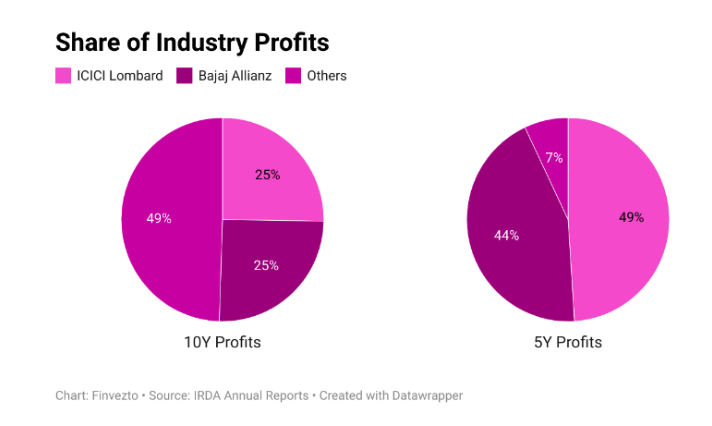

SynopsisICICI Lombard and Bajaj Allianz are 2 of the most efficient players accounting for almost half of the industry profits of the last 10 years and almost the entirety of the industry’s profits in the last 5 years. All the above point to a potential compounder franchise.

ICICI Lombard has operated with a focus on maximising profitability. That has meant moving in and out of segments with high competitive intensity and low profitability from time to time. This has led to the company being one of the most profitable players at a time when others are struggling. What lies ahead?

How can a company continuously lose market share over 14 years yet keep increasing its market cap and command the highest market cap in the industry? What does it say about the industry? Do investors reward growth or something else?

In spite of losing market share continuously from 11.5% in 2008 to 7% in 2021, ICICI Lombard accounts for 25% of the profits of the industry in the last 5 years. The country’s second largest general insurer is present in a hugely underpenetrated industry with a multi-decade growth opportunity, helmed by a conservative management team with a contrarian approach and laser-focus on profits and ROE.

General insurance works on a cash-before-cover model. This means that the insurer receives premiums upfront before coverage starts. And during this gap between receiving premium and paying claims, insurers can invest these premiums and earn income. This policyholders’ premium is referred to as float. A prudent insurer able to price risk appropriately (low claims ratio) and run the business efficiently (low operating expenses ratio) can, therefore, have money free of cost and make investment income out of it. Hence, for efficient players, general insurance is a multi-decadal wealth creation opportunity.

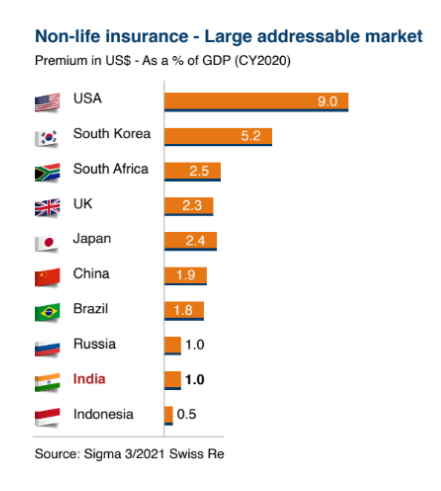

General insurance in India is a hugely underpenetrated industry. In spite of growing at 18% for a good part of the last 2 decades, the penetration has only moved from 0.5 to 1% of GDP. Globally, the penetration has moved from 3 to 4.1%.

ET CONTRIBUTORS

ET CONTRIBUTORS

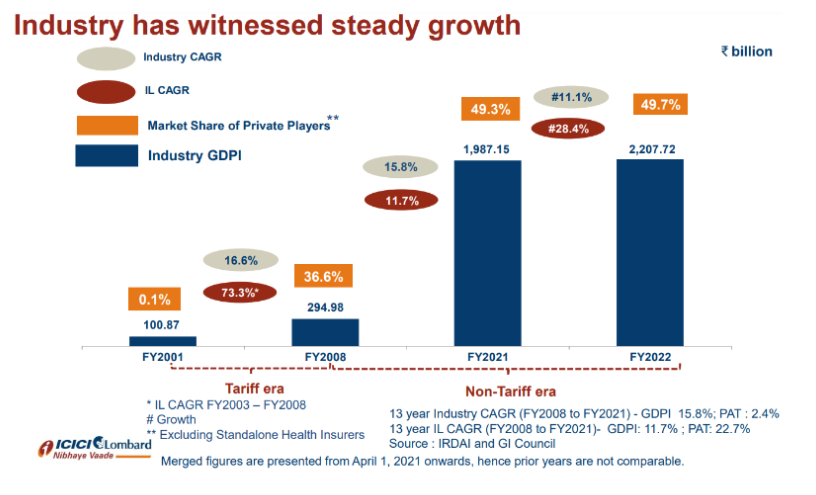

As a result, most players have had double-digit growth in the industry. ICICI Lombard, the largest private insurer, has grown at a rate slower than the industry average. This slower growth was more by design than due to an inability to grow.

