SynopsisThe Indian pharmaceutical market forms a significant part of the healthcare sector’s ecosystem. According to the National Health Accounts, 2016-17, published by the Ministry of Health and Family Welfare, pharmacies account for 28% of the healthcare expenditure in India.

MedPlus has done an IPO. Wellness Forever is also lining up with one. Apollo’s pharmacy business is showing decent revenue growth. Let us take a closer look at the retail pharmacy store business.

The Indian pharmaceutical market forms a significant part of the healthcare sector’s ecosystem. According to the National Health Accounts, 2016-17, published by the Ministry of Health and Family Welfare, pharmacies account for 28% of the healthcare expenditure in India. Data from the World Bank indicates that India is characterised by low per capita healthcare expenditure and a high share of out-of-pocket expenses. This presents a good growth opportunity, considering the limited penetration of healthcare services, especially in the rural parts of the country.

A retail pharmacy is a retail store that sells drugs and medicines that are either patented, over-the-counter (OTC, or does not require a prescription) or generic. Being an essential service, the retail pharmacy sector, in general, witnessed a rising demand for OTC and prescription drugs as well as wellness products during the pandemic. The sale of pharma products associated with preventive healthcare and personal hygiene also gained prominence as consumers looked to boost immunity in the wake of the situation due to the virus.

Medplus has done its IPO in the last week. Wellness Forever is following up in the next few months, and if we look at e-commerce players, PharmEasy has filed its DRHP in November. With the effects of the pandemic seeing a declining trend, a lot of companies in the pharma and associated sectors have reached the top of the earnings cycle compared with the pre-pandemic quarters. In the last one year, over Rs 1,00,000 crore have been raised from IPOs, FPOs and OFS. The conditions have lately started looking ripe to take companies public.

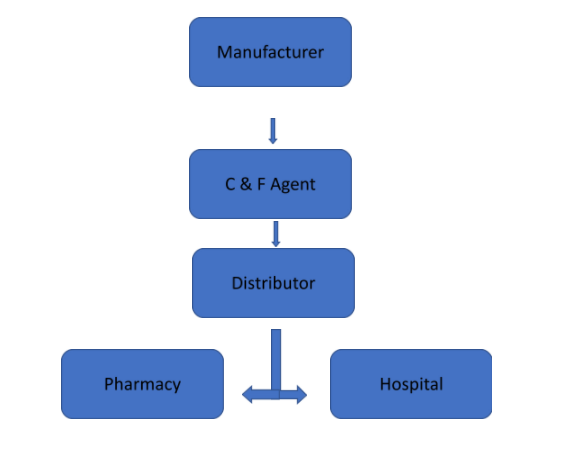

In the context of the Indian pharmaceutical industry, the supply side looks a little like this:

ET CONTRIBUTORSPharmaceutical companies usually have a C&F agent (carry forward agent) who is tasked with handling the warehousing, transportation and distribution of the drugs to distributors. In certain cases, the distributor also supplies through a sub-distributor, or an exclusive distributor may be appointed for a particular channel or customer.

According to the red herring prospectus filed by MedPlus, the network of pharma ecosystem in India consists of more than 500 companies involved in manufacturing, around 60,000 distributors and around 800,000 retail outlets that supply over 100,000 pharmaceutical brands to the consumers. Hence, the retail side of pharmacies is a big market. So far, it has been dominated by the traditional channels — the local pharmacy shops within a general range of 150-1,000 sq ft.

In recent years, there has been an emergence of modern retail channels. These mainly include a chain of pharmacies that operate under a brand name, maintain a value chain right from sourcing of products to warehousing, and then distribute through their stores.

The modern retail channel also includes the e-commerce channels that deliver drugs at home and only have an online presence. This includes players like PharmEasy, Netmeds and 1mg. Additionally, there are omnichannel networks, too, which combine the two modern forms by having brick-and-mortar stores and also an online presence. Medplus, Apollo Pharmacy, and Wellness Forever are some examples of such omnichannel networks.

The store count of Apollo Pharmacy, Medplus, and Wellness Forever has seen a steady increase in the last three years:

ET CONTRIBUTORSSource – Medplus DRHP

All these three players have had impressive revenue numbers per store — over Rs 1 crore per store — in the last three years. Pharmacy retail is also characterised by high inventory turns and economies of scale due to working capital efficiency.

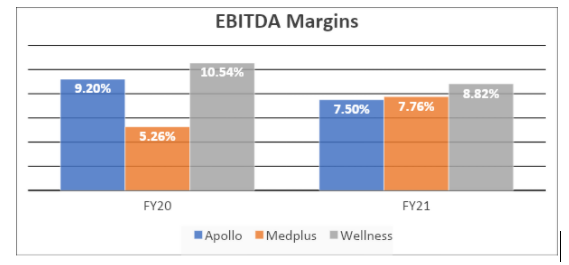

Now, let’s look at the picture of these companies when it comes to margins:

ET CONTRIBUTORSSource – Medplus DRHPLow margins are not necessarily a bad thing if the volumes are high and sustainable. But let us now look at some of the challenges this industry faces or will face, and could magnify the problems for players growing at wafer-thin margins:

- Highly overcrowded space – A lot of players have emerged in this space in the last 4-5 years. All players are fighting to gain more online presence, where retail pharmacy faces competition from e-commerce players as well. In the face of stiff competition, profitability might get further hampered due to the need to incur higher marketing costs to enhance presence and also the need to give higher discounts than competitors.

- Change in market dynamics – Covid has been a big reason for the current surge in the numbers of retail pharmacies. Omnichannel platforms had decent tailwinds during the pandemic as there was an increased need for drugs and demand for products like nutraceuticals. The environment after the pandemic subsides is still uncertain, and it remains to be seen if the environment will continue to remain conducive for retail pharmacy chains.

- Tightly regulated industry – In an industry involving sale of pharmaceutical products, laws and regulations are highly regulated. Factors like drug eligibility and capping of certain prescription drugs could adversely affect the business. The price of certain pharmaceutical drugs is controlled by agencies like the DPDO (Drugs Price Control Order) and the NPPA (National Pharmaceutical Pricing Authority) and this could be a significant hindrance on the margins.

- Expansion into newer markets comes with various challenges – Retail pharmacy chains need to expand into newer markets constantly in order to grow. This comes with challenges like establishing newer supply chain networks, decoding behavior patterns, gaining knowledge of risks of local laws, and the need to undertake debt to expand. Failure to expand can significantly hamper operations and margins of the company.

Adding on to the factor of high competition, it is also important to note that certain businesses like Apollo Pharmacy have the backing of their hospital business to help sustain and grow their numbers. The pharmacy stores of Apollo, for example, which are located on the premises of Apollo Hospitals, have strong numbers and are sticky as they offer convenience to patients. Certain drugs prescribed by doctors at these hospitals might be available only in their own pharmacy. Brands like these have a longer operating history; high recognition; better financial and supply chain management, and technical resources that other players might not possess.

Hence, the revenue and store-growth numbers in the modern retail pharmacy industry might continue to look impressive. But the challenges are significant as well. The retail pharmacy chain business and e-commerce pharmacy business will look to cash in on the share of the unorganised market in this sector — a massive space. However, it remains to be seen how these companies will grow as the pandemic wanes and whether the growth comes at the cost of margins.

(Gaurav Jain & Parimal Ade are Founders, InvestYadnya.in. Views are their own)

(Disclaimer: The opinions expressed in this column are that of the writer. The facts and opinions expressed here do not reflect the views of www.economictimes.com.)

Share the joy of reading! Gift this story to your friends & peers with a personalized message. Gift Now