Synopsis

Even for apparently more enforceable support such as corporate guarantees (as distinct from letter of comfort), RBI said such structures can be used to enhance rating only if there is a strict timeline on invocation of guarantee by lenders.

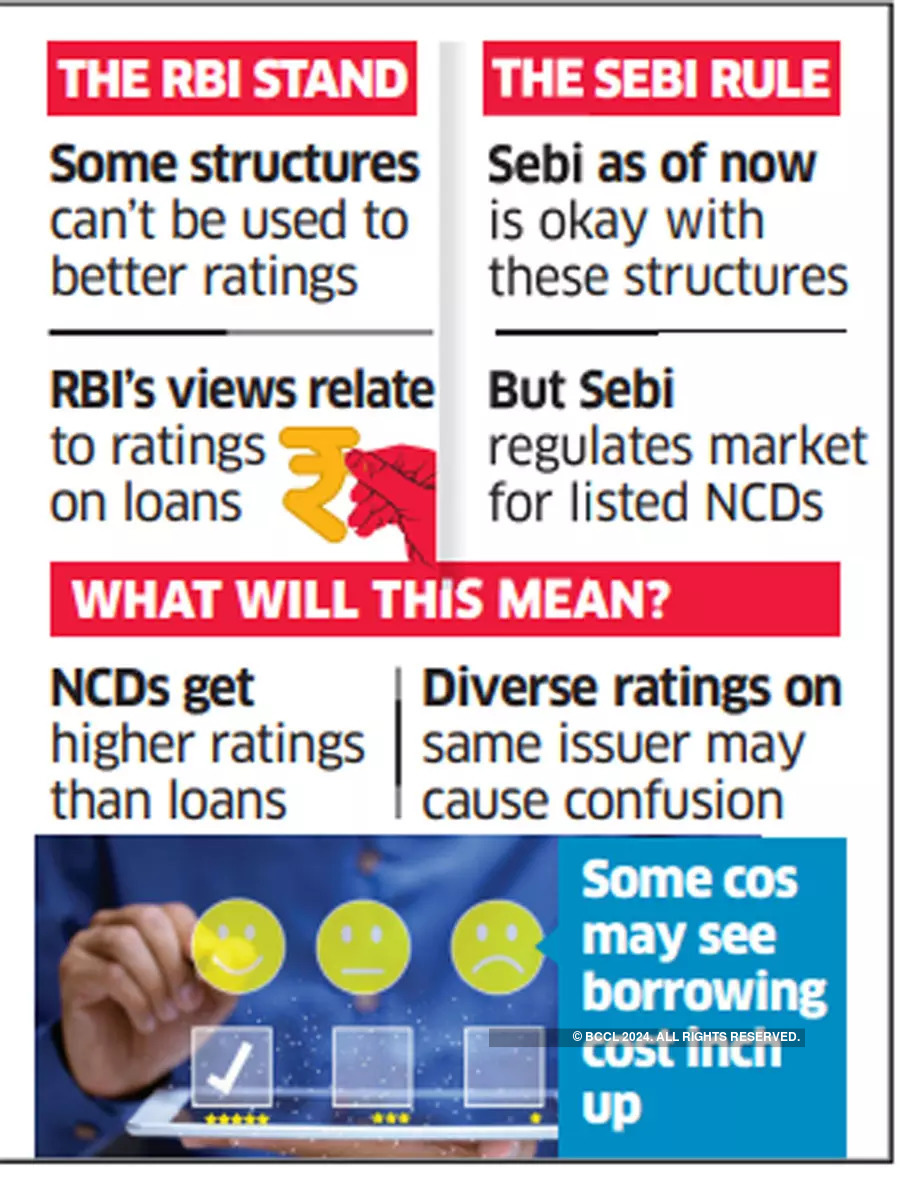

Credit rating agencies have sought the intervention of their primary regulator, Sebi, in the wake of new directions from the Reserve Bank of India (RBI) and the contradictions that have surfaced in the views of the two financial market watchdogs. The central bank has said ratings given on loans to a company cannot be notched up on the basis of “diluted and non-prudent support structures” such as letter of comfort, letter of support or undertaking, and other covers like pledge of shares.

Such support from the parent or promoters enables companies to reduce the cost of borrowings – as higher the rating, lower the interest charge on debt.

Even for apparently more enforceable support such as corporate guarantees (as distinct from letter of comfort), RBI said such structures can be used to enhance rating only if there is a strict timeline on invocation of guarantee by lenders.

“RBI’s instructions relate to ratings on loans from banks,” said a senior banker. “But according to Sebi’s existing directive, all these supports can be used to uplift rating for non-convertible debentures as long as the standalone rating (without support) is simultaneously disclosed.”

Several Structures Listed in Guidance

“But thanks to the RBI’s guidance, there would be situations where the same issuer has a higher rating for non-convertible debentures (NCDs) and a lower one on loan,” said the senior banker. “So, RBI and Sebi should sort this out to avoid confusion in the market.”

RBI’s April 22 guidance note to rating agencies also restrains them from deriving comfort from obligor-co-obligor structures. These are common arrangements by infrastructure companies where multiple special purpose vehicles (SPVs) – housing separate projects – pool their cashflow to create a mechanism where funds of one SPV can be used to service the debt if another vehicle facing a cash crunch finds it difficult to repay the loan.

“While such structures have become popular in infra and sectors like renewables, they are still untested for delinquency. So, RBI is probably sceptical because it is unsure how it would work when there is default, particularly if more than one SPV has problems and the total cash flow is inadequate,” said an industry person.

Many structured loans improved their ratings through shares pledged by promoters with at least a cover of 2x, that is, value of shares pledged is twice the amount lent. Along with this, there is an arrangement where more stocks have to be chipped in if there is a dip in the stock price and the cover shrinks to 1.5x.

“But there have been cases where promoters were not able to replenish the cover and top up stocks. Even mutual funds had invested in such instruments, backed by stocks from promoters. RBI’s concern may stem from such experiences and stock price volatility,” said an analyst.

Different Rules

Another question crops up. Even if rating agencies use these supports (on which RBI has put question marks) to give higher ratings to NCDs (the market for which is regulated by Sebi), will banks (regulated by RBI) invest in such debt instruments?

While the RBI directive endorsed the use of corporate guarantees for ‘credit enhancement’ (CE) – the parlance for rating improvement – it has laid down that banks have to formally agree to a timeframe within which they would invoke a guarantee following a loan default, while the corporate guarantor has to commit to a deadline to pay up once the invocation by lenders happens.