ET CONTRIBUTORS

Over the years, ICICI Lombard has excelled in a few things. These have helped the insurer find steady grounds. Here is a look at those:

1) Stable underwriting with an ability to move in and out of segments depending on profitability

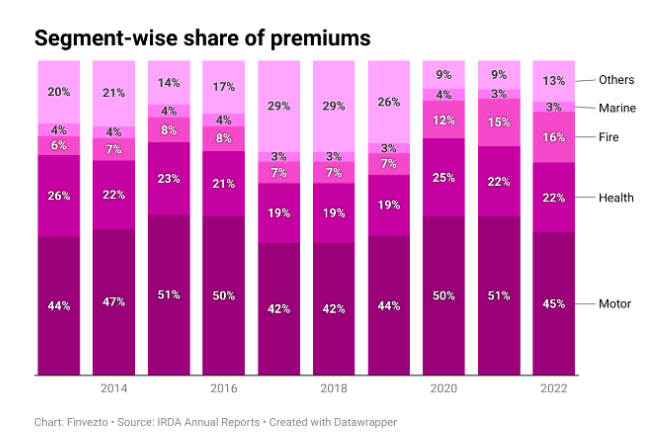

ICICI Lombard has operated with a focus on maximising profitability. That has meant shifting between segments depending on the competition and profitability measures. It shifted focus from fire in 2008-13, mass health segment in the mid-2010s and crop segment in 2019. It has also moved within the motor segments depending on the competitive intensity.

ET CONTRIBUTORS

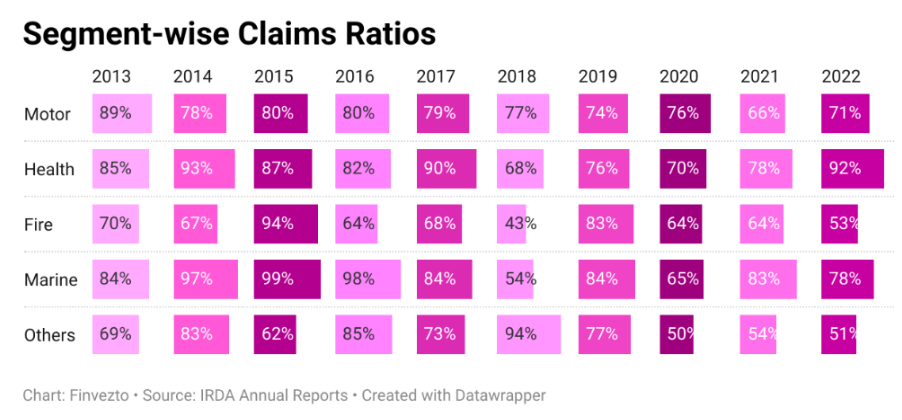

A closer look at the claims ratios suggests that ICICI Lombard has been cutting down exposure to the high claims ratio segments from time to time. Such a portfolio management process is a strong feature in ensuring sustainable profitability as growth isn’t really a problem in the industry.

