SynopsisTata Group, led by N Chandrasekaran, shows no sign of a late entrant’s desperation as it opts for the inorganic route to build its e-commerce platform. Its M&A team engages with target companies for months, drives down prices, and gains control by infusing funds in tranches via various instruments. The founders, too, rely on the group to enable them to take their ventures to the next level.

Tough bargains, protracted deal talks, discounted pricing, convertible instruments, and value buying of market leaders characterise Tata’s startup acquisition strategy as Bombay House adds a string of consumer-Internet ventures to power its digital-business ambitions. Tata Digital has acquired e-grocery market leader Bigbasket and e-health platform 1mg, besides investing in wellness platform Curefit. It is on the prowl for more.

In a fortnight starting May-end, Tata Digital issued three press releases announcing these back-to-back deals. All of them were conveniently vague. None of them talked about the valuation of the acquired or invested companies. The stake that Tata has picked in each of these startups, or the future road map to increase ownership, were unclear, too. Tata Digital said it had acquired a majority stake in Bigbasket, it would acquire a majority stake in 1mg, and it entered into a memorandum of understanding to invest USD75 million in Curefit. There is hardly any detail beyond these terse lines.

While these deals culminated in May-June, they were in the works for about a year. News of a potential Tata investment in Bigbasket and 1mg started floating in September last year.

While Tata Sons is determined to catch up with rivals and carve its presence in digital commerce, it shows no signs of desperation. It is neither frantic nor extravagant in its dealmaking. While it may spot a number of leaders in each segment, it takes advantage of the target companies’ desperate need for capital, competition pressures, and the pandemic blues they faced. The group takes its time, drives down the prices, and wins control through capital infusion in tranches.

Waiting it out for the right moment

In an earlier article, ET Prime had explained how Bigbasket, the market leader in e-grocery, was valued modestly in relation to its growth in gross merchandise value, top line, daily orders, and user base. Its sales volume doubled in a year and business-advisory company PGA Labs’ research shows it commanded nearly 37% market share against immediate rival Amazon’s 15%. But the valuation didn’t move in step with the business performance.

Tata bought out Alibaba and other investors at 50% premium to the last valuation. Alibaba last invested about USD50 million in Bigbasket in April 2020 at USD1.2 billion pre-money valuation. Tata bought the shares of Alibaba, Abraaj Group, Ascent Capital, and Sands Capital at USD1.8 billion valuation early this year. It thus became a majority shareholder in Bigbasket, commanding a 53% stake. Numbers from startup-data company Tracxn show that the private stocks of Bigbasket were then priced at INR1,271.87 apiece. Four months later, the Tatas increased the stake through fresh equity infusion at a discounted price. The price was INR1,005.06 per share. In essence, the stake increase price was at a 21% discount to the acquisition price.

The predicament of Alibaba, the strategic investor which held a 30% stake, in the wake of the restrictions on Chinese investors, may have helped the Tatas moderate the price at the time of the secondary share purchase. Once Tata gained majority control, it was in a position to determine the price for fresh issuance of shares.

