Clipped from: https://economictimes.indiatimes.com/industry/banking/finance/banking/view-cash-is-dying-but-we-arent-ready-to-bury-it/articleshow/88157151.cmsSynopsis

If all the money in circulation is private, controlled by e-commerce and social media platforms, authorities won’t be able to protect consumers from being exploited.

The demise of cash is near. As consumers, though, we should hope that the end doesn’t arrive too soon.

It isn’t the pandemic that’s putting this popular means of payment out of existence. All that Covid-19 has done is to accelerate a trend that was already with us. When Steve Jobs unveiled the first iPhone in 2007, he began killing the need for banknotes. Autonomous cars, self-ordering refrigerators and our digital avatars in the metaverse will put the final nails in King Cash’s coffin.

Covid-19 shifted $5 trillion in global retail sales from offline to online. To the extent that a big chunk of this value was transacted in cash (47% in the euro area), the idea that central-bank-issued currency was a must for purchasing daily essentials took a knock. After an initial bump in precautionary cash hoarding, curbs on mobility and the fear of catching germs from handling paper money forced a change in habits.

Where governments gave out vouchers to perk up spending — like in Hong Kong — millions of consumers and thousands of merchants became new users of online payment systems just to utilize the handouts. Many will likely continue using these new ways to settle bills.

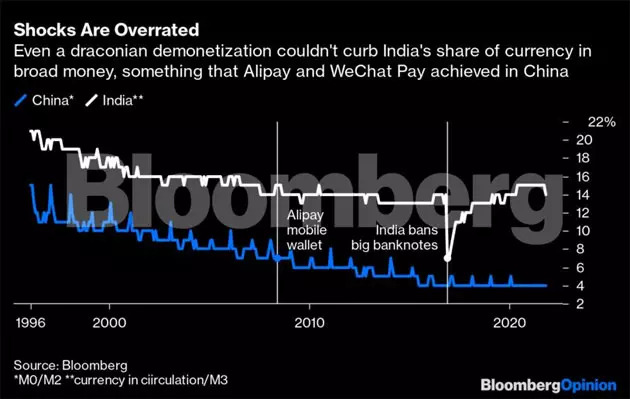

But just how crucial were these changes in the overall scheme of things? The different trajectory of banknotes in China and India provides a natural experiment to gauge the relative importance of temporary shocks and steady technological change.

Cash use plummeted in India after Prime Minister Narendra Modi cancelled 86% of the existing legal tender overnight as part of a botched economic experiment. That was five years ago. Nowadays, digital payments are booming, but cash is once again 14% of the broad money circulating in the economy — the same as before demonetization. In China, where physical currency was made irrelevant by the growing ubiquity of Alipay and WeChat Pay, the central bank’s IOUs to the public account for only 4% of money.

Technological progress lacks the drama of a behavioral shock, but it’s no less stunning. As JPMorgan Chase & Co.’s Jeremy Balkin and Neha Wattas remind us, the fastest way to move money from New York to London as recently as 2010 was to catch a flight from JFK to Heathrow and deliver it in person. Their report, provocatively titled “Payments Are Eating the World,” notes several shifts taking place in unison. In China, super-app platforms transformed money; elsewhere, the rise of a creator and gig economy is doing it. Globally, 50 million people are blogging, making short videos or telling people what to buy on the internet — and getting paid online as well.

Digital wallets are mushrooming everywhere, but what gets stored on them is changing because of another technological revolution: blockchain. Fintech firm Circle has teamed with Visa Inc. to enable business customers to spend USD Coin — a currency on the Ethereum blockchain that pegs its value to the dollar — with 70 million merchants. An equally important phenomenon is “buy now, pay later,” which is embedding finance (and cashless payments) even into low-value transactions: like buying lipstick in three installments.

Wait until each of our 15 internet-of-things devices does its own shopping, using central bank-issued programmable digital cash to pay only when they get the right stuff. While all this is happening in the real world, an entirely new parallel stream of consumption in the alternate reality of the metaverse could be as substantial as $390 billion by 2025.

Innovation in payments is an even bigger phenomenon in emerging markets than in developed economies. Last month, smartphone-based apps running on a shared public utility cleared the equivalent of $100 billion in domestic Indian payments, rising from less than $15 million five years earlier. And this is just the beginning. Alphabet Inc.’s Google, which alone handled $38 billion of these instantaneous transfers, has now developed an Android-based sub-$100 phone. The idea is to bring mobile internet to the bottom of India’s consumption pyramid.

Cash is still coveted, especially in a highly informal economy like India’s. But its importance as a means of payment is declining. In 2003, about 35% of cash in the euro area was used in domestic transactions; that number fell to an estimated 20% in 2019. Anywhere between 30% to half of banknotes have ended up overseas, while the rest are being hoarded in the euro zone: To some investors, a safe sovereign liability that pays zero is better than negative-yielding government bonds.

As cash vanishes into vaults — without a central bank digital currency, or CBDC, replacing it — the public’s trust in the convertibility of deposits into official money may become “more of a theoretical construct than a daily experience,” according to a recent research paper by the European Central Bank’s Ulrich Bindseil and others. That can destabilize entire financial systems.

If all the money in circulation is private, controlled by e-commerce and social media platforms, authorities won’t be able to protect consumers from being exploited. Which is why even in countries where technology has turned it into an anachronistic appendage, cash can’t be allowed to die. Not before CBDCs are ready.