ET CONTRIBUTORS

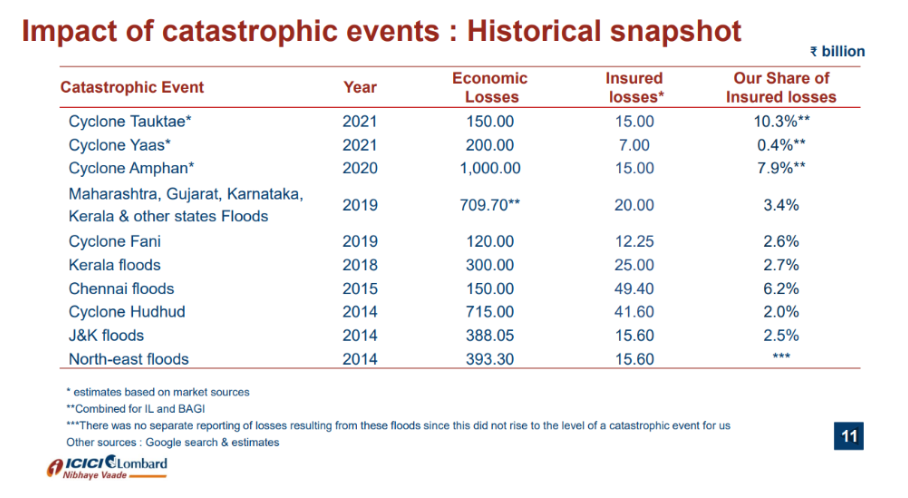

Similarly, ICICI Lombard has historically had a lower share of insured losses from catastrophic events than its market share. This underlines the insurer’s underwriting standards and reinsurance discipline.

ET CONTRIBUTORS

2) Conservative claims reserving leading to high policyholder float

Claims reserving is the process of reserving an amount in advance for yet-to-be-reported claims. This is a critical part of long-tail segments (a long gap between policy issuance, incident and claim reporting) like motor third-party covers. Insufficient claim reserving in the initial years can come back to bite when the claim eventually gets reported.

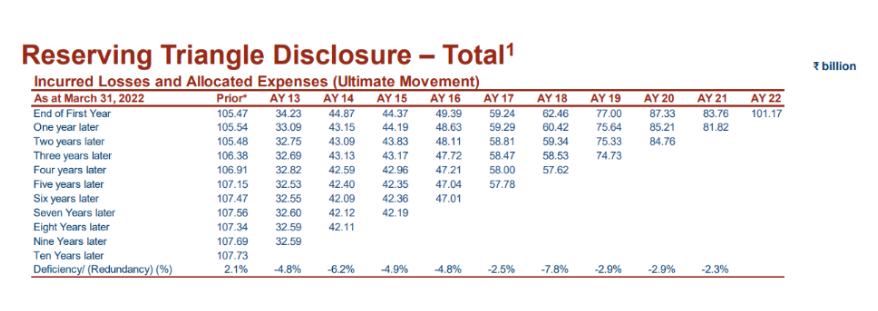

ICICI Lombard is among the most conservative when it comes to claims reserving. It is the only listed insurer in the country providing disclosures on reserving triangles. For each of the last 10 years, the movement of claims has been lower than what was reserved by the company. This means that ICICI Lombard’s claims ratios are usually exaggerated and profitability suppressed due to this conservatism.

However, this claims reserving is only an accounting entry and not an actual cash outflow. Conservative claims reserving helps ICICI Lombard maintain a higher policyholder float and, hence, higher investment income earned out of the float.

This is a key point in understanding general insurers. Just looking at the claims ratio to determine underwriting performance of insurers might be incorrect as it doesn’t take into account the conservatism of the insurer. Today, in the absence of similar reserving triangle disclosure by other players, there is very little comparison that can be done to determine factually the conservative insurers.

ET CONTRIBUTORS

3) Solid investment performance on the accrued float

ICICI Lombard’s asset allocation is more conservative than that of PSU insurers and more aggressive in comparison with those of Bajaj and other well-run private insurers. But the icing on the cake has been ICICI Lombard’s handling of its debt investments as it has had a strong reputation for not having any non-performing assets (NPAs). The investment yield has remained stable at 7-8.5% per year. With interest rates rising again, the yield can once again approach the middle of the range in the coming years.

4) Ever-improving technological muscle

ICICI Lombard has built strong leadership in technology by being the first insurer to launch online policy, first insurer to move completely to cloud, etc. Some of the solutions have been extremely productive and added value: such as InstaSpect (instant approval for 85% motor OD claims) and IL TakeCare (healthcare app to capture group health claims; 60% claims were apparently approved within 90 seconds).

Through these and many such efforts, ICICI Lombard has been able to improve employee productivity at 14% CAGR over the last 14 years.

The conscious choice to own the customers through in-housing of health insurance TPA and moving out of the leading insurance aggregator websites show clear intent in continuing the leadership and investing heavily behind customer experience, process excellence and underwriting execution.