Flat rounds, debt rounds

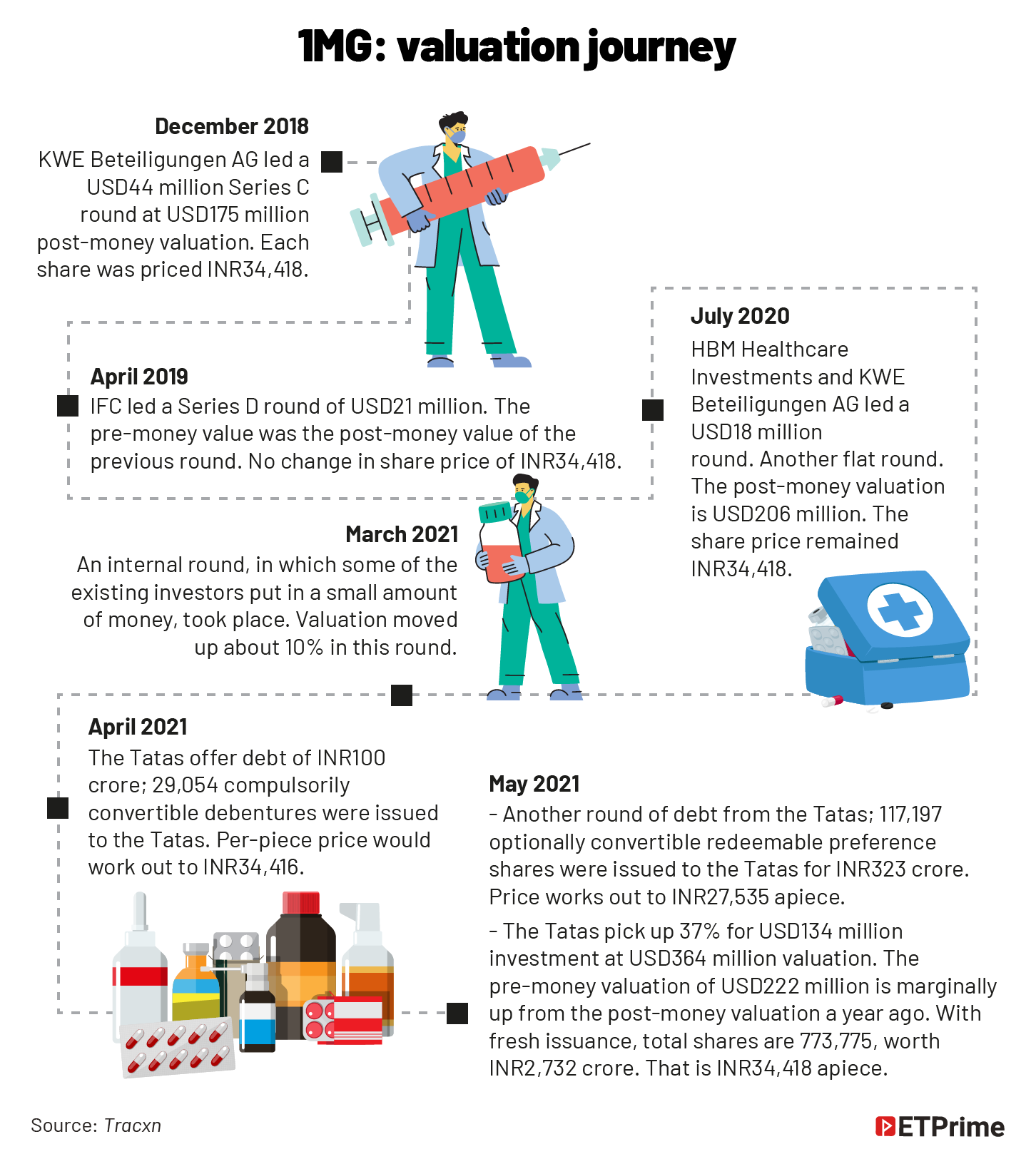

The 1mg acquisition was even more interesting. In December 2018, Swiss venture-capital firm KWE Beteiligungen AG led a series C3 round in 1mg at USD175 million post-money valuation. According to Tracxn, the share price was fixed at INR34,418 then.

In four months, 1mg had a new round of funding. But at USD175 million, the pre-money valuation in this round was the post-money valuation of the previous round. In simple terms, there was no upside; it was a flat round. There was no change in the share price. Another flat round followed a year later, when the company raised USD18 million, leading to more dilution.

Enter the Tatas. While there were reports of a deal for months, the Tatas first came on the scene only in April this year via a debt round. The transaction data on Tracxn reveals how Tata went about the 1mg investment. It invested INR100 crore through the compulsorily convertible debentures route. Why debt? A possible reason is a capital crunch that needed to be sorted when the acquisition talks were yet to conclude. A month later, the Tatas further invested INR323 crore and received optionally convertible redeemable preference shares.

