In most cases, the demand in the anchor category gives an indication to how successful the IPO is likely to be

Every IPO has three main buckets or categories

Every IPO has three main buckets or categories

Record mobilisation via initial public offerings (IPOs) this year has turned the spotlight on anchor investors. Who are anchor investors and what role do they play? Let’s find out.

Who is an anchor investor?

Anchor investors (referred to as cornerstone investors in some global markets) are marquee institutional investors who are allotted shares in a company ahead of its IPO. This is done to demonstrate healthy demand for the shares of soon-to-be-listed companies. Typically, if the list of anchor investors is good, it provides a boost to the IPO as it lures other investors to put their money in the company. Anchor allotment can be made only to so-called qualified institutional buyers (QIB). QIBs are entities such as sovereign wealth funds, mutual funds, pension funds and foreign portfolio investors (FPIs) registered with market regulator, the Securities and Exchange Board of India (Sebi).

When and how are anchor investors allotted shares?

Talks between the issuer and potential investors begin well in advance. However, the allotment can only be made one day prior to the IPO. (Paytm’s IPO opens on Monday. However, Thursday and Friday being market holidays, the allotment was made on Wednesday.) In most cases, anchor investors are allotted shares at the top-end of the IPO price band. The list of investors to get allotment in the anchor book is decided by the investment bankers handling the IPO and the issuer company. Anchor allotments are made on a discretionary basis, unlike in the IPO, where allotment needs to be done on a proportionate basis.

How many shares are reserved for anchor investors?

Every IPO has three main buckets or categories. These include QIBs, retail investors (those investing up to Rs 2 lakh) and non-institutional investors (NIIs includes high net worth individuals, corporate entities and family offices). Companies with a profitability track record can have to reserve 50 per cent shares for QIBs, 35 per cent for retail and 15 per cent for NIIs. Companies that don’t meet Sebi’s profitability criteria have to compulsorily allot 75 per cent to QIBs, 15 per cent to NIIs and only 10 per cent to retail. Anchor quota is carved out from the QIB portion. According to Sebi rules, a maximum of 60 per cent of the shares reserved for QIBs can be allotted to anchor investors. A third of the shares available in the anchor book are reserved for domestic mutual funds.

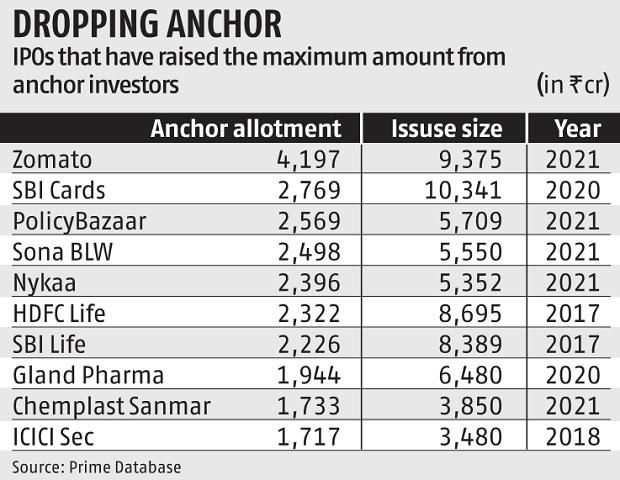

As most startups don’t meet the profitability criteria, the QIB portion in their IPO increases to 75 per cent from 50 per cent. This also increases the quota meant for anchor investors (from 60 per cent of 50 per cent QIB quota to 60 per cent of 75 per cent QIB quota). As a result, a large portion of the shares sold in the IPO get allotted to anchor investors even before the IPO opens. For instance, 45 per cent of shares sold by Zomato, PolicyBazaar and Nykaa were allotted to anchor investors ahead of the IPO. This shrinks the number of shares available in the QIB quota at the time of the IPO.

Do anchor investors indeed boost IPO prospects?

In most cases, the demand in the anchor category gives an indication to how successful the IPO is likely to be. If the company fails to generate enough demand in the anchor book, it can be perceived negatively by the market. However, each investor is driven by different considerations. Typically, those investing in the anchor book take a very long-term view on the company, while HNIs and retail look to make a quick buck and exit. Therefore, there have been instances where anchor demand has been strong yet the issue has got lukewarm response from HNIs and retail during the IPO.

Is there a requirement for a minimum number of anchor investors?

IPOs of less than Rs 250 crore are required to make allotment of at least five and at most 15 anchor investors. An additional 10 investors are allowed for every Rs 250 crore increase in IPO size. A minimum allotment of Rs 5 crore has to be made to each investor. Recently, some FPIs have made an appeal to Sebi to increase the maximum limit set for anchor investors.

Do anchor investors have to observe any restrictions?

While those allotted shares in the IPO can sell any time after the listing, anchor investors are subject to a lock-in period of 30 days from the date of allotment. In the recent past, it has been observed that shares of companies tend to correct after this 30-day period has ended as anchor investors have looked to book profits.