5) Innovative products

Be it weather-based crop insurance schemes in the early 2010s or the recent sandboxes on motor premiums based on driving behaviour, ICICI Lombard has been at the forefront with innovative products. Also helping is the solution mindset demonstrated through several preventive corporate solutions in property and health.

6) Strong distribution capability

Strong presence with OEMs on motor vehicles, increasing presence with garages and hospitals, aggressively expanding the agent network for health insurance mean that the next few years will be focused on maintaining and strengthening the distribution capability.

ICICI Lombard and Bajaj Allianz are 2 of the most efficient players accounting for almost half of the industry profits of the last 10 years and almost the entirety of the industry’s profits in the last 5 years. All the above point to a potential compounder franchise.

ET CONTRIBUTORS

Over the last 2 years, however, the company has had to deal with multiple headwinds.

1) Slow premium growth

ICICI Lombard’s decision to exit crop business in 2019 and a prolonged pick-up in retail health meant that the premium growth significantly underperformed industry growth. This has raised doubts in the minds of some investors on the ability of ICICI Lombard to grow ahead of the industry.

2) Auto demand slowdown

ICICI Lombard has a higher share of new vehicle premiums compared with the industry. The prolonged auto slowdown — initially caused by the demand downturn and later further accentuated by Covid-led supply shocks and constraints — caused the slowest auto sales growth in the last 3 decades. This slowdown has had a much higher impact on ICICI Lombard. Also, because of the slowdown and the decrease in claims during Covid lockdowns, the competitive intensity in terms of pricing picked up and has affected ICICI Lombard’s growth further.

3) No motor TP price increases

As motor TP is the only regulated segment still and given that there were no price increases by the Insurance Regulatory and Development Authority (IRDA) for 2 years, the profitability of the segment started declining. And given the importance of the segment to the industry, industry profits have also come down. Even recently, the price increase announced by IRDA is in single digits, whereas the claims inflation for the past few years have been in double digits led both claims inflation of parts as well as led by court judgements.

4) Covid-impaced health insurance segment

Covid and its devastating health concerns have resulted in elevated combined ratios for almost all the general insurers.

All the above factors have contributed to stock prices correcting more than 30% from highs. But it also potentially made ICICI Lombard look like an attractively valued long-term portfolio company.

Investors should understand that there are some downside risks to consistent wealth creation.

1) Insufficient health segment scale-up

Standalone health insurers like Star Health have captured the major share in the retail health insurance segment by building a strong agency channel through the regulatory arbitrage of getting life insurance agents to double up as SAHI agents. Also, ICICI Lombard has at various points reduced growth focus on the retail-health segments. Now, the insurer is making significant investments in ramping up its agent workforce. Any continued loss of market share would, therefore, be seen as a failure in execution.

2) Motor TP tariff deregulation leading to price wars

IRDA has deregulated all segments except motor TP in 2008. This resulted in insurance players competing on price, leading to a decline in profitability for 4-5 years. The general insurance industry had to wait until 2013 before its players could become profitable again. Since then, private insurers have had a benign few years and the competitive intensity has not reached the earlier levels. Any deregulation of motor TP could lead to another round of price wars, resulting in poor profitability levels for the industry for a few years. Such a situation could de-rate all general insurance stocks and might be a good time to accumulate the most efficient players for the long term.

3) Potential increase in supply of shares in the medium term, as ICICI Bank has to reduce its shareholding to under 30% in the next couple of years

With the acquisition of Bharti AXA General Insurance, ICICI Bank’s shareholding in ICICI Lombard has fallen below 50%. According to the Reserve Bank of India (RBI), ICICI Bank needs to reduce the shareholding in the insurer to below 30%. It has another 2-odd years for that. This could result in a sustained period of increase in supply of shares if ICICI Bank chooses to sell in the market. Such a scenario could be averted with either a bigger acquisition or entry of a large strategic investor. Alternatively, depending on how the RBI handles HDFC Life/HDFC Ergo situation in the HDFC-HDFC Bank merger, ICICI Bank might want to bring back the shareholding above 50%, in which case this risk will get invalidated.

(Anand Ganapathy is founder of Finvezto & Prashanth Jana is an investor and IIM-A graduate. Views expressed are personal.)

(Disclaimer: The opinions expressed in this column are that of the writer. The facts and opinions expressed here do not reflect the views of www.economictimes.com.)

(Originally published on May 17, 2022, 12:37 PM IST)

Share the joy of reading! Gift this story to your friends & peers with a personalized message. Gift Now