Tracxn data does not show the debentures-to-equity conversion ratio. But the number of debentures and the amount of debt make the price per piece the same as 1mg’s shares in December 2018. The subsequent preference shares were issued to Tatas at 20% discount to this price, at INR27,535.

On May 25, 1mg raised fresh capital, primarily from Tata. After two back-to-back debt rounds, this was the first equity round in 1mg in which Tata participated. It put in USD134 million and picked a 37% stake. On conversion of the debt it provided to 1mg into equity, the Tatas will become the majority shareholder. Tata Digital announced on June 10 that it would acquire a majority stake in 1mg.

The total worth of 1mg after the acquisition, when fresh capital was infused into the company, was INR2,372 crore or USD364 million. This means the pre-money valuation was USD222 million, marginally up from 1mg’s valuation a year ago. The acquisition round was pretty much a flat round. In simple terms, if we factor in the USD30 million 1mg raised in the past two years, its valuation did not move much from USD175 million in December 2018. The price of 1mg shares at INR34,418 apiece has remained unchanged.

In essence, Tatas acquired 1mg at a price at which the latter was valued two and a half years ago, irrespective of the growth the startup may have seen following the increased adoption of online delivery of medicines, online booking of diagnostics, and e-consultation. Its business volume nearly doubled in the past two years, according to a source.

1mg is one of the top two players in the sector and claims 40 million monthly users. Reliance’s acquisition of 1mg’s competitor Netmeds, Amazon’s entry into the sector, and the PharmEasy-Medlife merger that propelled its quick growth to a unicorn, have put pressure on 1mg to opt for strategic options. Exactly as in the case of Bigbasket, the Tatas stepped in at the right time.

As mentioned earlier, the Tatas’ investment in 1mg is part equity and part debt. Of the USD190 million that Tata has invested, about USD56 million is by way of debt. The conversion of these instruments into equity may be linked to the performance of the company and its management. On achieving certain milestones, they may convert into equity at a specific date. Thus the Tatas are in a position to control the performance of the management, and, more important, control the price/ratio at the time of conversion of the debt into equity.

“There was enough capital chasing Bigbasket. But when they got significant interest from Tata, they chose to go with them.”

— Nilesh Kothari, managing partner, Trifecta CapitalAccording to a top source, the Tatas opted for convertible instruments in the Curefit deal, too. Tata announced the deal to put USD75 million in Curefit but did not specify the nature of the investment. Curefit, which was once shaping into a full-stack wellness platform, underwent a split when its food business under co-founder Ankit Nagori was separated from the parent entity. The remaining piece of business, primarily the network of gyms, suffered massive loss of business because of the pandemic.

The M&A guys

Having taken the inorganic route to build their digital business, the Tatas have so far done a good job in dealmaking. Industry sources say Tata’s mergers and acquisition (M&A) team under group CFO Saurabh Agrawal has created ripples in the startup world. M&A is the forte of Agrawal, who was handpicked by Tata Group chairman N Chandrasekaran as the first one to hold the post.

Previously, as strategy head of Aditya Birla Group, Agrawal oversaw the Vodafone India-Idea merger and the acquisition of Jaypee’s cement assets, according to an ET report. His long years at DSP Merrill Lynch, where he was head of investment banking, and later at Standard Chartered Bank as south Asia head of corporate finance, have become particularly useful as a string of acquisitions and investments are in the making. Agrawal has a long association with Chandrasekaran, advising TCS on IPO and a string of acquisitions during his DSP days, according to the report cited earlier.

A key member in Agrawal’s M&A team is Ankur Verma, head of corporate development, who was previously the managing director of the investment banking division of Bank of America Merrill Lynch (now called Bank of America and BofA).

Modan Saha, CEO of Tata Strategic Management Group, too, plays an important role. Another person who was involved in the deal talks with startups was general counsel Shuva Mandal, who left the group in January to start a new legal practice. Nipun Aggarwal, senior vice-president, investment management, also takes part in the deliberations. Like CFO Agrawal and Verma, Aggarwal too comes with experience in investment banking and corporate finance. He previously worked with Standard Chartered Bank and Bank of America Merrill Lynch.

