Clipped from: https://timesofindia.indiatimes.com/business/india-business/slowly-slowly-manage-rupee/articleshow/92661048.cms

With oil prices up, a record trade deficit of $70.25 billion in the April-June quarter, rupee sliding and GoI taking some policy calls, India’s responses to external sector challenges are crucial. Here’s how to read the problem.

How critical is the impact of energy price surge?

It is a severe headwind. Net energy imports were $150 billion last year, 5% of GDP. If prices remain elevated for a year, this can rise by nearly $80 billion. This creates two somewhat related problems, which need different solutions.

- First, a drag on domestic demand, as Indians cut down on consumption of other products to pay more for fuel, coal, fertilisers and edible oil.

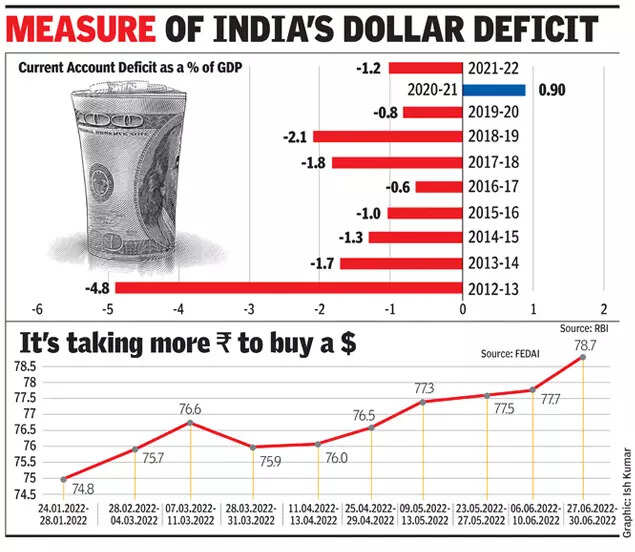

- Second, a balance-of-payments deficit: the demand-supply of dollars. India collectively consumes more than it produces, imports more than it exports, paying for it by selling assets to foreign investors or companies or borrowing in dollars. Given higher energy prices, India needs more dollars to pay for it. From a reasonable surplus before February, India now runs a $45 billion deficit per year, nearly 1.5% of GDP.

How will various GoI measures affect the economy?

Announcements made in the last three months to support domestic demand add up to nearly $70 billion, or Rs 5.5 trillion. Of this, fiscal measures are Rs 4 trillion. A fuel excise cut of Rs 1 trillion, an additional Rs 0.5 trillion cut in fuel taxes by states, Rs 1.2 trillion of additional fertiliser subsidies, Rs 0.8 trillion of additional free grains, and Rs 0.5 trillion of implied power subsidies as power tariffs remain largely unchanged even as high-priced coal imports rise.

Such measures are consistent with global trends. Nearly every economy is now subsidising energy prices to prevent a sharp slowdown in their economies: GDP growth needs use of dense energy. The challenge of course is that if everyone subsidises energy demand, prices may remain higher for longer.

An additional Rs 1.5 trillion of demand support has been through export duties in sectors where India is a net exporter and global shortages have pushed up profit margins: first steel, and now refined petroleum products. These in effect shift companies’ profits to consumers without going through the government budget. If 15% export duty on steel brings prices in India $90 below global prices, it means steel consumers will pay $10 billion less than they would have on a volume of 110 million tonnes. Similarly, export duties on refined products make products in India cheaper than they are globally: This helps Indian consumers and erodes profits of refining companies.

Do these measures address the dollar deficit?

They do not. These are internal transfers and have no impact on the demand-supply of dollars, which is an external and binding constraint.

One can earn more dollars through higher exports of goods and services, or by attracting more capital inflows. However, in an environment of subdued global demand, growing exports meaningfully would be difficult, and would take time. Further, elevated macroeconomic and geopolitical uncertainty can pressure capital flows. Other than steps like restarting the process of India’s inclusion into global bond indices, there are limited options to improve capital inflows.

Thus, the only practical way out, in our view, is to reduce imports. One can achieve that by slowing down the economy, say by raising interest rates sharply, we believe this is too blunt an instrument. For example, if higher interest rates put brakes on the housing market, for every Rs 100 reduction in activity, imports would fall by only Rs 15 or Rs 20. On the other hand, letting the rupee depreciate would make all imports pricier, naturally bringing down their demand with less collateral damage. This is not a good option, but the least bad one given constraints the economy is facing.

Can India not use reserves it has built up?

India has sufficient foreign exchange reserves to fund this deficit for a while, but it would be unwise to do so beyond a few months. Policymakers are aware that India’s reserves are “borrowed”. Reserves of China, Japan and South Korea are “earned”, a result of sustained current account surpluses. India’s reserves are just due to excessive capital inflows, which in theory can also leave. Thus, we believe the best use of India’s reserves is to smoothen the rupee’s devaluation rather than obviate it.

How much does the rupee need to fall and how fast?

Currency weakness is likely to be gradual, not sudden, in our view. Unlike earlier episodes of global uncertainty, when exports fell and capital inflows slowed or reversed but imports sustained or grew, most recently in 2013, this time India has the foreign currency reserves to control the pace of depreciation.

Given a highly uncertain global economic environment, the level of the rupee against the dollar at which the imbalances go away is best discovered through calibration. Going by past trends, we believe RBI may target a 3-4% depreciation every three months until the dollar deficit disappears.

The writer is co-head of APAC Strategy and India Strategist for Credit Suisse