dependence on government resources reduces after their retirement.

Due to its volatile nature, the equity market can bring first-time investors onto their toes every time the market moves up or down. However, the 3-year lock-in for ELSS funds helps first-time investors manage their behaviour and also see the kind of returns equity funds can generate if they had stayed invested for a longer duration.

Having said all this, the availability of more cash and more investment choices provided by the new tax regime will decide the kind of inflows the ELSS category would see from younger taxpayers. Once the tax incentive is not in the picture, ELSS seems like any other equity fund.

(The authors, Gaurav Jain & Parimal Ade are Founders, InvestYadnya.in. Views are their own)

Disclaimer: The information here is provided for reference purposes only and should not be misconstrued as investment advice. Under no circumstances does this information represent a recommendation to buy or sell stocks or MF.

(Disclaimer: The opinions expressed in this column are that of the writer. The facts and opinions expressed here do not reflect the views of www.economictimes.com.)

Share the joy of reading! Gift this story to your friends & peers with a personalized message. Gift Now