The goodwill premium

In mid-2020, the founders of 1mg were moving ahead with the plans to close a fresh venture-capital round when the Tatas approached them for a buyout deal. Despite the higher valuation offered by the financial investors, the founders chose to go with the Tatas.

It took about a year for the acquisition to conclude. As explained earlier, the price was flat at 2018 levels. But that did not affect their decision. The same thing played out in the case of the Bigbasket deal, too. Amid rising competitive pressure, the founders chose to be part of Tata Group rather than carry on with the independent pursuit. When the funding from Bigbasket’s strategic investor Alibaba was restricted as a fallout of geopolitics, a number of large fund houses were ready to step in, according to some of the Bigbasket investors.

“There was enough capital chasing Bigbasket. But when they got significant interest from Tata, they chose to go with them,” says Nilesh Kothari, managing partner of Trifecta Capital, the venture-debt firm which is an investor in Bigbasket.

The M&A team used Tata’s goodwill to good effect. The back-to-back deals have sent out a message that the Tatas have ambitious plans. “The Tatas are looking at sizable companies with stable growth,” adds Kothari.

But they have a lot of catching up to do. While many disparate digital entities, from Tata CliQ to Tata Health, have been in existence for quite some time, a focused effort to build a consumer-facing digital platform is relatively recent. Tata Digital, the Tata Sons subsidiary that will drive these initiatives, is the newest entity within the group, incorporated as recently as March 2019. Chandrasekaran, popularly called Chandra, put a number of his key associates from the TCS days in charge of this critical initiative, starting with Pratik Pal, the CEO.

Pal was formerly global head of retail, travel, and consumer business units at TCS. Tata Digital board members Aarthi Subramanian and Suprakash Mukhopadhyay also were top TCS functionaries.

According to a source, Chandra was particularly keen on digital health. He sees healthcare as a missing piece in Tata Group’s portfolio, an inspiration for his team to pursue deals in this space.

His book, Bridgital Nation, holds clues to his interest in the sector. The book predominantly talks about reimagining healthcare access through technology and the first two chapters vividly narrate the entrepreneurial work of a driver in Silchar, Assam, who transports patients from the interiors of northeastern states to hospitals.

This driver became a full-time “medical co-ordinator” who guides his clients to the right doctor for a fee. The anecdote brings home the need for trustworthy intermediaries to address the access challenge.

“The entire edifice of healthcare relies on creating an environment of trust,” he wrote in the book. He clearly sees an opportunity to leverage the Tata legacy to build a healthcare platform. Last week, the founders of 1mg sent out a letter to customers announcing the change of the brand name to ‘Tata 1mg’. They said the new identity signifies the coming together of the icon of trust and the popular healthcare platform.

An important aspect of the Tata strategy is the reliance on the founders to continue to drive their ventures and take it to the next level. That is a reason why they preferred stability to high valuation and signed on the dotted line. While the stake size of the Bigbasket and 1mg founders have been further diluted in the deal, the promise of future rewards seems to be in place. A case in point is how new shares at discounted price were issued to 1mg founders in the acquisition round. The founders remain an integral part of the ride.

In the case of Curefit, founder Mukesh Bansal was roped in as president of Tata Digital, and other founders, including Hari Menon of Bigbasket and Prashant Tandon of 1mg, have also been made part of the Tata Digital leadership team.

Unlike Reliance, which lapped up distress assets such as Zivame, UrbanLadder, and Milkbasket at throwaway prices to build different e-commerce verticals and digital services, the Tatas have focused on acquiring market leaders at a fair price, against the tide of bullish valuations in the venture-capital world.

Media reports have already surfaced about Tata Digital’s talks with delivery startup Dunzo. A delivery arm that serves multiple e-commerce verticals makes sense in Tata’s super-app scheme of things.

It would be interesting to see how its deal team gets this one done.

(Graphic by Sadhana Saxena)

The latest from ET Prime is now on Telegram. To subscribe to our Telegram newsletter click here.